The Ultimate List of Credit Card Statistics for 2025

Despite credit cards being one of the most expensive ways to get money, consumers have become increasingly reliant on them for paying bills and refinancing debts. Nevertheless, the latest credit card statistics show that wages haven’t caught up with the increased cost of living, resulting in people spending more than they earn.

If you’re interested in learning more about credit cards, this list will give you a peek into the average number of credit cards in circulation, the best credit card mobile processing solutions, the total credit card debt, and other fascinating findings shaping the credit market today.

Key Credit Card Statistics

- There are 2.8 billion credit cards in use globally and 1.06 billion in the US.

- MasterCard has 551 million credit cards globally, making it the most common credit card.

- Crypto-linked credit cards are on the rise, with Visa reporting $1 billion in revenue from them in the first half of 2022.

- In 2022, fraud attempts will account for nearly a quarter of all digital interactions.

- Stolen credit card numbers cost as low as $5 on the black market.

General Credit Card Statistics

1. By 2028, the global market for digital payments is projected to reach $194.2 billion.

(PR Newswire)

Digital payments are transactions made over the internet or through a mobile channel. Great examples are card and eWallet payments.

According to projections, the industry will increase at a compound annual growth rate (CAGR) of 17.6% over the next six years, reaching $194.2 billion. That might be ascribed to the rising desire for quick and safe transactions, as well as China and India's rapid growth rates.

2. By 2025, the global payments market is expected to be worth $2 trillion.

(Valuates)

According to Valuates' analysis of the market size, position, and forecast projections for global payments from 2018 to 2025, the market will grow at a CAGR of 7.83%. The demand for near-field communication (NFC)-based mobile internet payments is also rapidly expanding. Here are some of the vital payment market trends and analyses:

- North America was the first region to do more than half of its transactions electronically.

- The payments industry has been growing the fastest in Latin America.

- Nearly half of worldwide payments revenue is generated in the Asia-Pacific area.

The following companies offer the best business bank accounts and payment solutions:

- PayPal

- Citibank

- Bank of America

- Wells Fargo & Company

- JPMorgan Chase & Co.

- Apple

3. The typical American has 3 credit cards.

(Experian)

Most adults have multiple credit cards. The figure for 2021 is down 4% from the previous year. According to credit card usage statistics from Experian, the drop was due to a pattern of US consumers paying off outstanding credit card debt as the coronavirus pandemic wreaked havoc on the economy.

Here’s how many credit cards each generation has on average: Gen Z has 1.4 credit cards, Millennials have 2.5, Gen X has 3.2, Baby Boomers have 3.5, and the Silent Generation has 3.

4. After introducing digital wallets, PayPal witnessed a net gain of 22.3%, while mobile wallets saw a 20.4% growth.

(PayPal) (Statista) (Consumer Reports)

As if purchasing with credit couldn't get any easier, the emergence of digital wallets has made it even easier. Americans and others worldwide are now using their phones to make purchases, eliminating the need for cash or carrying a wallet full of cards. According to Statista, over a third of US smartphone users will use contactless mobile payments in 2022, up from 25.3% in 2018.

5. New forms of payment may blur the conceptual link between spending and having less money.

(New York University)

A professor of marketing at New York University conducted a study in which she asked respondents to rate how comparable credit cards are to cash on a 100-point scale, with 100 being completely similar. The average response was 72.

When she compared cash to Apple Pay, a digital wallet, the average went down to 56. The study demonstrates that spending cash is not the same as spending with a digital wallet, which entices consumers to spend more with a simple tap of a phone.

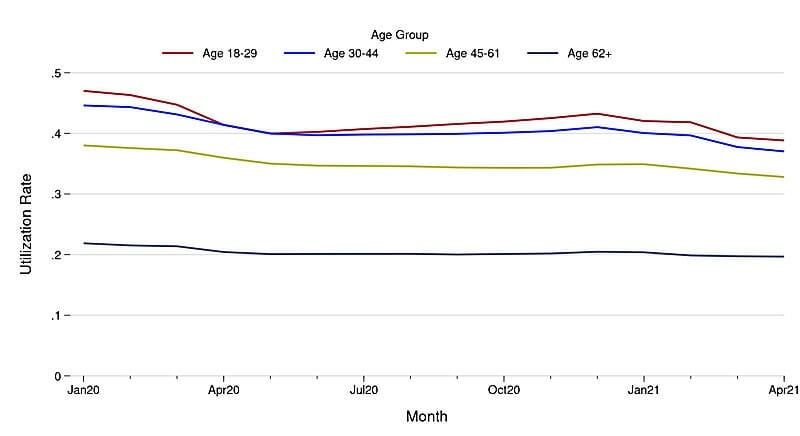

6. 87% of consumers over the age of 65 own a credit card.

(Reserve Bank of Boston) (Quartz)

Consumers aged 55 to 64 are the most likely to use a credit card (78.1%), while consumers aged 45 to 54 use it 70.5% of the time. The younger age groups have a lower propensity for credit. We see the 35 to 44 and 25 to 34 demographics use credit cards around 69% of the time, while fewer than half of customers under 25 use them.

7. In 2021, utilization ratios and card balances both declined.

(Experian)

According to a study from a credit bureau called Experian, consumers have steadily reduced their card debt in recent years. The average credit card balance in 2019 was $6,494. In 2021, the average balance declined to $5,525, down from $5,897 in 2020.

Credit utilization rates, which reflect how consumers use credit, fell to 25% in 2021, down from 26% in 2020 to 30% in 2019. Lower card debt and utilization rates suggest that US families may be better financially prepared to respond to calamities such as the COVID-19 pandemic.

The pandemic may have influenced these tendencies as consumers used their government stimulus checks to pay off debt.

8. Most Americans turn to personal loans or lines of credit when they can't use their credit card.

(NerdWallet)

When credit cards aren't an option, Americans look into a variety of other options for financing. Personal lines of credit are considered by 34% of customers, while personal loans through credit unions or banks are considered by 32%.

A 401(k) loan would be preferred over a credit card by 30% of consumers, while a personal loan via a P2P site would be chosen by 26%. Payday and title loans were the top choices for 25% of consumers, while 23% said they'd consider loans from a friend or loved one, home equity credit, or point-of-sale loans.

9. 6 million people in the US applied for credit cards in March 2021.

(Equifax) (Diary of Consumer Payment Choice)

That is up from 4.54 million in March 2020. At the same time, spending increased, with US retail sales going up by 11% between 2020 and 2021.

Experts believe consumers will spend more in the future due to increased optimism about the economy and fewer restrictions since the COVID pandemic in 2020. Consumers are becoming more comfortable using credit cards as the economy gradually improves.

10. In 2018, $430 billion was spent on business credit cards.

(Forbes)

That’s about $1 out of every $6 spent on general-purpose credit cards. According to stats on the best business credit cards, 67% of small-business owners have one despite only 24% of those professionals using them for business expenses.

As more and more business owners learn how to get a business credit card, 31% say they use them as a source of capital, and 29% say they use business credit card rewards to pay off their business expenses.

11. There were 2.8 billion credit cards in use in 2021.

(Processing Shift)

1.06 billion of those were used in the United States. In 2008, credit card issuers gave out 1.49 billion cards in the United States. In 2000, 1.43 billion cards circulated in the US. In contrast, between 2000 and 2008, the number only increased by 0.06 billion.

12. Approximately 10.8 billion smart chip cards were deployed globally in 2021.

(EmVCo)

Between January 2021 and December 2021, around 73% of card-present transactions in the United States were EMV (cards embedded with a microchip). Contactless cards are another technology that is expected to gain traction in the future. The pandemic has piqued consumers' interest in the technology, as they seek ways to limit their physical contact with others.

Nearly 65% of consumers said they would prefer to use contactless payments as much as or more in the future than they do now, according to a credit card usage survey by Visa released at the end of 2021. After the pandemic, only 16% said they would go back to non-contactless payments.

13. QR-code payment users are projected to surpass 2.2 billion by 2025, accounting for 29% of all mobile phone users worldwide.

(Forbes)

QR codes are used 70% of the time in China and only 8% in Japan. International adoption of QR codes for payment is expected to grow.

14. A contactless credit card's maximum limit is usually $250.

(American Bankers Association)

Contactless cards were available from 66% of credit card issuers in 2021. In the next one to three years, 25% of respondents planned to start issuing contactless cards.

15. Credit cards are used by nearly one-fifth of Americans to cover basic living expenses.

(The Motley Fool)

According to a survey of 1,000 credit card holders in the United States, 50% have maxed out their cards, and 23% plan to open another account to meet ends.

16. 710 is the average credit score in the US.

(Experian)

Experian reports that the average credit score in 2022 will be 710, up from 703 in 2021. The interest rate you pay on credit cards, loans, and mortgages is influenced by your credit score.

If your organization's credit score is low, you’ll need to learn how to build business credit fast to get better terms in the near future. However, you can still get the best business credit cards for bad credit if your company is in dire need of some funds.

17. In 2020, the average VantageScore soared to 688, which was a new high.

(Experian)

That represents a 6% increase from the previous year. The major US credit reporting agencies, Experian and TransUnion, collaborated to create VantageScore. The number ranges from 300 to 850 and is calculated using the same criteria as a FICO credit score.

Unlike a FICO credit score, which requires a credit history of at least six months, a VantageScore only requires a month of history and one account opened within the last two years. As a result, the latter is appropriate for millions of consumers looking to demonstrate how trustworthy they are before FICO can issue them a credit score.

18. One late payment can reduce your credit score by 100 points.

(Experian)

The day your credit card payment is due, credit card companies will charge you a late fee, and you should expect to receive emails, letters, and phone calls. On the other hand, your credit card issuer will not report your late payment to the credit bureaus until it is 30 days late or more.

Because missing monthly payments can severely harm your credit score, it's essential to keep this in mind. Someone with good credit can lose up to 100 points, whereas someone with bad credit will not be affected as much.

Because credit scores were created to predict the likelihood that you will repay your debts as agreed, your payment history is the most critical factor in determining your score. Missed or late payments send a message to credit card issuers that you may be unable to repay them, making it more difficult for you to obtain financing from any financial institution.

19. In 2021, the United States had 335 million VISA credit cards

(Statista)

According to personal finance statistics, more than 1.14 billion VISA credit cards were in circulation worldwide in 2021. There were also 200 million MasterCard credit cards in circulation in the US and 967 million worldwide.

Cash vs. Credit Card Spending Statistics

20. Consumers who pay with cash spend less money.

(Processing Shift)

When using cards, the average consumer spends $112. In comparison, the average cash transaction is only $22. Consumers spend nearly 83% more when using cards than cash. Despite the advantages of cash, around 70% of Americans prefer to pay with a card (credit or debit), citing ease as a reason.

21. US consumers prefer cash for minor purchases.

(New York Reserve Bank)

In 2021, small-value cash payments went down by 26%. That explains why people are less likely to utilize cash. According to reports, cash is primarily used for low-value purchases of products and services under $25. In addition, the average minimum payment using a card was $5.

22. Cash payments fell by 7% in 2021.

(PYMNTS)

That could be due to the COVID 19 pandemic, with many people doing their shopping online to avoid having to interact with others. Although debit cards remain the number one payment mode and with the rise of credit card ownership, cash is still not yet obsolete. In 2021, cash still accounted for 19% of all payments.

According to a credit card industry survey by PYMNTS.com, which took place from January 2021, 44% of consumers who primarily use cash have switched to other payment methods.

Credit cards are now preferred by 18% of these changers, while 16% use PayPal, which has no annual fee, and another 16% use various digital wallets.

23. In 2021, cash transactions decreased by seven percentage points.

(San Francisco Reserve Bank)

According to new trends, cashless payments are becoming the norm, and you may be wondering: How many business transactions are still done in cash?

Cash payments accounted for 19% of all transactions in the United States in 2021. That was a 7-percentage-point decrease from the previous year. As a result, the use of cash currency in the United States has decreased significantly.

According to a survey by the Fed, the average value of a cash transaction is $22, and that number more than doubles when it comes to credit card transactions.

24. Only 16% of Americans carry cash at all times.

(Travis Credit Union)

That indicates that society is moving toward a cashless future and the rising worldwide digital payments market. Some 27% indicated they carry cash most of the time, while 37% claimed they do so occasionally.

25. The average American carries $46 in cash.

(Travis Credit Union)

Small expenditures and an emergency are the two main reasons Americans carry cash. Surprisingly, while just 7% indicated they use it to manage their finances better, most respondents (62%) stated that paying with cash makes them less inclined to overspend.

26. Payment cards are preferred by 59% of consumers in the United States.

(Travis Credit Union)

According to research data from a survey by Travis Credit Union, credit and debit cards are the most popular payment method among Americans. Consumers prefer cash only 29% of the time.

People were also questioned about why they prefer payment cards. The ease and convenience of this payment method were mentioned by 54% of the study respondents.

27. Consumers make an average of 23 debit card payments monthly.

(Bank of Atlanta)

Consumers made an average of 18 credit or charge transactions and 14 cash purchases in a typical month in 2021. In addition, they wrote three checks and made eight direct bank transfers. The number of reported card payments remained constant from 220 to 2021 at 9 per month.

28. In the Southern USA, cash is king.

(Finder)

20% of Southerners prefer using cash most of the time. The Midwest isn't far behind, with 17.48%. The Northeast and the West are the following regions, with 15.81% and 14.29% of individuals preferring cash as a payment option, respectively.

29. As of June 2, 2021, cash amounting to $2.17 trillion is in circulation in the United States.

(Bank of America)

The amount of cash in circulation in the United States is increasing, although the digital payments market is also expanding. Take a look at the total amount of dollars circulating in the US in previous years:

- $2.09 trillion in 2020

- $1.79 trillion in 2019

- $1.67 trillion in 2018

- $1.57 trillion in 2017

- $1.46 trillion in 2016

- $1.38 trillion in 2015

- $1.3 trillion in 2014

- $1.2 trillion in 2013

- $1.13 trillion in 2012

- $1.03 trillion in 2011

- $0.94 trillion in 2010

- $0.89 trillion in 2009

- $0.85 trillion in 2008

- $0.79 trillion in 2007

- $0.78 trillion in 2006

- $0.76 trillion in 2005

30. 46% of US consumers often use their cashback cards.

(The Ascent)

Cashback cards are the most frequently used form of credit cards, followed by store cards. Store cards are cards that can only be used at a specific business. You may be eligible for discounts if you pay using this card. However, acquiring one is pointless if you don't go to the store often.

What about cashback cards? These are cards that you get a specific amount back every time you use your card. Let's say you spend $1,000 this month. If you receive 1% back, you will have ‘earned' $10. These types of cards usually have no annual fee, hence their popularity.

International Credit Card Statistics

31. 79% of American consumers own at least one credit card.

(Bank of Atlanta)

Here are the percentages of consumers who own at least one credit card from each country: Israel (75.10%), Canada (73.10%), Luxembourg (62.70%), Hong Kong (59.30%), New Zealand (58.30%), Australia (56.30%), United Kingdom (55.30%), Norway (54.20%), and South Korea (53.90%).

32. In January 2022, the UK saw 1.7 billion payment card transactions, up 42.8% from January 2021 and 9.2% from January 2020.

(Statista)

Contactless payments comprised 55% of all credit transactions and 69% of debit transactions. In January 2022, there were 1.2 billion contactless card transactions, up 78.7% from 645 million in January 2021 and 31.2% from 878 million in January 2020.

In January 2022, the total value of contactless transactions was £16.3 billion, up from £8 billion in January 2021 and £8.3 billion in January 2020, a 102.9% rise.

The number of contactless credit card transactions increased by 112.8% in January 2021 and 17.9% in January 2020. The number of contactless debit card transactions increased by 74.5% in January 2021 and 33.5% in January 2020, respectively.

Statistics on Credit Card Acceptance Rates

33. In 2021, 62% of consumers had at least one payment app.

(Bank of Atlanta)

According to credit card companies, consumers used PayPal 24.8% of the time, followed by Venmo (19.2%), and Zelle (12.6%)

34. American Express is the most wildly accepted credit card in the world.

(Spreedly)

In 2021, it had success rates of:

- 91% in Europe,

- 88% in the United States, and

- 89% in Latin America.

MasterCard and Visa both have 79% acceptance rates in the United States and 81% in Latin American countries. According to a study by Spreedly, Visa is more often accepted in Europe, with an 88% success rate, while MasterCard had an 85% success rate.

Credit Card Debt Statistics

35. The average credit card debt for US consumers is $5,313 per individual.

(Value Penguin)

Americans in the 100th annual income percentile have $5,313 in outstanding credit card debt. And when it comes to credit utilization rate, people often utilize 25.3% of their credit card limits.

Statistics show that the average consumer credit card balances in Canada and the UK are $4,154 and $3,245, respectively. The top five countries with the highest average revolving debt include Japan and Germany. Their relative averages are $2,900 and $2,052.

36. The average credit card balance is substantially lower than other types of debt among US consumers.

(Shift Processing)

The average mortgage debt in the United States is $148,060 and the student loan debt of $33,654.

37. The total revolving debt in the United States was $974.6 billion in February 2021.

(Bank of America)

This sum has increased from $992 billion in Q2 2020. However, in April, Americans' card balances were down from $1.07 trillion in Q1 2020. These numbers typically indicate that Americans are paying off their credit card debt.

The decline follows the global economic impact of the COVID-19 outbreak. As a result, it's more than likely that the loss of income played a role in the decline in credit card balances in the United States.

38. Alaska has the highest average credit card debt per consumer in the United States.

(Shift Processing)

According to statistics, the average debt per individual in this state is $7,726. Connecticut ($6,876), New Jersey ($6,881), and Virginia ($6,773) are the other leaders in this category. Iowa has the lowest average credit card debt ($4,622). Wisconsin's average credit card balance is $4,810, slightly more than the national average.

39. The highest credit card delinquency rate was in 2009 when it was 6.77%.

(Federal Reserve Bank of St. Louis) (Investopedia)

In Q2 of 2022, the delinquency rate was roughly 2.50%, which is low and sustainable. When a borrower misses two payments in a row and is 60 days late on a credit card loan, it is declared delinquent or overdue. The account is subject to credit card default rates if this is the case.

Over the last two years, the rate of credit card delinquency has decreased. The best outcomes have been seen in delinquencies of 90 days or more, which have been reduced by 63%.

In 2022, Millennials and Generation X have by far the most considerable credit card delinquency rates. The Silent Generation has the lowest likelihood of defaulting on their credit cards.

40. 25.2% is the average credit utilization rate in the US.

(Forbes)

Your credit card balances divided by your credit limits is the metric known as a credit utilization ratio. Your credit usage will be 10% if you have one credit card with a $1,000 balance and a $10,000 credit limit. Lower credit utilization is better for your credit score, and the consensus is that it should be kept below 30%.

At the same time, the average credit utilization for Gen Z, Millennials, and Gen X is around 30%. The average credit utilization for Baby Boomers and the Silent Generation is far lower.

41. Regarding average credit card debt by age, those aged 45 to 54 had the most significant amount.

(TheStreet)

On average, people in this age group owe $9,096. Americans between the ages of 55 and 64 owe more than $8,158 on average. Retired Americans have a credit card debt of more than $6,000.

42. Generation X is the generation with the most credit card debt.

(Gallup)

Traditionalists (those between the ages of 75 and 80) are credit cardholders with the lowest debt levels. Because of the Credit Card Act of 2009, the percentage of Americans with credit card debt is the lowest among Millennials.

The law made it more difficult for people under 21 to obtain a credit card. When applying for their first credit card, 27% of Gen Z consumers report they were denied, which is twice the rate of any other generation.

43. Credit cards (50%) were the most popular financial instrument among Gen Z.

(CreditCards.com)

Other financial instruments they used were college loans (39%), auto loans (25%), and unsecured personal loans (4%). Younger buyers prefer the convenience of Buy Now, Pay Later, with 44% of Gen Z and 37% of Millennials planning to use it in 2022, compared to 23% of Gen X and 9.4% of Baby Boomers.

While cash and debit cards are the most popular payment methods among all generations, Gen Z is open to non-traditional digital payment methods. More than any other generation, 53% use person-to-person payment apps, 50% use PayPal, and 25% are considering cryptocurrency.

For transactions between $30 and $150, 36% of Gen Z uses credit cards. 59% of Gen Z consumers with credit card debt are comfortable discussing it with their friends and family.

44. In 2022, the average credit card amount for Caucasians was around $7,000.

(CreditCards.com)

Latino's and African American's credit card debt was $6,066 and $5,784, respectively. The average African American citizen made a minimum payment of $368 using a credit, compared to $483 for the average Latino. For African Americans and Latinos, the average credit card APRs are greater.

45. Men, on average, have much more outstanding credit card debt than women.

(ValuePenguin) (BMO Harris Bank)

Female households generally had 22% less debt than their male counterparts. Women are more likely than men never to carry their credit card bills over to the next month.

According to a survey by Harris Bank, a popular credit card issuer, 35% of women consider credit card debt a big financial problem, while only 22% of men do.

46. Credit card debt is most common in consumers in the $40,000 to $80,000 salary range (48%).

(CreditCards.com)

Furthermore, if you earn more than $80,000 per year, you are more likely to have credit card debt than if you earn less than $40,000 per year. Credit card debt is common among Americans earning less than $35,000 annually.

The average debt increases with earnings, according to national credit card debt figures. Examine the following averages by income level:

- More than $290,000: $12,600

- $152,000 to $290,999:$9,780

- $95,000 to $151,999: $6,990

- $59,000 to $94,999: $4,910

- $35,000 to $58,999: $4,650

- $34,999 or less: $3,830

47. 29% of credit card users make minimum or low debt payments monthly.

(National Bureau of Economic Research)

People with earnings of more than $150,000 are the most likely to pay off their credit card amount in total, but only 38% of the time do they make minimal or low payments. Consumers earning less than $50,000 a year make modest payments 50% of the time.

48. Almost two-thirds of Americans (64%) believe they will be debt-free in ten years.

(CreditCards.com)

Around 48% predict it will happen in the next five years, with a lucky 14% expecting to be debt-free in only one year.

49. The average credit debt among American consumers with less than a high school diploma is the lowest.

(The Motley Fool)

The average credit card balance in the United States varies by education level:

- $3,390 if you don't have a high school diploma.

- $4,940 for a high school diploma.

- $6,210 for a college education

- $7,940 for a college diploma.

Credit Card Fees, APR, and Interest Rates

50. In the first quarter of 2022, the average credit card APR was 18.32%.

(The Motley Fool)

Wells Fargo is a credit card company with the longest 0% introductory APR, offering 21 months of interest-free credit card debt transfers. The percentage quickly jumps to between 13.24% and 25.24% after that.

38% of credit card firms polled by The Motley Fool charged penalty rates and balance transfers. The highest penalty rate for defaulting on a payment is 29.99%. Customers with strong or excellent credit have an average APR of 19.53%, while those with weak to fair credit have an average APR of 23.68%.

A travel rewards card's average annual percentage rate (APR) is 19.75%. Compared to the previous year, the average APR for student credit card offers climbed the most, climbing 95 basis points from 15.38% in Q1 2021 to 16.33% in Q1 2022.

51. The average annual fee for a credit card is $21.94, up 14% from 2021.

(Experian)

The average interest rate and balance transfer charge on a credit card is 2.44%. These have dropped 9.29% from the previous quarter and nearly 20% from the prior year. Interest rates on credit cards differ from one card to the next and month to month. The average rate for all cards in 2021 was 14.6%.

According to the Federal Reserve's monthly Consumer Credit Report, 16.45% is the average charge for consumers with a balance. Although the Fed does not determine the rates consumers pay for credit or other loans, it alters specific bank rates, which can indirectly affect consumer rates.

This year, consumer rates may rise more as the Federal Open Market Committee raises its benchmark federal funds rate.

52. The average percentage of accounts 90 to 180 days delinquent decreased by 53% between 2019 and 2020.

(Experian)

Accounts 60 to 89 days delinquent declined by 36%, while those 30–59 days past due dropped by 37%. For a variety of factors, revolving debt dropped in 2020. Due to COVID-19 limits and safety concerns, Americans spent less on travel, dining out, and other consumer activities.

Simultaneously, the Fed provided financial assistance in the form of immediate relief payments and unemployment benefits for millions of people who lost their jobs due to the pandemic.

53. There aren't any requirements for grace periods.

(Experian)

Most credit card companies provide interest-free grace periods, which give you a set amount of time to pay off your balance or balance transfers without incurring interest charges. However, some don’t offer grace periods since they are not required by law.

The legislation stipulates that if a credit card offers a grace period, it must last at least 21 days, although it does not require all issuers. That is one of the many reasons why reading the card's terms and conditions before signing up is essential.

COVID-19 Credit Card Statistics

54. Subprime credit card originations fell from 2.53 million in the first quarter to 1.84 million in the second quarter of 2020.

(TransUnion)

Lenders may have tightened their lending conditions due to the COVID-19 pandemic. In the third quarter, however, they rebounded, reaching 2.80 million subprime credit card originations.

55. The number of consumers with credit cards declined in 2020.

(TransUnion) (Experian)

There were 452.8 million card accounts in the fourth quarter of 2020. However, according to TransUnion, the number of funds increased to 454.6 million in the first quarter of 2021.

Experian data, on the other hand, shows that Americans coped well with the pandemic, at least in terms of their credit.

Credit card users' average VantageScore increased from 682 in 2019 to 688 in 2020. Credit card balances declined from $6,629 in 2019 to $5,897 in 2021.

56. At the start of the COVID-19 pandemic, over half of all individuals in the United States (47%) had credit card debt.

(CreditCards.com)

Most people's circumstances deteriorated dramatically during the pandemic, so we can safely conclude we've passed the 50% mark.

57. The average credit card debt load was over 13% lower in March 2021 than the previous year.

(Experian)

Experian reported a $968 decrease in the average credit card amount from before COVID-19 to $5,525 after COVID-19. The rate of delinquency has also decreased. Credit account firms' support efforts during the pandemic may have had a role in helping cardholders avoid delinquencies.

In April 2020, 2% of open credit card accounts began reporting for help. For most, cardholders did not require assistance programs for long periods. In May 2020, around 0.8% of credit card accounts switched out of assistance, and another 1.1 percent transitioned out in June 2020.

58. The average number of card accounts with payments 30 days past due fell to 1.67% in 2021, down from 1.82% in 2020.

(Experian)

Even though the pandemic strained the US economy and individual consumers, it did not increase credit card default rates and balance transfers. In 2020, consumers also did well in building credit and improving their credit scores.

According to FICO, the average score increased by one point per year until 2020, when it increased by seven points to 710 from 703. The previous highest rise was 3.8 points between 2015 and 2016.

59. Since the beginning of the pandemic, one out of every five cardholders reported that the limit on one or more of their credit cards had been reduced.

(NerdWallet)

Consumers (51%) with a reduced credit limit now use a different card they already had more frequently. More than a third of Americans whose credit limits were reduced due to the pandemics say they will use credit cards less and save more cash if their limits are reduced again.

Credit Card Fraud Statistics

60. For the past few years, credit card-related identity theft has been rising.

(FTC)

Fraud stats reveal that the situation has gotten worse over time. In 2015, there were far fewer ID theft reports, with only 74,902 linked to credit cards. Over the next three years, this figure more than doubled. There were 124,514, 133,096, and 157,715 credit card fraud reports in 2016, 2017, and 2018.

61. In 2021, new account fraud grew by 48%.

(FTC)

There were 365,597 fraud reports in this study. According to the most recent identity theft statistics, impersonation (29.39) was the most common type of fraud. Card fraud is one of the most common subcategories of ID theft, second only to the theft of government credentials or benefits. Scammers also target wire transfers, which have accounted for 56,811 of the 250,678 fraud reports with a payment method, resulting in $311 million in damages.

62. The most prevalent victims of card fraud are Americans aged 30-39.

(New York Federal Reserve Bank)

There were 110,952 reports in this age bracket, more than any other category. According to new statistics, persons aged 40 to 49 were the second most prevalent victims of credit card fraud. In 2020, there were 78,612 reports. Consumers aged 20-29, 50-59, and 60-69 reported 65,779, 45,175, and 21,634 occurrences of credit card theft, respectively. Among Americans aged 19 and under, credit card fraud was the least common (2,186 cases).

63. The United States accounts for 35.8% of all card payment fraud losses.

(Nilson Report)

The US accounts for more than a third of all losses, or $10.24 billion. No other country in the world suffers such significant losses as the United States due to credit card fraud. That increased from $9.62 billion in 2020 when the US was responsible for 33.58% of global fraud.

Experts studying this trend say the increased use of card-not-present (CNP) transactions in the United States has increased fraud. These digital purchases, which have been rising since the COVID-19 pandemic, have resulted in significant losses. According to estimates, every $1 spent on CNP fraud costs merchants in the United States $3.36.

64. Credit card fraud costs the average American $311.

(Federal Trade Commission)

That figure represents the average. Some cases of card fraud involve much more significant sums of money. Keep in mind that the number of credit cards in the United States is over 190 million. And debt in the United States has now surpassed $1 trillion. So, while the average amount stolen isn't as large as in other types of scams, there's still a lot to steal!

65. Payment card fraud will cost the world over $28.5 billion in 2021.

(Nilson Report)

That slightly decreased from the previous year's figure of $28.65 billion. The figure is alarming, and for financial institutions, the worst is yet to come.

As more people accept credit cards, the risk of becoming a victim grows. However, existing account fraud is only one of the issues. Experts warn that new account fraud is rising, with criminals registering new accounts using stolen personal information.

66. Creating a new account with stolen data has increased 48% in just a year.

(Federal Trade Commission)

Not only is it prevalent to create new accounts with stolen data, but it's also growing at an alarming rate. On the other hand, using stolen credit cards on ATMs increased by only 9%.

67. By 2030, gross losses from card fraud transactions are forecasted to exceed $49 billion.

(Nilson Report)

The total volume of all payment cards is expected to reach $79.14 trillion by 2030. In 2021, card fraud will cost the world $32.04 billion. In the coming years, that number is expected to skyrocket. Card fraud is expected to cost the global economy $38.5 billion by 2027 as the average number of credit cards increases.

68. In 2021, approximately 1 in 4 digital interactions was a fraud attempt.

(Arkose Labs)

According to a recent study, fraud attempts will account for 22.9% of all digital interactions in 2021. The research also shows that more criminals target American cardholders than in any other country. More than 1.3 billion of the 4.4 billion fraud attacks originated in the United States.

69. In 2021, $6.81 of every $100 spent with a bank card was stolen.

(Nilson Report)

The figure for 2021 is slightly higher than the 6.78 cents per $100 figure from the previous year. Card fraud in the US was 10.89 cents per $100 in 2021 and 10.25 cents in 2020.

70. In 2021, the most common card fraud loss was between $1 and $1,000.

(Federal Trade Commission)

Of 526,007 reported cases in 2021, the most common card fraud loss was between $1 and $1,000. Almost 50% were for losses ranging from $1 to $100. The lowest reported cases were in the $8,000 to $9,000 range (3,451). However, there were 39,734 losses over $10,000. That is a sizable proportion of the total number of reports.

71. Stolen credit card information can cost as little as $5 on the black market.

(Forbes)

Because card fraud is rising, stolen data costs continue to fall. A single consumer's stolen credit information card can sell for anywhere between $5 and $150, depending on how much supplementary data is included.

72. Card-not-present fraud is projected to cost retailers close to $130 million between 2018 and 2023.

(Juniper Research)

One of the most common types of credit card fraud is remote fraud. Because scammers don't require physical access to a credit card, it's growing increasingly popular. They can buy card information on the dark web or obtain it through phishing.

73. The travel, hospitality, and retail industries target 63% of credential stuffing attacks.

(Akamai)

Attackers often target customers' names, emails, social security numbers, CVV codes, card numbers, and other personal information they can utilize later.

74. Around 11% of credit card holders use “1234” as their PIN.

(Mashable)

I'm sure you're thinking something along those lines of “that can't be true,” – right? Unfortunately, it was true in 2012, when a study by Mashable was carried out. According to the results, 1 out of 10 people uses the PIN code “1234“.

We don't think we need to elaborate on how bad of an idea that is. The number “1234” is easy to guess and easily leads to fraudsters wiping out your money. A word of advice: don't pick a PIN code that's easy to guess, like:

- 0000

- 1111

- 1234

- 2468

- Easy-to-figure-out combinations

- Your birth year

Skimming is still common these days, too. So when you need money, keep an eye out for strangers at the ATM, or else you’ll land yourself on the list of credit card skimming statistics.

Statistics on Credit Card Rewards

75. Consumers consider loyalty points the most crucial element when choosing the card they want.

(TSYS)

According to a survey by TSYS, when asked what reasons influence their decision to use one credit card over another, most respondents (79%) cited loyalty rewards programs.

Card brand and finance charges were chosen as critical elements by 55% and 67% of respondents, respectively. Other crucial considerations included mobile capabilities, balance transfer alternatives, customer service, and flexibility. Only 12% of shoppers stated card design influences their purchasing decisions.

76. The most popular credit card reward is cashback.

(TSYS)

According to credit card stats, around 73% of customers like and have used cashback perks, including discounts and no annual fees.

77. More than 17% of travel rewards card holders put their credit card expenditures on their travel rewards cards.

(Forbes)

However, 19% of travel rewards card holders don’t use their travel rewards card for any of their card purchases. Since 2020, 39% of travelers have used a cashback card more frequently than their travel rewards card.

78. The average number of points/miles Americans save using travel reward cards is 64,800.

(Forbes)

66% of travelers with travel rewards cards have fewer than 10,000 points/miles, while 25% have 50,000 or more. Since 2020, 14% of travel rewards cardholders have opened a new travel rewards card account.

Statistics on Cryptocurrency Credit Cards

79. Although 82% of credit card holders are not interested in crypto incentives, 13% would want the choice, and 5% are interested.

(Forbes)

Only a tiny percentage of American adults have a card that allows them to earn some cryptocurrency, indicating that customers in the United States are slow to accept cryptocurrency credit cards.

80. Customers used Visa's crypto-linked cards to make $2.5 billion in payments in the first quarter of 2022.

(TSYS)

People use their crypto-linked cards to pay in various ways – retail products and services, travel, and restaurants. As part of a push for digital currency acceptance, Visa has launched a crypto consultancy service and invested in crypto platforms.

That accounted for 70% of the company's total crypto volume in the fiscal year 2021. BlockFi, Circle, and Coinbase are among the companies that have joined the payments company's network of crypto wallet partners, which has grown from 54 to more than 65.

The number of shops that accept cryptocurrency as payment has also increased to around 100 million. Visa announced in July that crypto-linked card usage had hit $1 billion in the first half of 2021.

81. Crypto-rewards credit cards are on the rise.

(Forbes)

Although they may appear odd at first glance, crypto-rewards credit cards are essentially the same as most standard rewards credit cards. Transactions are processed through the world's top payment processing networks, such as MasterCard, Visa, and others, just as they are with the majority of credit cards in circulation.

While some credit cards give you cash back or airline miles, crypto credit cards can provide you with Bitcoin, Ethereum, and other cryptocurrencies as a reward.

Grow Your Business With Credit Cards

These insightful credit card statistics show how consumers value credit cards for their benefits and convenience. Regarding industry developments, users can expect to see the rise of contactless cards, which have an ever-increasing market presence.

To get a slice of the credit card boom, you’ll need to choose one of the best of the best credit card processing companies to help process payments from your customers.

- Merchant One is the best merchant solution with loads of credit card processing services like mobile payments, virtual terminal transactions, and POS systems. The company has been around since 2002 and currently serves over 100,000 customers.

- Square is the best mobile credit card processor for small businesses, as it doesn't have monthly fees. It’s easy to use, and different companies can enjoy its services.

- Helcim is best for businesses that accept global payments. The card processor provides powerful features that allow you to accept mobile, eCommerce, and in-person payments. Unlike its competitors, Helcim has no binding contract or termination fees.

Editorial Disclosure. The info on this post is not from any bank advertiser, nor has it been reviewed or approved by them. We’ve made every reasonable effort to maintain accurate information. Check the bank’s own proprietary website rules for current info on the applicants’ credit approval terms, card rates, and fees.

Sources

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.