15 Best Credit Card Payment Processing Companies of 2025

The ability to accept credit card payments can make or break a business. Today, credit card processing is an integral part of business activities, both online and offline. Businesses depend on credit card processors to expedite card transactions.

A credit card processor is responsible for verifying, accepting, or declining transactions, securely transmitting data, and transferring payments to the merchant account. All this happens in seconds.

Choosing and integrating the right credit card processing company is essential to ease transactions for goods and services through credit and debit cards. The best credit card processing for small businesses offers flexibility to grow and merchant services.

Different businesses require different credit card processors’ services, depending on e-commerce or in-store capabilities and sales volume.

The best credit card processors provide transparent pricing, approve you in days, never require long-term contracts, and offer next-day ongoing transaction funding. To establish the best credit card processing companies of 2021, we reviewed 15 providers.

What is the Best Credit Card Payment Processing Company?

- Merchant One

- Square Payments

- Helcim

- Flagship Merchant Services

- Fiserv

- Payment Depot

- QuickBook Payments

- Fattmerchant

- PaymentCloud

- National Processing

- Dharma Merchant Services

- PayPal

- TSYS

- FIS

- Stripe

1. Merchant One

Best merchant solution with a suite for credit card processing services, including POS systems, virtual terminal transactions, and mobile payments.

Merchant One provides comprehensive credit card processing services and hardware suitable for many businesses. It was established in 2002, and its headquarters is in Miami Beach, Florida. Merchant One serves a little over 100,000 customers.

As a mid-sized card processor, Merchant One is among the largest resellers of Fiserv. So, it uses the Fiserv back-end processor to provide you other Fiserv products and services, including the famous Clover line of terminals and POS systems.

Merchant One offers primary credit card terminals, i.e., Pax S500, First Data FD-130, VeriFone VX520, and Pax S80 models. The models support NFC, and EMV-based payments save for Pax S500. You get these free with your merchant account.

The Fiserv reseller also offers a full suite of Clover POS systems that include Clover Station and Clover Mini. However, you’ll have to purchase these outright since they’re not part of the company’s terminal placement program.

Over the years, Merchant One reputation has had its highs and lows. Although it isn’t terrific, it seems to be consistent with other mid-sized merchant services providers.

Pricing

Merchant One does not reveal any pricing details about account fees or processing fees on its website. Prices are negotiable in the service industry. So, if you get in touch with Merchant One, expect a custom quote for your business.

It provides tiered pricing as well as interchange-plus processing rate plans. Some reports indicate that Merchant One monthly fees could be as low as $6.95.

Pros

- Provide a complete suite of POS systems and Clover terminals

- No equipment leases

- No automatic renewal

- Avails interchange-plus pricing

Cons

- Standard 3-year contract

- At least $295 early termination fee

- A lot of poor customer service complaints

2. Square Payments

Best mobile credit card processor for small businesses without a monthly fee

Square provides a quick and easy way of accepting credit card payments anywhere, anytime. Founded in 2009, Square is a card processing company that focuses on making it easy and affordable for businesses to accept digital payments.

It supports card processing for various businesses, including retail shops, e-commerce, and restaurants. Besides, it doesn’t require you to sign a long-term contract, eases funding with next-day transfers, and offers predictable pricing.

Square lets you use its POS apps or integrate Square Payments with other POS systems such as Lavu, TouchBistro, and Vend. It even integrates with numerous shopping cart software providers. You can also use Square APIs for custom setup.

With Square, deposits get into your merchant bank account in 1 to 2 business days. However, you can opt for a same-day or instant deposit for 1.5% of the transfer amount.

The Square Card launch, a Mastercard debit card, gives you instant access to your funds without a bank transfer.

Pricing

Predictable pricing is one reason businesses use Square credit card processor. The card processor charges a consistent flat rate, irrespective of your industry, transaction size, or card type. Square payment doesn’t charge more for American Express transactions.

With Square’s pay-as-you-go system, small businesses that ordinarily won’t afford a merchant account can accept credit and debit cards. Basic processing rates & fees range from 2.6% + $0.10 to 3.5% + $0.15. Square Payments also provides optional monthly plans.

Pros

- No monthly fees

- Predictable pricing

- All-in-one payment solution

- Perfect for small merchants

Cons

- Not ideal for high-risk industries

- Account stability problems

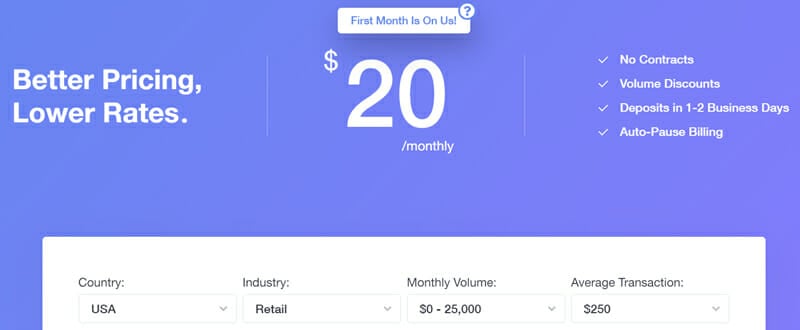

3. Helcim

Best for international businesses that accept global payments

There is plenty to like about Helcim. Unlike most merchant services providers, the credit card processor provides exclusive interchange-plus pricing, no binding contracts, low account fees, and good customer service.

Helcim offers strong and comprehensive features that allow you to accept in-person, e-commerce, and mobile payments. Its international payments feature enables you to accept global payments through its built-in options.

The card payment brands will deal with cross-border fees and currency conversions for you. With Helcim Card Reader, you get a mobile and counter-top friendly card reader that accepts payments from popular credit cards.

The credit card processor lets you accept American Express, Mastercard, Visa, JCB, Discover, Google Pay, PIN debit, and Apple Pay contactless payments. The credit card processing provider is fully EMV-compliant and offers NFC options.

You can also accept payments through a tablet, mobile, or by turning your desktop to POS using Helcim Card Reader. The card processor, through its hosted payment pages, lets you accept payments on an existing website without programming.

Helcim allows you to integrate dozens of third-party software.

Pricing

With Helcim credit card processing, every merchant has an interchange-plus pricing plan. Most credit card processors don’t provide interchange-plus while others fail to advertise it. Helcim provides high discounts for high-volume businesses.

For businesses processing up to $25,000 worth of transactions per month

- Swipped/NFC/EMV payments: 0.30% + $0.08

- Keyed-in & Online Payments: 0.50% + $.0.25

Helcim interchange-plus charge for business processing $25,001 – $50,000 per month

- Swipped/NFC/EMV payments: 0.25% + $0.07

- Keyed-in & Online Payments: 0.45% + $.0.20

Helcim interchange-plus rates for businesses processing $50,001 – $100,000 per month

- Swipped/NFC/EMV payments: 0.20% + $0.07

- Keyed-in & Online Payments: 0.40% + $.0.20

Also, there is hardware costs divided into Helcim Card Reader ($199/unit) and Countertop Stand ($39/unit)

Pros

- No contract or termination fees

- Excellent customer service

- Transparent account fees

- Accepts international payments

- Exclusive interchange-plus rates

Cons

- Monthly fee

- Not ideal for high-risk business

The recurring SaaS fee for Helcim is $20/month but Helcim is currently waving the first three months. The waiver extends indefinitely for approved nonprofits.

4. Flagship Merchant Services

Best merchant services provider with products and services that support retail, eCommerce, and mobile businesses

Flagship Merchant Services is among the most appealing credit card processing providers. Thanks in part for being one of the first credit card processing for small business providers to wave setup, termination, and application fees.

Flagship Merchant Services is a credit card processing reseller of First Data and Paysafe (initially iPayment). Since its launch in 2001, the company has grown rapidly over the past ten years.

With Flagship Merchant Services, you get access to merchant services like a virtual terminal, payment gateway, online reporting, and fraud protection, among others. It provides you with various payment solutions for online e-commerce, retail stores, and restaurants.

Flagship Merchant Services will provide you with one free credit card terminal for the initial account setup if you are a retail merchant. The company offers Verifone VX 520 terminal that supports EMV and NFC payments.

For those who wish to purchase terminals, Flagship Merchant Services will re-program them for free during your initial account setup. For e-commerce, Flagship lets you choose from Authorize.Net payment gateway or their proprietary Quiq gateway service.

To make it easy to accept payments on-the-go, Flagship provides you with iPayment’s card reader and MobilePay app. The MobilePay app is available for Android and iOS devices and includes an EMV-compliant card reader.

Pricing

You won’t find much detail on the company website about its fees and rates. The only way you can get information about its plan is by contacting the company to receive a personalized quote. Flagship provides tiered and interchange-plus pricing plans.

Pros

- No gateway setup charges

- No early termination fees

- No application or setup fees

Cons

- Limited pricing details

- Many public complaints

5. Fiserv

Best retail credit card processor for average to large businesses

Unlike many merchant service providers, Fiserv is a direct Mastercard and Visa processor. Fiserv relies mainly on partnerships with resellers and sub-ISOs to sell its credit card processing service. It even includes incentives to veterans and accepts Alipay payments.

The two biggest resellers include large banks in the US, Bank of America Merchant Services and Wells Fargo Merchant Services. The two partnerships, coupled with thousands of others, establish Fiserv as one of the leading global credit card processors.

Fiserv processes approximately 45% of credit card sales in the U.S. Fiserv supports businesses of different sizes across almost every industry, including professional services, retail, food, and beverage.

So, you don’t have to worry regardless of whether your business is a startup or a multinational corporation. It is available in 118 countries, and its credit card processing services serve over 6 million business locations.

Also, Fiserv owns Clover POS systems sold by over 3,000 Fiserv resellers in the US. With Fiserv, you can accept payments from different channels offline, online, through mobile, and on-the-go.

Pricing

Fiserv does not provide pricing details on its website, which is an inconvenience for merchants shopping for better deals. However, it is a common practice in the credit card processing industry. You can contact the credit card processor for a custom quote.

Pros

- Ideal for high-volume merchants

- Multiple payment processing options

- EMV and PCI compliant

- Supports Clover credit card processing

Cons

- Many negative reviews

- Early termination fee

6. Payment Depot

Great for low-risk businesses in the US looking for transparent pricing

Payment Depot covers all the bases with its features to ensure your business can accept credit card payments. However, it only offers its services in the US.

Payment Depot has a partnership with two of the biggest credit card processors, i.e., Fiserv and TSYS (part of Global Payments). With Payment Depot, you can integrate payment gateways like Authorize.Net and others on your eCommerce website.

The credit card processor includes a free virtual terminal with each pricing plan. It allows you to use your computer as a credit card terminal. As one of Fiserv resellers, Payment Depot provides the popular Clover POS systems.

Also, you get access to a suite of standard counters from vendors such as Dejavoo and Ingenico. All the models’ Payment Depot supports can accept magstripe, NFC-based, and EMV payment methods.

Also, in line with emerging trends in the credit card processing industry, Payment Depot offers you ‘smart’ terminals with touchscreens. The credit processor currently provides Poynt Smart terminal, Clover Flex, and the Smart Terminals Vital Plus.

Through the partnership with SwipeSimple, Payment Depot allows you to use its iOS and Android mobile app and card reader. The platform also provides ACH (e-check) processing, developer tools for web designers, and online shopping cart integration.

Pricing

Payment depot is a credit card processor popular for pioneering subscription pricing or membership pricing to reduce merchant processing fees and costs. It offers four pricing plans designed to meet specific merchant needs.

- The Basic membership plan attracts $49/month, interchange + $0.15/transaction, up to $25,000/month

- The Most Popular Membership plan starts from $79/month, interchange + 0% + $0.10/transaction, up to $75,000/month, and other perks

- The Premier Membership plan attracts $99/month, interchange + 0% + $0.07 per transaction, up to $150,000/month processing volume, among other features

- The Unlimited Membership plan starts from $199/month, interchange + 0% + $0.05/transaction, unlimited processing volume, and much more

Pros

- Transparent pricing

- No setup or application fees

- Free virtual terminal and gateway

- Great customer support

Cons

- Supports only US-based merchants

- Not good for low-volume businesses

7. QuickBook Payments

Best credit card processing for businesses that use QuickBooks for accounting

QuickBooks Payment credit card processor is designed for businesses that use QuickBooks for accounting. It helps you manage everything in one app by connecting your payment accounts with QuickBooks. QuickBooks Payment allows you to accept swiped transactions.

You can rely on a USB-connected swiper to your computer for payments. Also, you get the option of accepting payments through iOS and Android apps. With QuickBooks Payment, you can bring any credit card processor into Intuit’s POS system.

However, only QuickBooks Payments can integrate seamlessly without the need to enter transaction data. Bundling QuickBooks Payments in your business is a great choice if you already use QuickBooks and POS.

You won’t get as many features and hardware choices as traditional merchants if you operate an online store. QuickBooks Payment is compatible with Big Commerce and Shopify. The two platforms are great if you need credit card processing for your small business.

Besides, with QuickBooks GoPayment, you can accept payments through a tablet or smartphone.

Pricing

QuickBooks Payments discloses most of its prices on the Intuit website. But each variation has its own pricing with subtle differences. So, you will need to do your research to know the exact fees for your account.

In general, the processing fee plans are flat-rate, but some plans differentiate between non-qualified and qualified rates, which is a hallmark of tiered pricing. The flat rate applies per transaction but processing over $7,500/month makes you eligible for custom processing rates.

Here are the rates per transaction for Mastercard, Visa, American Express, Discover, and Apple Pay.

- ACH bank transfers – 1%(capped at $10)

- Card Swiped – 2.4% + $0.25

- Card Invoiced – 2.9% + $0.25

- Card Keyed – 3.4% +$0.25

Pros

- Great professional services

- No monthly minimums

- Cheap chip card readers

- Seamless QuickBooks integration

- Predictable pricing

Cons

- High costs per transaction

- Inconsistent customer service

8. Fattmerchant

Ideal for high-volume businesses in the US looking for predictable pricing

Fattmerchant is a credit card processing company catering to the needs of various businesses through its subscription plus fixed-rate model. With this merchant services provider, you can customize your Fattmerchant account to accept payments in different ways.

It allows you to accept in-person transactions, online, virtual terminals, or mobile payments. However, the Fattmerchant is not for small businesses that make low-volume credit card transactions with less than $10,000/month.

It is a great option for growing companies that will eventually scale up. The credit card processor automatically accepts Discover, PIN Debit, American Express, MasterCard, and Visa.

Also, you can include other card types in your Fattmerchant merchant account, including Voyager, WEX, EBT, JCB Dining, and Health Flex. The Merchant services provider lets you receive payments in-person, mobile, or online.

It lets you process unlimited transactions per month. You get next-day payment processing with Fattmerchant, but you can opt for instant payment at a fee.

Pricing

Fattmerchant provides three plans, each with a monthly contract you can cancel at any time without cancellation fees.

- Its lowest plan caters to businesses that process up to $500,000/year. The plan attracts a $99/month fee per acceptance method like an online solution, card reader, a terminal.

- The second plan caters to businesses processing over $500,000/year and attracts a $199/month subscription fee.

- The enterprise plan deals with businesses that process over $5,000,000/year. Fattmerchant has a custom plan for enterprise clients. To get a quote, contact Fattmerchant directly.

Pros

- Transparent pricing

- 24/7 customer support

- Low transaction fees

- No cancellation fees

Cons

- High subscription fee

- Unfavorable for low-volume businesses

9. PaymentCloud

Best credit card processor for high-risk merchants

PaymentCloud is a merchant services provider that focuses on credit card processing for high-risk businesses. It provides a comprehensive service that includes payment and credit card processing in-store, online, gift cards, or checks.

Also, the credit card processor provides hardware and software to existing and new businesses. It is PCI-compliant to ensure you get complete protection against data breaches and fraudulent transactions.

PaymentCloud is a credit card processor for mail order/telephone order (MOTO), eCommerce, and other high-risk businesses. Although the merchant services provider serves brick-and-mortar and lower-risk establishments, it shines in high-risk businesses.

As a credit card processor for high-risk business, PaymentCloud isn’t a direct card processor. Rather, the processor partners with various processors and banks to increase your chances for approval and continuous account stability.

PaymentCloud prefers Authorize.Net payment gateway for online processing. The other option is USAePay. Its ACH & eCheck processing lets you process direct debit payment methods on your website.

Pricing

No pricing information is available on the PaymentCloud website. It is common for credit card processors serving high-risk sectors not to disclose such details. The pricing varies widely from one merchant to another depending on various factors.

However, PaymentCloud provides tiered and interchange pricing.

Pros

- Not setup fees

- Specializes in high-risk sectors

- Few customer complaints

- Free credit card terminal

Cons

- Pricing not transparent

10. National Processing

Best credit card processor for cost-conscious mid-sized to large businesses

National Processing primarily provides an electronic network for financial transactions. It can process a large volume of credit and debit card transactions. If you require a POS system, National Processing has a partnership with leading providers.

The merchant service offers secure payment processing through a terminal, tablet, online through a PC or smartphone. Although the credit card processor may not provide the extra bells and whistles you get from large providers, it is great at covering the basics.

National processing, like most credit card processors, is not a direct processor. It appears the company uses Fiserv exclusively as its back-end processor. While you get customer support in most cases, if your account is on hold, frozen, or terminated, you will deal directly with Fiserv.

National Processing exclusively offers terminal products from Clover. These accept NFC and EMV payment methods. Also, you get an affordable mobile processing system for your business with the Clover Go mPOS system.

Currently, the company supports eCommerce merchants through the partnership. Also, you get excellent ACH services from this processor through its proprietary ACH software.

Pricing

Unlike many credit card processors, National Processing provides a clear pricing plan on its website.

- For low-volume businesses, it breaks down the plans by primary sales channel with plans, including interchange-plus pricing.

- In the case of high-volume & very high-volume businesses, National Processing provides membership pricing that eliminates the percentage of markup per transaction.

Pros

- Great reputation online

- Ideal for budget-conscious merchants

- No long-term contract

- Provides membership and interchange-plus pricing

Cons

- Early termination fee for free equipment

- Free equipment may require a contract

11. Dharma Merchant Services

Best credit card processor for mid-to-large sized businesses and nonprofit organizations

With Dharma Merchant Services, you get a complete set of essential services and products for eCommerce and retail merchants. It uses Fiserv as its main back-end processor. Although Fiserv has a poor reputation among small businesses, Dharma offers a better deal.

Dharma offers you customer service, so you won’t have to deal with Fiserv directly. With MX Merchant, Dharma gives you an all-in-one account. It gives you access to features such as a virtual terminal, customer database, mobile processing app, and online reporting.

Also, Dharma Merchant Services offers you exclusive B2B processing at a discounted rate if you process level 2 and 3 data. Dharma provides eCommerce merchants with NMI Gateway and Authorize.Net.

You also get several countertop credit card terminals that support a direct sale. The terminals are EMV-compliant and include NFC-based payments like Apple Pay. Dharma can reprogram your terminal free of charge if you already own it.

Pricing

Dharma pricing is among the most transparent in the industry. The merchant services provider fully discloses all its costs on the website. It exclusively offers interchange-plus pricing to each merchant account.

The company reveals the cost of each fee and why Dharma charges you for it. Here are pricing options:

- Storefront (Retail) rate starts from $20/month, interchange + 0.15% + $0.07 per transaction, other incidental fees

- Virtual (eCommerce) rate attracts $20/month, interchange + 0.20% + $0.10 per transaction, other incidental fees

- Restaurant rate begins from $20/month, interchange + 0.15% + $0.07 per transaction, several incidental fees

- High-volume Retail rates apply to businesses with transactions over $100,000 per month. The fee includes $15/month, interchange + 0.10% + $0.05 per transaction, other incidental fees.

Pros

- No monthly minimum or annual fee

- Discounted price for approved nonprofit organizations

- Transparent pricing

- No early termination fees

Cons

- It doesn’t support international or high-risk merchants

- Not ideal for businesses that process less than $10,000/month

12. PayPal

Best for credit card processor for individuals and small businesses

PayPal is a big player in the credit card processing industry across the world. It claims 22 million merchants and 305 million active consumer accounts. PayPal provides a fast way of setting up your merchant account and getting started almost instantaneously.

If you process sporadically, have low volume, or are starting a business, PayPal should be on your list or merchant service providers. It is difficult to find better value if you are a new merchant. So, go for it, provided you get all the features you need.

PayPal is a third-party processor, also known as an aggregator or payment service provider (PSP). The problem with PSP over traditional merchant accounts is that you bear a high risk of account instability as a merchant.

PayPal provides you three options for online payments, i.e., PayPal Checkout, PayPal payments Standard, and PayPal Payments Pro. With PayPal Checkout, you can accept credit cards online by integrating PayPal with your eCommerce provider.

The PayPal Payment Standard plan gives you more customization and control over the payment process. With the PayPal Payments Pro, you get the most customizable online payment option, but it will cost you an extra $30 per month.

Pricing

PayPal doesn’t come with annual fees, setup fees, cancellation fees, or PCI compliance fees. Besides a few optional software fees, PayPal doesn’t require additional fees other than the payment processing fees.

PayPal is very transparent about its transaction costs even when the costs are higher compared to traditional merchant services. Some merchants will find the lack of extra fees cost-effective compared to the interchange-plus plan.

Below are the PayPal transaction fees, regardless of whether you opt for the Pro or Standard plan.

- Online sales attract a 2.9% + $0.30 fee per transaction

- Swiped/tapped/dipped in-store and mobile transactions attract a 2.7% fee

- Keyed-in mobile and in-store transactions cost 3.5% + $0.15

- Virtual terminal transactions cost 3.1% + $0.30 per transaction

- Mass payouts attract a 2% fee using an online form ($1 maximum) or $0.25 fee per payout on an API

Pros

- Extensive integration

- Trusted by consumers

- All-in-one payment solution

- Multiple pricing plans

- Great for low-volume merchants

Cons

- Not ideal for high-risk industries

- Account instability issues

13. TSYS

Best credit card processor for established merchants accepting payments from multiple sources

Total System Services (TSYS) is a credit/debit card processor and merchant service provider. The credit card processor serves clients in more than 80 countries across the world. Apart from being one of the oldest credit card processors, it is among the largest processors.

TSYS is second to Fiserv in terms of its annual processing volume. It specializes in backend credit card processing for ISO, companies that create and sell credit card processing, and non-acquiring banks. So, TSYS is a supplier to companies that sell credit card processing.

With TSYS, you get access to a complete set of products and services for eCommerce, omnichannel, and retail businesses. As a direct processor, TSYS helps you manage your merchant account and process transactions.

It makes it easy to deal with issues like account freezes and chargebacks. TSYS integrates other payment processing systems with its mobile, wireless, and countertop terminals that let you accept payments online or in-person using a credit card, debit card, or ACH.

Besides, TSYS provides various Ingenico and Verifone credit card machines and PIN pads. The models support NFC-based and EMV payment. You even get a virtual terminal that turns your laptop or desktop into a fully-kitted credit card terminal.

Pricing

After its acquisition by Global Payments, TSYS no longer shows pricing information on its website. To get a quote that includes processing fees, incidental fees, one-time, and recurring fees, you need to contact the company.

Although you won’t pay setup fees, you can expect to pay a monthly fee that ranges from $9.95 to $45. The amount you pay depends on the amount you process per month.

Pros

- Strong product lineup

- Few complaints

- Offers interchange-plus pricing

- Numerous integrations

Cons

- Hefty cancellation fee

- Hidden fees

14. FIS

Best direct credit card processor for small businesses

The 2018 merger of Vantiv and FIS resulted in FIS, one of the biggest credit card processors. Although it is a giant in the credit card processing industry, FIS works with small businesses alongside large corporations such as ISO processing companies and banks.

FIS gives you access to various credit card processing solutions. With FIS, you can create a merchant account that allows you to accept all the main credit and debit cards online, over the phone, in-store, or on-the-go.

You also get FIS Gateway Services that you can use to accept payments online and mobile transactions. The payment gateway supports over 300 international payments that allow your customers to buy online in their local currencies.

Such a consideration is important for an international e-commerce business. Also, FIS integrates with more than 1,000 software, so chances are it can integrate with your accounting software, POS, shopping carts, and e-commerce platforms.

Although FIS credit card processing does not resell POS systems, it integrates with hundreds of popular options such as Lightspeed, ShopKeep, and Vend.

Also, if you need to process payments on your computer, FIS offers you a virtual terminal that helps you accept credit cards, ACH payments and set up recurring payments. As well, access to a virtual terminal lets you use a mobile card reader on your tablet or smartphone.

Pricing

On its website, FIS doesn’t provide any information on pricing. So, you need to speak with a sales representative or request a pricing quote online. The credit card processor offers both interchange-plus and flat rates.

Pros

- Offers competitive pricing to small businesses

- Numerous integrations

- No termination fee if you give a 30-day notice

- Solid features

Cons

- Nontransparent fees

- One-year contract

15. Stripe

Best credit card processor for online-based businesses

Among all the merchant service providers, none is as popular for online payment processing as Stripe. It allows you to accept electronic credit card payments from your customers.

Stripe is a third-party credit card processor designed to make it easy for businesses to accept payments online. It helps you accept credit cards and offers industry-leading, impressive features. It supports almost any online business you have in mind.

Stripe processes online payments for large businesses like Lyft, Blue Apron, Under Armour, TaskRabbit, Wish, and Pinterest. With a huge array of clients, Stripe is among the big players in the industry. It is available in 36 countries and accepts payments in over 135 currencies.

Stripe gives you access to developer tools such as API that help you integrate Stripe in your e-commerce business. The card processor also accepts payments in-person and through mobile apps.

Pricing

The best thing about the pay-as-you-go processor is that it gives you a clear pricing structure. Stripe charges simple, flat rates for ACH and credit card transactions.

- Credit cards attract 2.9% + $0.30 per transaction

- ACH charges are 0.8% capped at $5

Stripe offers discounts for nonprofit and a plan for micropayment businesses.

Pros

- Multicurrency support

- Excellent tools

- Ideal for international merchants

- Predictable pricing

Cons

- Not ideal for high-risk business

- Requires technical skills

What is Credit Card Processing and How Does It Work?

Credit card processing enables businesses to securely receive payments made through credit, debit, gift, or even loyalty cards.

In the past, the ability to accept card-based sales involved a one-size-fits-all approach, characterized by complex configurations and long delays in the authorization. Today, multiple payment processing options exist, most of which meet specific business needs.

For instance, online credit card processors that an eCommerce merchant may consider are very different from merchant services for a brick-and-mortar retailer and vice versa.

Ultimately, variety in merchant services is a plus since business owners can locate the best payment solutions for their needs. The many options available can be overwhelming.

So, it is important to choose a trustworthy partner who can take you through the entire process – from choosing a credit card terminal to processing payments quickly and securely.

Parties Involved in Processing Credit Card Payments

Processing each credit card transaction occurs in seconds. All this is made possible through a seamless collaboration of 6 partakers.

- Customers/Cardholders– These are your customers who provide their credit card details as they make a purchase. Cardholders are categorized as either transactors or revolvers.

Transactors repay in full their credit card balance to avoid accruing interest and late fees. On the other hand, revolvers only repay a fraction of the credit card balance every month and pay interest on the rest. - Merchants – Accept payments through credit or debit cards for providing goods and services. During a purchase, merchants request payment by sending credit card details of the customer.

- Acquiring Bank – To process credit card transactions, merchants require a merchant account in an acquiring bank. The acquiring bank connects the cardholder’s bank to the merchant.

- Payment Processor – A credit card payment processor provides the infrastructure for merchants to accept credit card transactions. Through a terminal, payment processors send credit card details to the credit card network for approval.

- Credit Card Network – The main credit card networks are Visa, Mastercard, and Discover. These accept credit card payment information from acquiring processors.

The credit card network sends authorization requests to the cardholder’s issuing bank and transmits the responses to the payment processor. - Issuing Bank – The card-issuing bank is the bank that issued the customer/cardholder with a credit card. It is responsible for approving or denying payment requests based on the available balance of the cardholder.

How Credit Card Processing Works

Credit card processing is a fast and complex process. It involves the transfer of data between the cardholder’s bank and the merchant. It occurs in a matter of seconds once the customer swipes or taps their credit card.

Processing a credit card payment occurs in three steps: authorization, authentication, and funding/clearing. The authorization step takes place in seconds, but the authentication and funding steps occur within 24 hours.

Step 1: Credit Card Authorization

The payment authorization process starts when a customer presents their credit card to pay for goods and services. Swiping or scanning a credit card sends a payment authorization request from the payment processor or the acquiring bank.

- For in-store purchases, a customer pays through swiping, tapping (contactless), or dipping (EMV chip) cards. Also, they can use a digital wallet connected to their credit card, such as Apple Pay.

- The customer provides their credit card information in a payment form on a website or app for online payment.

- In the case of phone transactions, virtual terminals provide secure credit card processing.

The credit card terminal or website transmits the details of the cardholder, including the payment amount to the merchant’s credit card processor or acquiring bank.

The processor then forwards the information to the right credit card network (such as Visa or Mastercard), which, in return, passes it on to the customer’s issuing bank for authentication.

Suppose the cardholder is in good standing with the issuing bank and card association. In that case, all parties will get a notification that the transaction was successful, enabling the merchant to receive payment.

Step 2: Credit Card Authentication

In this step, the card-issuing bank establishes the validity of the credit card. To do so, it uses fraud protection tools like security codes such as CVV and Address Verification Service (AVS).

The credit card network sends payment authorization requests to the issuing bank. The card-issuing bank verifies the credit card number and checks the available funds. After the card-issuing bank approves or declines the transaction, it sends the response to the merchant.

Once the merchant is authorized, the card-issuing bank puts on hold the purchase amount on the customer’s account. The POS terminal collects authorized purchases for batch processing. The merchant then gives the cardholder a receipt to mark the end of a sale.

Step 3: Credit Card Clearing & Settlement

In this stage, clearing & settlement occur simultaneously as the transaction is posted on the customer’s credit card billing and merchant’s statement. A merchant sends a batch of approved authorizations at the closure of each business day to the credit card processor.

In return, the processor requests settlement by sending the batched details to the credit card network. The credit card network then sends each authorized transaction to the right card-issuing bank. It happens between 24 and 48 hours of the transaction.

Eventually, the card-issuing bank transfers the funds minus the interchange fee, with a portion going to the card network. Next, the card network will pay the acquiring bank/processing with the remaining funds.

Now, the acquiring bank credits the merchant account minus a merchant fee. Lastly, the issuing bank sends the transaction details to the customer’s account. The customer receives the statement and settles the bill.

Credit Card Processing Rates and Fees You Need to Know

Credit card transactions and fees are inseparable. The processing involves various parties besides a consumer and a merchant. Each player in credit card processing attracts a certain fee in different stages of credit card processing.

The fees pay banks and payment processors that do all the work. For instance, an interchange fee goes to acquiring and issuing banks. For the acquiring bank or processor, it applies before receiving payment where the processor takes a fee before depositing funds.

So, the merchant receives slightly less amount for sold goods and services. Interchange fees usually combine a one-time percentage of the sale and a transaction fee. These calculations differ depending on the credit card network.Also, recurring fees from acquiring banks are common.

Credit Card Processing models

Interchange-plus Pricing

Also known as cost-plus pricing, interchange-plus pricing includes a markup percentage to the interchange fee for every transaction. The markup pays the credit card processor.

With the interchange-plus pricing model, you will know what portion of your cost is going to the processor, regardless of the type of card you accept. Most industry experts endorse this pricing model as a cost-effective option for most small businesses.

Although most credit card processing companies offer interchange plus, the best processors provide it to all their customers. Keep this in mind since you may have to ask for it as most companies prefer to sign you up with tiered pricing.

Some companies also require you to meet specific requirements to be eligible to process cards using an interchange-plus rate. For instance, to qualify, your processors may require you to process a set dollar amount each month.

Flat-rate Pricing

The flat-rate pricing model is popular with mobile credit card processors. However, it usually isn't available from traditional credit card processors. It charges you a flat percentage of each transaction.

If you want simplicity, have small sales tickets, or process a low volume each month, check out flat-rate pricing. A variation of flat-rate sees some processors charge a flat rate and a per-transaction fee.

The percentage rate in these fees is lower compared to services that only charge a flat percentage. However, before choosing a payment plan, ensure you calculate which option is cost-effective for your business.

Tiered Pricing

Tiered pricing arranges pricing into tiers, setting a price for each tier. Usually, credit card processors have two to six pricing tiers, with separate tiers for credit and debit cards.

The standard tier structure includes three tiers for credit and debit cards.Usually, processors categorize them as “qualified,” “mid-qualified,” or “non-qualified.”

Instead of implying the validity of a credit card, the terms refer to the type of card and how to process and verify cards.

Recurring Credit Card Processing Fees

Apart from the standard fees you pay per transaction, most credit card processors charge maintenance fees. Nevertheless, the best credit card processors charge very few fees and no additional fees for processing mobile payments.

The usual credit card recurring fees include a PCI compliance fee, a monthly fee, and a gateway fee for those who accept online payments.

- Monthly fee: For preparing statements and providing customer services, some credit card processors charge a monthly fee commonly referred to as a statement fee. As well, others charge you an extra fee for sending you printed statements.

- Gateway fee: A gateway allows you to receive payments online. Some credit card processors have proprietary systems or collaborate with third-party providers. For the service, many credit card processors charge you a separate monthly fee.

- Monthly minimum fee: Today, some credit card processors set a minimum processing amount per month. Meanwhile, other processors set monthly minimum fees to ensure your merchant account is active before applying a fee on your transactions.

- Among all the credit card processors, the best processors only apply a charge only on the processing costs for the set monthly minimum. To avoid surprises, let the credit card processor inform you if this fee applies.

- PCI compliance fee: Merchants have regulations they have to follow in the credit card processing industry in order to process credit cards. The regulations are useful in preventing fraud and protecting businesses, customers, and credit card processing from security breaches. For this, you need to carry out a self-assessment questionnaire even though your business may need additional requirements. However, not all credit card processors charge this fee. Credit card processors charge it monthly, quarterly, or annually.

- PCI non-compliance fee: Credit card processors usually give you several months to comply. Failure to be PCI-compliant or reestablish compliance may attract a fine per month. The fine can be expensive and varies depending on the credit card processor.

- Batch fee: The nominal fee you pay for sending a batch of transactions. It usually happens once or twice on a business day. The nominal fee varies from 10 to 25 cents per transaction.

Incidental Credit Card Processing Fees

These fees only apply to transactions that qualify.

Address Verification Service (AVS) fee: It applies whenever the processor uses AVS to verify the cardholder’s billing address. The fraud-prevention tool is used when processing credit card payments online.

Voice authorization fee: Another fraud-prevention approach that charges a fee when the terminal requires voice authorization for a transaction to be successful. It is rare, but it charges you for each voice authorization.

Retrieval fee: The fee applies whenever a customer suspects a payment. So. their bank may require a copy of the receipt to verify the legitimacy of a purchase. It varies from one credit card processor to another.

Chargeback fee: Whenever a customer is unsatisfied with their purchase, they can cancel the order and request a return of their funds. For this, a chargeback fee is necessary to cater for the processing costs when crediting the account of the cardholder. A chargeback is common in e-commerce compared to traditional in-store businesses that accept credit cards. Also, a chargeback fee happens when the merchant’s name varies from your business name, which causes doubts in the customer.

Non-sufficient Funds (NSF) fee: If your business bank account has insufficient funds to pay credit card processing fees, the processor will place the NSF fee.

Credit Card Network Fees

All credit card processing networks place non-negotiable fees that, in return, get passed to you by your credit card processor. Some even overcharge you through a markup.

APF/NABU/Data Usage fees: All credit card network brands charge you usage fees. For Visa, the fee is known as Network Acquirer Processing Fee (APF), while Mastercard charges you a Network Access and Brand Usage (NABU) fee, and Discover places a Data Usage fee.

Cross-border fees: U.S.-based merchants pay a fee that caters for currency conversion if they accept international credit cards.

Nonstandard Credit Card Processing Fees to Avoid

Also, some credit card processors charge you miscellaneous fees. Try as much as possible to avoid these extra fees. The best processors do not charge you these fees. Usually, you can negotiate with the credit card processor to get rid of these nonstandard fees.

- Cancellation fee: Also known as an early termination fee, the fee applies whenever you cancel your credit card processor or lease equipment. To avoid paying a termination fee, select a credit card processor with a monthly subscription, and buy the credit card terminals.

- Annual fee: It is an annual merchant account maintenance. While the best credit card processors never charge annual fees, others online waive the charge for a year. So, choose a card processor that never charges you annual fees.

- IRS reporting fee: Also known as IRS regulatory fee. Your credit card processor will charge you this fee for sending you IRS 1099-K form. It applies if your business processes more than 200 transactions per year and more than $20,000.

- Some processors charge a fee for preparing and supplying this form. However, the best credit card processor won’t charge you this fee.

- Membership fee: Some credit card processors combine various standard fees to simplify their fees.

- Access fee: In case your credit card processor charges an access fee beside card network fees, let them clarify and, if possible, waive it.

Other Nonstandard Fees

- Audit fee

- Application fee

- Customer service fee

- EBT network access fee

- Excessive transaction fee

- Liquidated damages fee

- Next-day funding fee

- Online reporting fee

- Quarterly technology fee

How to Choose the Best Credit Card Payment Processing Provider?

The process of choosing the right credit card processor for your business is not easy. Like many other decisions, comparing your options is always wise. First, you should decide the kind of processor you need.

Once you understand where the business stands as well as its needs, take into account other general attributes. The attributes include aspects such as customer service, transparent pricing, PCI compliance, and features & integrations.

1. Merchant Account Provider or Third-Party Processor

Merchant Account Providers

Often, merchant service providers are suitable for growing or large businesses. These credit card processors are customizable and offer a stable solution for processing transactions in your network.

Some merchant service providers in credit card processing include Fattmerchant, Helcim, and Dharma Merchant Services. Merchant account providers offer cheaper costs per-transaction and give your business access to in-house customer support.

For some businesses, the underwriting process for approving your merchant account is a hindrance. Consider your business’s credit health since you may have to fill out an application similar to financing forms for your merchant account to be approved.

Besides considering the type of credit card processor, take into account your business goals. Also, consider the different types of transactions your business accepts (cash, mobile, or online) since the design of most credit card processors fit a certain format.

Third-Party Credit Card Processors

They are also known as payment aggregators and help merchants avoid signing up for merchant accounts. If you run a small business, then a third-party processor like Square or PayPal provides a simple and affordable way of processing payments.

Usually, you only pay third-party processors after making a sale. These credit card processors eliminate the need to comply with PCI-DSS because transactions take place outside your platform.

The main drawback is that third-party processors can hold your funds or terminate the business account for failure to comply with their terms.

2. Customer Service

Poor customer service, coupled with technical issues, can negatively affect your business. So, selecting a credit card processor that provides you ample support is essential. If you have a problem submitting batch transactions, you’ll need timely customer service from the provider.

If your business has complex credit card processing needs, you’ll need priority customer service. So, consider credit card processors that provide in-house customer service. Also, confirm if the service is available 24/7.

As well, check if the credit card processor offers a comprehensive online knowledge base that can help you resolve issues on your own. A dedicated support service helps you reduce any downtime you may face in case of any issues.

3. Transparent Pricing

Partner with a credit card processor with transparent pricing. Knowing the pricing plans is just the beginning. You also need to figure out the right pricing model for your business.

Each tier in a pricing plan offers different features and performance for various processors. So, take into account product bundles.

Besides reviewing the price list, compile questions you need the credit card processor to answer. So, take the time to speak with a representative of the credit card processor. This will let you know if the credit card processor provides you honest and transparent pricing.

4. PCI Compliance

As a merchant, your business must be PCI-compliant to make sure you protect your customer’s credit card data.

For a business that accepts, transmits or stores cardholder information, it’s prudent to partner with a card processor that understands and can help you become PCI-compliant.

With rapid development in payment processing services, you need to be up-to-date with the latest PCI DSS requirements as a business owner.

Some statements from marketing or sales departments about PCI compliance may not paint the true picture. For instance, the processor could be PCI compliant, which protects the processing of payments on its channels but excludes your business channels.

So, establish how a credit card processor aims to protect your credit card payment data. If your business relies on a third-party credit card processor, you will have less burden to comply with PCI regulation. However, you still need some form of verification to remain compliant.

Inquire how the credit card processor will protect credit card payment data. Let the processor clarify if they do annual assessments.

Should you decide to sign up for a merchant account, inquire if the credit card processor helps with yearly PCI assessment for your business. In addition, establish if your preferred POS terminals and card readers support point-to-point encryption.

High-end encryption in the retail sector allows merchants to comply with most PCI requirements when they send encrypted credit card data. A quick glimpse at the website for the PCI Security Standards Council gives you free resources you can use for your business.

It allows you to verify if the credit card processor has been tested independently for the protection of credit card payment details. Also, the website can help you come up with questions you may want your preferred credit card process to answer.

5. Features and Integrations

Some credit card processors do more than just processing credit cards. They allow merchants to access details such as customer insights, manage inventory (check out the best inventory software), and send invoices.

Today, there are credit card payment processors that are more suitable for POS, e-commerce, or mobile, while providers offer omnichannel solutions. Choosing one processor with multiple integrations and features is an excellent decision for cost implications and consistency.

If you need a card processor that integrates with other platforms, you should establish if the processing system allows this for your business.

In case you rely on other vendors for the POS system, the credit card processor should integrate transaction data from your vendors. Lastly, establish the reliability of the credit card processor. Sometimes, unsophisticated gateways are slow, which can result in frustrations.

So, do an online search for reviews of the credit card processor you’re considering to establish customer feedback. Make sure the processor has a solid uptime and impeccable connectivity speed for the smooth processing of credit cards in your business.

Contractual Terms You Need to Consider

For a business owner, understanding the contractual terms and conditions in credit card processing is essential. Here are some common contractual terms.

Contract Length Clauses

As you sign up with a credit card processor, request detailed information regarding the duration of the contract. Some credit card processors conveniently “forget” to give you these details.

The normal contractual period is 3 years or 36 months that correspond to your monthly billing. However, it is not uncommon to find contracts that last at least a year and others that go up to four or five years.

If the contract has an automatic renewal clause, your credit card processor may extend the contract by 12 months. However, the renewal clauses vary from one provider to another but vary from 6 months to 2 years.

Canada is one of the countries that limit automatic contract extensions to a maximum of six months. Long-term contracts limit your chances of leaving the contract as a merchant in case you wish to change the credit card processor.

The trend today in credit card processing is subscribing to monthly, flexible billing. Businesses are committed to monthly contracts from credit card processors.

Scrutinize the contractual Terms and establish if the initial contract is 30 days with a similar renewal period.

Provided there are no early termination fees; monthly contracts provide businesses with the freedom to terminate their contracts without financial consequences. Most likely, you will only pay a recurring fee for one more billing cycle.

Early Termination Policies

Few contractual aspects in credit card processing are worse than an expensive penalty. Some credit card processors impose an early termination fee if you terminate your merchant account before the contract expires.

Usually, the fixed early termination fee varies from $295 to $495, regardless of how long you have been in the contract. Other credit card processors use proration to calculate the fee depending on the time left before the contract expires.

Proration decreases the penalty provided you have been with the credit processor for a while. In some cases, credit card processors have liquidated damages clauses instead of a fixed fee termination fee.

With liquidated damages, a processor combines the average volume of credit card processed monthly with the contract’s remaining period. These can be expensive for a business with a high monthly volume if it terminates the contract very early.

While reviewing the early termination policies in a contract, you will notice the intensely biased way the policies apply. For instance, as a merchant, the contractual obligation requires you to keep your merchant account active as you pay fees.

However, the credit card processor can terminate your merchant account for any reason. Although it is unlikely for a processor to terminate your account if you pay their fees, impromptu termination of a merchant account can halt your ability to accept credit card payments.

Account Closure Clauses

Prolonged contracts and automatic renewals are supposed to hook you indefinitely to a credit card processor. However, it is possible to terminate your card merchant account without paying fees. Most merchant contracts include clauses for closing a merchant account.

Although some credit card processors make it difficult, you can still terminate your contract when it expires without paying a termination fee. You can accomplish this by carefully adhering to the account closure instructions in the contract.

Most credit card processors require written notice within a certain period before the expiry of your current contract. Unfortunately, it can be hard to establish the exact renewal date. So, submit your notice long before the necessary minimum notice period.

Normally, credit card processors require a 30-day notice, even though this varies since some contracts have a 90-day notice period before contract termination.

Also, some credit card processors require users to submit their termination notices on special written forms that the processors only provide upon request.

Legal Dispute Clauses

It is rare to have a legal dispute between merchants and credit card processors. Usually, credit card processors will protect themselves by adding clauses in the contract that make it hard to sue them.

As you come to the end of the contract terms, you’ll find various provisions that deal with any legal action. The most familiar limitations are the mandatory arbitration clauses that are available in almost every merchant service contract.

Such clauses just require submission to mandatory arbitration instead of filing a lawsuit. Normally, courts refer you to arbitration prior to hearing a case. As such, these clauses rarely influence the ability to sue your credit card processor.

The choice of jurisdiction clause is part of almost all credit card processor contracts. Most processors limit jurisdiction to the state they have their headquarters.

Even though this doesn’t hinder you from suing a credit card processor, it can be a roadblock when you are not in its jurisdiction. So, this leaves you to cater to all the costs you incur traveling to court appearances.

However, the geographical proximity of a credit card processor should not determine your choice. It only applies to contractual limitations, should you decide to sue the merchant services provider.

Third-Party Agreements

Should your credit card provider include a third-party service or product, the provider should give you a separate third-party agreement. Most third-party agreements come from payment gateways and equipment leases.

The agreements can be part of the main contract or separate documents. For instance, for an online business, you may require a payment gateway. So, if the provider offers exclusively, then you sign an agreement with Authorize.Net.

Many credit card processors rely on different providers for equipment leases. In most cases, the credit card processors own the companies that offer equipment leases. Note that equipment leases are different from credit card processing terms.

Often, equipment leases are designed to be longer to hook you to monthly payments long after terminating your credit card processing account.

Credit Card Processing FAQ

You have different ways of saving money on credit card processing fees. Start by choosing the right fee structure by considering the bundled fees and what is ideal for your business. If you sell big-ticket items, you may find interchange-plus pricing cheaper compared to a flat fee.

You can also negotiate with your payment processor, provided you have a history with them, and your business is growing. Your processor won’t want to lose a growing business.

Besides, you can encourage customers to use debit cards since, in tiered pricing, they fall under the lower, qualified rate. So, you will save money when customers pay with debit cards.

As well, avoid using a swipe function and go for a chip reader terminal. Even though it may not save you money immediately, it will help in the future when a customer issues a payment dispute. Also, setting a minimum amount for credit card transactions saves you money.

For instance, avoid credit card transactions for $2.00 payment when the processor charges you $0.30 for each transaction. This applies when you have interchange-plus pricing or tiered pricing.

Another way you can save money on fees is by passing those fees to customers. Many states in the US permit businesses to do so. You can charge your customers a surcharge fee when checking out using a credit card.

Today, you have multiple credit card processing hardware and software. Depending on your business needs, you can choose any or a combination. A mobile card reader is a portable device that lets you accept payments via a credit card payment app on a smartphone or tablet.

Also, you can use a credit card terminal with a built-in keypad and receipt printer. You can opt for a countertop model that connects to your computer through Ethernet or wireless models that rely on Bluetooth or Wi-Fi.

As well, you can choose a Point-of-sale (POS) system, which is a complete checkout station consisting of a touchscreen, software, card reader, cash drawer, and a receipt printer. POS allows you to integrate barcode scanners, among other peripherals.

What’s more, if you run an online business, you can use a payment gateway to accept payments. Ecommerce sites developed on platforms such as Squarespace (check our Squarespace pricing review) allow you to integrate payment gateways.

Having the right credit card processing equipment is important for any business. You can decide to buy, lease, or purchase credit card processing equipment.

Even though each approach has its pros and cons, equipment leasing is among the most unfair and dishonest practices. For a while, equipment leasing was viable; however, it is no longer affordable compared to purchasing your equipment.

Last few years, competition led to a drastic decrease in hardware prices. Today, mobile payment systems allow you to receive credit card payments on your smartphone or tablet through an affordable card reader.

Technically, free credit card processing terminals are never free. In case your credit card processor gives you a ‘free’ credit card terminal, it recoups its money somehow in the contract, either through fees or surcharges.

For instance, most free terminals are proprietary, supporting only specific credit card processors. So, a “free” terminal is not free, after all.

The slow adoption of EMV by businesses in the US gave way to a high rate of credit card fraud. EMV is a global safety standard for chip-based payments that protects credit card users against fraudulent charges.

By embracing EMV chip cards, your business will join the international fight against credit card fraud. Also, you will protect your POS system from fraudulent activities like credit card skimming.

You can also opt for third-party help from businesses that specialize in detecting credit card fraud to help you establish a possible risk before making a sale. Better yet, you can integrate mobile payments to receive payments through apps such as Apple Pay.

With mobile payments, you significantly decrease credit card fraud since you no longer need a credit card to receive payment.

Thanks to technology, processing credit cards is now safer compared to the past. However, as a business owner, you must remain vigilant. Most experts agree that businesses can increase their security when processing credit cards by taking these actions.

Businesses must ensure they comply with the Payment Card Industry Data Security Standard (PCI DSS). Second, businesses should upgrade to card readers that are compatible with EMV (Europay, Mastercard, and Visa) chip cards.

Unlike magnetic stripe cards, EMV chip cards are harder to counterfeit and make transactions more secure.

Ready to Collect Money from Your Customers Using Credit Cards?

Regardless of whether you’re juggling multiple retail locations or own an eCommerce business, one of the 15 credit card processors should meet your credit card processing needs.

Although each credit card processor has its own features, they all give you competitive rates and an easy, cheap setup. While they all offer more or less the same service of connecting an acquiring bank to an issuing bank, each brings unique value to the table.

Square, PayPal, Payment Depot are excellent choices for very small, low-volume businesses, while Fattmerchant, Helcim, PaymentCloud, Merchant One, FIS, TSYS, Fiserv, and Flagship Merchant Services are better for larger retail businesses.

National Processing is ideal for startups and cost-conscious businesses. For eCommerce businesses, Stripe is a remarkable option. If you run a nonprofit, Dharma Merchant Services could be your best option.

If you already use QuickBooks, then consider QuickBooks Payments. These credit card processing services will give you a better, more affordable service compared to what you would get from any of the traditional, bank-owned credit card processors.

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.