Bank Guarantee – Overview, Types, and Examples (Easy Guide)

Contracts are successful not because both parties act on the agreement but because there is a guarantee available to protect both parties from major losses.

This article discusses how bank guarantees work and how you can take advantage of their benefits.

Let's get started.

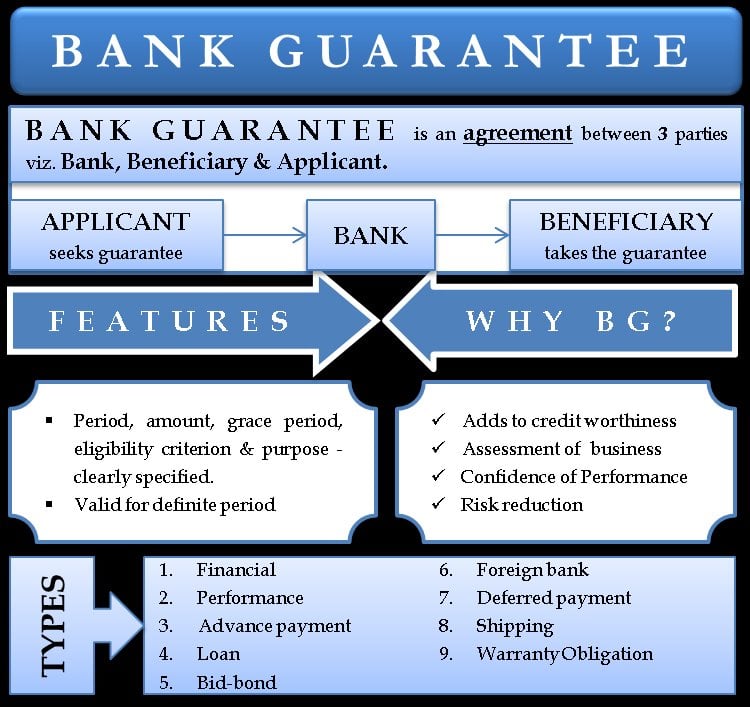

What is a Bank Guarantee?

A bank guarantee is a reliable assurance a financial institution offers to an external party if the borrower defaults in paying back the money owed. This risk management tool is a guarantee that the financial institution will refund the debt if the borrower fails to satisfy its financial liability.

Most businesses use bank guarantees to make major business decisions such as acquiring goods, buying equipment, or performing international trade.

The parties involved in the contract.

- The Applicant is an individual or a corporate body interested in requesting a bank guarantee and borrowing on credit.

- The Bank or Financial Institution is responsible for the payment obligations if the applicant fails to fulfill the bargain.

- The Beneficiary is the lender that offers financial assistance to the borrower and is liable to receive a partial guarantee if the debtor defaults.

A simple example will involve the CEO of Joy’s Bakery. The CEO took a loan from an investor willing to offer loans to start-ups.

Both parties agreed to set the repayment time to two years, but the CEO of Joy’s Bakery failed to make enough profit because of poor sales to repay the loan. The investment company will receive the payment from the bank with an already signed bank guarantee contract.

Types of Bank Guarantees

There are a variety of bank guarantees within the banking system. These bank guarantees are relevant in different situations for different transactions.

Let’s check out some of the popular bank guarantee types.

1. Direct Guarantee

A direct bank guarantee is popular among merchants and business owners. They only involve three parties: the financial institution or bank, the borrower who needs funds or goods, and the beneficiary who receives the funds.

The bank is liable to refund a certain amount to the beneficiary if the corporate customer defaults on payment.

2. Indirect Guarantee

An indirect guarantee applies to international trade rather than local trade. What separates this bank guarantee from others is it requires four parties to guarantee financial credibility and finalize the process.

International suppliers may not be confident in the ability of a local bank or financial institution to deliver on the bank guarantee promise. There is a need for a fourth party for an extra guarantee.

An indirect guarantee involves four parties: a local buyer, a local bank, a foreign supplier, and a foreign bank.

The payment process is the same as a direct guarantee with a slight difference. A local bank issues a bank guarantee to the foreign bank, which will offer a guarantee to the exporter.

3. Financial Guarantee

A financial guarantee is a common offer with most banks. You can call it a financial bank guarantee. It involves the prompt payment of funds the corporate customer used to purchase goods and services once the supplier fulfills the bargain.

The bank‘s only concern involves ensuring the beneficiary gets the designated funds once the due dates for the payment arrive.

4. Performance Guarantee

Performance guarantees are different from payment guarantees. They focus on other contract aspects rather than funds.

The guarantor (bank) responds if the seller fails to deliver on the deal or defaults in delivering the products or services as promised in the contract.

A vital part of the bank's job is to guarantee that the seller delivers the required goods or services on time. They return the advance along with any fines and penalties decided in the contract.

5. Secured Guarantee

A secured bank guarantee works when the bank receives a payment or collateral before signing the bank guarantee.

Corporate customers may offer assets in the form of properties or several funds. Such deals protect the bank from high risks regarding the contract because they have something to hold till the customer pays the debt.

6. Unsecured Guarantee

An unsecured guarantee does not require collateral to sign the contract. This bank guarantee type is similar to a business loan the bank approves because of the security based on the buyer's credit.

The issuing bank charges a huge payback fee since there is no collateral to back up the customer's claim to pay back.

Unsecured back guarantees are risky. Without proper management, they can destabilize a banking system.

7. Advance Payment Guarantee

An advance payment guarantee helps in protecting the buyer after making payment to the seller before acquiring the desired goods and service.

In protecting the interests of the corporate customer, an advance payment guarantee will ensure that the buyers recover either partial or all of the amount paid.

8. Deferred Payment Guarantee

A deferred payment guarantee is usually associated with the purchase of capital goods or machinery. The seller of these goods or machinery offers credit to the buyer, and the buyer's bank guarantees the due payments to the seller.

This form of bank guarantee is relevant when the agreed installment payment is deferred or postponed.

The seller creates a convenient payment plan for the purchase of goods and machinery. For the contract to stand, the bank and the buyer must accept the payment plan.

The bank pays the seller on the agreed due date, and the borrower will return the funds in installments.

Other Types of Guarantees

- Demand Guarantee serves as a protective means for a contract that ensures the beneficiary gets funding if one of the parties does not meet its obligation.

- Customs Guarantee serves to cover debts that arise from customs and excise duties and import VATs. With this guarantee, you will always get your goods back without loss on your part.

- Rental Guarantee serves as collateral for rental agreement payments.

- Warranty Bond Guarantee performs the role of collateral that ensures a buyer gets the goods ordered based on the original agreement.

Examples of Bank Guarantees

A real-world example will give you more insight into how bank guarantees work and how to take advantage of them. Here is a perfect example that applies to both financial and performance guarantees.

Carbon Flower Mill is a major supplier of baking flowers. Most successful bakeries and restaurants patronize them because of the quality of their products.

Junes Bakery is a start-up company that produces pastries in small quantities but hopes to expand with the right supply of raw materials and funds.

June's Bakery wants to go into a legal contract with Carbon Flower Mill for a contract supply of rum materials for a year. Carbon Flower Mill requires a legit bank guarantee before agreeing to the details of the contract.

This bank guarantee will protect both parties if one defaults. If there is any deficiency in the supply of raw materials or Junes Bakery refuses to pay on the due date, the bank will swing into action by compensating the aggrieved party.

Advantages of Bank Guarantees

Bank guarantees offer benefits to every party involved in the contract. Here are some advantages of a viable bank guarantee.

1. Lower Costs

Bank guarantees are an effective way to boost the creditworthiness of a company or an individual involved in the contract.

Paying a supplier will naturally cut down the borrower's savings. A bank guarantee offers a cost-effective solution because the bank fees are generally low. Most banks charge between 0.5% to 1% of the actual amount they guarantee.

Repaying the bank is a more convenient option for the corporate customer base. Business activities can continue without financial issues.

You can produce goods and services at a reasonable price without increasing the prices due to the pressure to pay back the loan.

2. Better Cash Flow Management

A purchaser has no obligation to make advanced payments because the bank guarantee promises print payment to the seller.

The seller is encouraged to fulfill his part of the bargain by delivering goods or services without asking for advance payments. This arrangement helps the buying company manage its cash flow better.

In addition, no advance payment equals less working capital, which positively influences the overall business cost.

3. Increased Opportunities

Small and medium enterprises face issues when applying for loans to improve their business operations because of the lack of creditworthiness.

This problem does not apply to large corporations. Large corporations can easily acquire loans for various financial needs without much scrutiny.

Bank guarantee gives all types of companies a level playing group to execute their operation and receive loans and credit guarantee.

Because banks are a valid substitute for creditworthiness, small and medium organizations are more open to opportunities to expand their business and increase sales.

4. Streamlined Process

Acquiring a bank guarantee is not as difficult as it seems. Organizations that have taken advantage of this opportunity regularly are aware of the seamless and streamlined process.

The bank conducts extensive research and checks to ensure the business is legit and will not default on payment. Once the bank confirms the organization's reliability, it issues a bank guarantee within a couple of days.

Acquiring bank guarantees is not as complicated as obtaining bank loans and overdrafts.

Disadvantages of Bank Guarantees

Bank guarantees have certain drawbacks that make the process difficult for all the parties involved. Here are some disadvantages of bank guarantees.

1. Difficult to Obtain

Acquiring a bank guarantee is not easy when the requesting corporation does not have a stable cash flow. Companies in this position may encounter difficulties acquiring bank guarantees, but it is not impossible.

Businesses may receive unsecured bank guarantees, similar to bank loans. Most banks carry out due diligence regarding the credibility of the company in question. This process may take a long time before they offer them the guarantee.

2. Collateral Required

Most banks ask for collateral from corporate customers before issuing a bank guarantee. The purpose of this collateral is to safeguard their investment if the transaction does not go according to plan.

For businesses that don't have collateral to offer to secure a bank guarantee, the process is usually difficult.

3. Regulatory Hassles

Bank guarantees are an effective way for businesses and corporate organizations to take vital steps regarding their growth and development without much financial stress.

Not every party fulfills their end of the bargain, and it may cause a backlash on the issuing bank.

The banking system regulatory body has a strict set of rules which all the involved parties must follow. These strict rules make the process difficult and stressful, thus discouraging most organizations.

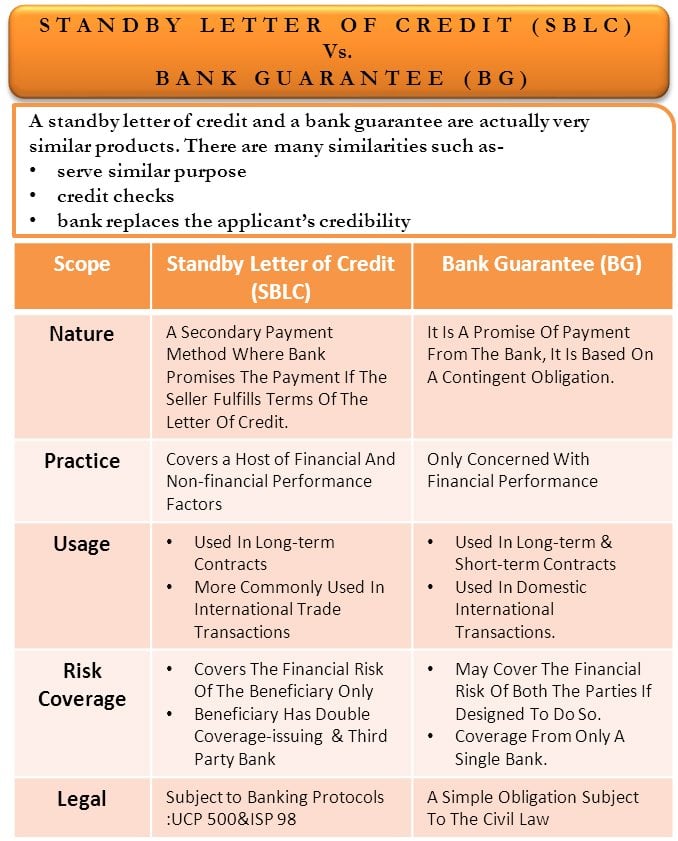

Bank Guarantees vs. Letters of Credit

Standby letters of credit are similar to traditional bank guarantees but with some unique differences, and they serve the same purpose.

A letter of credit is a financial instrument that guarantees that the beneficiary will receive funding once the buyer collects the designed goods and services.

With a standby letter of credit, the seller is the bank's priority. This financial instrument offers more confidence that the seller will receive prompt repayment because the bank is involved in the transaction.

A letter of credit is a great option for a buyer when there is a temporary financial shortage. The bank will later recover the amount paid by the seller with any associated or applicable bank guarantee fee.

A bank guarantee promises the bank will take action when one party fails to fulfill their contractual obligations. In most cases, the bank steps in when the defaulter fails to pay the supplier or fulfill the performance criteria.

The bank's role is to settle the beneficiary by paying a compensatory amount when there is non-performance of the signed contract. In reality, the bank's liability only applies if one party fails to uphold their end of the contract.

FAQ

Do Banks in the U.S. Issue Bank Guarantees?

Banks in the United States do not often issue legitimate bank guarantees mainly because of the high risk of default. Their alternative means is to issue standby letters of credit that can serve the same purpose.

Explore Further

- How to Build Business Credit Fast

- Financial Leverage: How Does It Work

- How to Open a Business Bank Account

- Business Loan Eligibility Criteria and Documents Required

- Small Business Lending Statistics and Trends

- How to Calculate Working Capital

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.