Small Business Lending Statistics and Trends (2025)

82% of small businesses fail because of poor cash flow management. 29% run out of money. Fortunately, you have a variety of lending options. Traditional banks, online lenders, friends, and family can all help meet your cash flow constraints. You can also get funding to help your business gain the necessary momentum to expand your operations and reach your financial goals.

Whatever situation you’re in, this article covers the latest small business lending statistics for 2022 that you should be aware of. We cover the hidden lending opportunities for women and minorities, how to get a business loan, the best business credit cards, and lucrative trends reshaping the loan industry.

Key Small Business Loan Statistics

- A small business loan typically has an interest rate of 2.54% to 7.01%.

- A third of small businesses are founded with less than $5,000.

- Of all small business financing options, merchant cash advances have the highest approval rate (85%).

- Poor credit resulted in 36% of small firms being denied the requested funding.

- Businesses with two founders raise 30% more capital than those with one.

General Small Business Lending Statistics

1. 48% of small businesses have their financial requirements satisfied.

(ValuePenguin)

This 48% comprises the 28% of small businesses that didn't apply for financing because they had sufficient capital, as well as the 20% who were approved for all the financing they required after the small businesses applied for funding. The remaining 52% of small businesses with unmet financing needs consist of:

- Those who apply but only obtain a percentage of the financing they want.

- Those who apply for funding but are not approved.

- Those who refrain from applying because they are discouraged.

- Those who choose not to apply due to a fear of debt.

2. The median small business loan across all banks in America is $633,000.

(Federal Reserve)

Since a small business in the United States and Canada has less than 100 employees, loan amounts can range widely depending on the organization's size, from a few thousand dollars to more than $5 million.

This figure can help you estimate the amount of financing you can obtain, but it also leaves out a lot of information. It’s challenging to determine the average small business loan amount because there are so many lending institutions and funding options available that an overall average amount isn't always useful.

However, you'll start to have a clearer picture when you compare the average small business loan amount across lending organizations, loan categories, and lenders.

3. 70% of small businesses have some sort of outstanding debt.

(Federal Reserve)

Additionally, according to small business lending statistics, most businesses with outstanding debt have balances under $100,000. 17% of small firms have debts of up to $25,000, while 21% have debts of between $25,000 and $100,000.

4. The interest rates on 95% of business term loans are fixed.

(Fundera)

A lump sum of money known as a business term loan is available to business owners through online lenders, institutional lenders like Pension Funds, or other financial organizations. Companies have a set period to pay back the lender.

These small business loans may be for short, medium, or long term, and the approval rate varies significantly depending on the lender. For instance, the approval rate for medium-term small business loans through a bank takes longer than approving them through an online lender.

- Long-Term Loans: These have at least a six-year term. Small businesses often employ them for large purchases, like a business vehicles or real estate.

- Medium-Term Loans: These loans typically have two to five years and are used to finance business expansion or purchase equipment.

- Short-Term Loans: These have periods of less than two years. Small businesses frequently use them to finance inventory purchases, bridge shortfalls in working capital, or take care of other urgent cash requirements.

A small business loan typically has an interest rate of 2.54% to 7.01%. The loan source, whether a bank, program, or administration, accounts for most of this discrepancy.

5. Traditional banks are being superseded by fintech lenders.

(Westtown Bank Trust)

The fintech lending market has developed over the past few years, and these new school lenders are getting closer to displacing traditional banks. That has corresponded with a change in public perceptions about fintech, with a recent survey showing that 88% of American consumers now use it to some extent.

By obtaining a bank charter, fintech businesses can provide financial services comparable to conventional banks while utilizing cutting-edge technology to enhance the borrowing experience. Additionally, it implies fewer regulatory obstacles must be overcome, which may result in cheaper overall expenses.

The fintech sector is continuously developing in new directions, and lending is just one trend that companies should keep an eye on to determine how they might use the services provided by the fintech sector.

Fintech is experiencing a very exciting time right now. By upending the closed club of established financial institutions and introducing alternative, tech-focused solutions into the mainstream, more entrepreneurs are now able to launch and grow their firms.

6. A quarter of small businesses launch without any sort of funding.

(Gallup)

Many small businesses prosper without financial backing when they first begin. 77% of them, according to a Gallup survey, rely on the founders' personal savings to cover their startup costs.

That indicates that more than three-quarters of new enterprises require capital from founders—regardless of how much capital they can raise externally—despite the constant chatter and news of startups raising capital from external sources.

7. A third of small firms are founded with less than $5,000.

(Kabbage, Wells Fargo)

The founders' financial commitment to financing a startup may not be as substantial as you might believe, according to the small business loan statistics from Kabbage.

The financial repercussions of starting a business can be overwhelming, regardless of whether you plan to fund it with personal savings, stock, loans, or all of the above. But those effects might not be as severe if a third of small businesses can survive on less than $5,000 in startup capital.

The Wells Fargo Small Business Index conducted another survey similar to the one above, which revealed that the typical small business needs roughly $10,000 in launch financing.

This data demonstrates how drastically startup capital requirements—and accessibility—can vary, especially when compared to the fact that a third of small enterprises launch with less than $5,000.

While some small firms can launch with less than $5,000 in funding, other small businesses need and can get far more funding, which increases the average.

8. The most frequent reason for loan requests from business owners in 2021 was to pay operating costs.

(LendEDU)

That is expected in an environment where pandemic-related shutdowns have hurt the economy. According to small business loan statistics from LendEDU, more than half of enterprises that sought financing did so to pay for operating costs like rent or mortgage payments and salaries.

Fewer small business owners now borrow money to grow their companies than in years past. Compared to 56% in 2020, just 38% of business owners got a loan to grow their company in 2021. Government initiatives and low-interest rates might have inspired business owners to refinance for a bargain.

9. In 2021, 32% of business owners asked for a loan to refinance or pay off debt.

(LendEDU)

Small business owners continue to turn to banks as their initial source of finance. Forget what you've heard about how banks will soon be a thing of the past, thanks to fintech startups. Banks of all sizes dominate the market for business loans, and this trend doesn't seem to be changing anytime soon.

Statistics on Small Business Loan Type

10. In 2021, 65% of SBA loan applications backed by the government and collateral were approved by many lenders.

(NerdWallet)

While SBA small business loans are intended for companies with difficulty obtaining financing elsewhere, they come with their own complex set of qualifying standards that consider anything from a business owner's personal assets to prior legal troubles. If you have any legal issues, read this article on the best online legal services.

11. The average sum for short-term business funding is about $20,000.

(Fundera)

The average amount for a medium-term small business loan is $110,000. While $107,000 is the average SBA loan amount. And $22,000 is the average SBA loan amount for a business line of credit.

The lender also affects loan sizes. Here’s a breakdown of average loan sizes by type of lender. The typical sum of a large bank loan is $564,000. While for a small bank loan is $185,000, while an alternative loan is $80,000.

12. $5 million is the highest amount you can get for an SBA loan.

(SBA)

Lenders and banks process loans provided by the U.S. Small Business Administration SBA. You can use these low-interest loans to purchase property or equipment, expand your business, or get back on your feet. There are four distinct types of SBA loans:

- SBA 7(a) Loans: These SBA loans are mostly used by full-service restaurants because they can help with working capital and purchasing a company or business equipment. The maximum loan amount is $5 million, and the interest rate varies based on the prime rate. There must be collateral.

- SBA 504 Loan: Business owners can use this option to buy real estate and equipment but cannot use it for working capital or purchasing inventory. The SBA 500 loan has a $5 million cap. Normally, interest rates are fixed and based on the yields on five- and ten-year US Treasury bonds. No security is needed.

- SBA Disaster Loan: This option offers business owners up to $2 million. They are created especially for small businesses impacted by natural disasters or major world crises. The SBA claims interest rates are set and decided by legally prescribed formulas. (Normal rates range from 3% to 7%.)

- SBA microloans: This option can be used for operating capital, as well as to buy supplies, furniture, or equipment. Interest rates range between 8% and 13%. You can borrow a maximum of $50,000 from community-based groups that offer loans.

13. In the US, 77% of small firms rely primarily on business earnings for finance.

(SBA, US Census Bureau)

According to the US Census Bureau, the average annual revenue of a small business with no workers is $46,978. Many small businesses used the tools offered by the SBA Office of Capital Access throughout the pandemic to sustain their financial flows.

The Paycheck Protection Program provided financial help to 73% of small employer businesses in 2020. It gave small businesses loans to cover the interest on their mortgages, rent, and utility bills.

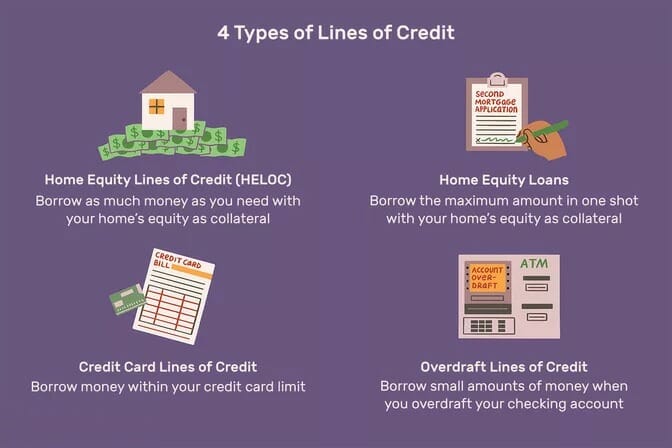

14. Lines of Credit loans’ main eligibility condition include having a minimum personal credit score of 500 or higher.

(FORA Financial)

LOCs, often known as lines of credit, give business owners instant access to funds ranging from $1,000 to $250,000. They can use a line of credit, a one-time payment, for expenses like inventory, rent, or new equipment.

Large banks provide businesses with lines of credit without set repayment conditions, in contrast to business term loans. In 2021, 54% of US small firms asked for a line of credit, according to small business financing statistics from FORA Financial.

15. Banks served as the primary lender for 43% of equipment financing transactions.

(Business News Daily)

Equipment financing is a business loan made to finance equipment, like tractors, computers, or industrial fridges you require. Your equipment will be rented from lenders while you make monthly installment payments for it.

The equipment will belong to your company after the sum has been paid. Nearly 8 in 10 US businesses, according to small business funding statistics, finance the purchase of new equipment in this way.

16. Most Accounts Receivable Finance lenders only provide a portion (about 75–80%) of the whole amount of your outstanding invoices.

(FORA Financial)

Small firms can borrow money for working capital by using their unpaid invoices as collateral through accounts receivable financing. When the invoices are paid, you pay the initial sum back to the lender and weekly fees that serve as interest.

Only 3% of small business owners said they used a home equity line of credit (HELOC) to launch their business. Small businesses with low credit scores turned to non-bank finance companies for loans 23% of the time, and 35% of them turned to online lenders. The latter group consists of mortgage lenders, suppliers of equipment, and insurers.

17. Shopify Capital loan amounts for small businesses range from $200 to $2 million.

(Shopify)

This is a finance choice for Shopify store owners without an application process. It has an established 12-month duration and is generally utilized for growth financing. Automatic repayment of the loan is made as a proportion of your sales.

Statistics on Small Business Lender Type

18. Alternative lenders loan small businesses $50,000 to $80,000.

(Biz2Credit)

These lenders are primarily online-only private businesses. Some well-known alternative lenders include Balboa Capital BlueVine, Fundbox, OnDeck, Credibly, Funding Circle, and QuarterSpot.

19. 32% of small businesses apply for loans at non-bank lenders.

(Finder)

Small businesses are increasingly turning to non-bank lenders for loans, as evidenced by the rise in this percentage from 19% in 2019 to 24% in 2020.

That is because 77% of small firms that ask for loans from major banks are turned down. In the past, banks were the primary source of finance for business owners. But because there is a small chance of not receiving their money back, big banks aren't usually eager to lend.

Thankfully, many other lenders provide small company loans. The application process for these online, non-bank lenders is simpler and quicker than going to a bank. You can start receiving the money the following business day after being approved.

20. There are numerous scams to be on the lookout for in the online lending space.

(BBB)

Receiving the necessary funding has become simpler for small business owners thanks to the enormous rise of online lending. Sadly, this has also increased the number of scammers.

According to a BBB and Fair Trade Commission poll, 67% of small businesses indicated lending scams have gotten worse since three years ago. By assuming the identity of a legitimate lender, scammers will attempt to steal your money, personal information, and company data.

Make sure you first conduct your due diligence to prevent lending scams. Ensure the lender has reliable contact information, such as a real address and an operational phone number.

21. 0.05% of new businesses secure venture capital.

(Entrepreneur)

Only a handful of small businesses raise initial venture financing, even though venture capital is mentioned in about 100% of news on startup funding. This statistic, taken from an article in Entrepreneur, contributes to creating a more accurate image of what startup funding looks like for a typical new business.

Because “seed funding,” “unicorns,” and “supergiants” receive so much media attention, the public's image of startup funding is understandably distorted. And it's exciting and worthwhile to write about that stuff. However, it only accounts for a fraction of the total startup investment.

22. The typical seed round is around $2.2 million.

(Susa Ventures)

The typical small business needs $10,000 in initial capital, which is 200 times more than that amount.

Naturally, many businesses go through the seed round in the hopes of becoming much larger than the average small business and attracting considerably larger amounts of investment.

Nevertheless, comparing these figures shows how venture capital is an outlier compared to startup funding.

23. The average business running a seed financing round was three years old.

(Susa Ventures)

But these days, seed investment and startup capital aren't always the same.

The typical company raising a seed round of venture capital funding had been in operation for 3.03 years.

As a result, companies that successfully close their seed round of financing are already very well-established and can leverage their track record to get venture capital.

24. Only 1% of firms that raised seed capital were valued at $1 billion or more, or unicorns.

(CB Insights)

CB Insights examined 1,119 firms that raised seed rounds over ten years to understand the venture capital funnel better and discovered that just 12 were acquired for a price of $1 billion or more.

Many came out of the funnel through self-sufficiency, IPO, or an M&A, which are excellent for some firms. However, many point to this “unicorn status” of an exit valuation of $1 billion or more as a target for entrepreneurs.

25. Businesses with two co-founders raise 30% more capital than ones with one.

(Inc.)

According to Inc, businesses that have two co-founders are more likely to succeed, and this success might take many different forms. This increased success translates to more funds when soliciting capital for businesses.

Two business founders working together, contrary to what some may believe, is a sign of balance and well-roundedness. Instead of a lone wolf entrepreneur, investors like to see co-founders, and their fundraising strategies reflect that.

26. Over $169 billion in community development loans were made by all lenders in 2021, up 52% from the amount reported in 2020.

(The Guardian)

This significant growth can be attributed to PPP financing, as many PPP loans that did not reach the size standards for reportable small company loans nevertheless satisfied the criteria for reporting as community development credit.

Statistics on Small Business Loan Demographics

27. Small firms in rural areas are 51% more likely to be approved for all the funding they ask for.

(Ondeck)

Conversely, only 38% of urban small businesses receive the entire amount of capital that meets financing needs. That is particularly intriguing given that just 17% of small enterprises are located in rural areas. With 62% of loan applications going to small banks, small rural companies rely on them more.

In contrast, 43% of urban small businesses approach smaller banks for loans; 53% ask for loans from larger banks. Of course, this is understandable given that just 25% of banks in cities are small banks, compared to 55% in rural areas.

Given the stark differences between urban and rural locations in the United States, it’s not surprising that small firms can perform differently depending on where they are located. Inequalities in racial, gender and social class might also be factors.

28. Less than 2% of small business loans go to black-owned firms.

(Statista)

That is the case even though Black Americans make up 13% of the population. According to studies, fewer than 47% of financing requests submitted by Black-owned businesses are granted, which indicates that they are twice as likely to experience loan rejections.

Only 16% of small business financing goes to women-owned small businesses. And this is despite the fact that women own about 30% of small businesses. Overall, studies have indicated that women are more likely than men to be rejected or subject to stricter conditions.

29. April 2020 had the highest percentage of small business closures, with Black-owned enterprises suffering the greatest loss (41%).

(Statista)

However, the number of Black, Latino, and AAPI small companies functioning increased as the immediate effects of pandemic shutdowns subsided.

Small businesses shifted their operations, returning to pre-pandemic levels by April 2021. Most notably, compared to pre-pandemic levels in February 2020, the number of Black and Latino-owned businesses was much higher in September 2021.

Statistics on Small Business Loan Applications and Approvals

30. In 2021, 43% of small business owners applied for a loan at a small bank, compared to 42% at a major one.

(Bank of America)

Only 20% of applications for business loans were submitted online, down from 33% in 2019. Only a small portion of business loans came from other kinds of lenders.

A credit union received about 9% of loan requests from business owners, while a community development financial institution (CDFI) received 3% of those requests.

31. Last year, 43% of small firms submitted a loan application.

(Federal Reserve's Small Business Credit Survey)

Therefore, it's no surprise that almost half of the small businesses applied for loans in the previous year. 57% of small business applicants requested loans for up to $100,000, and only 8% requested more than $1 million, while 20% wanted less than $25,000.

32. Poor credit resulted in 36% of small firms being denied the requested funding.

(NerdWallet)

However, why a small business lender rejects an applicant's request might vary widely. For instance, 35% of rejected applicants already had too much debt, and 33% had inadequate credit history, affecting a person's overall credit score. Here’s an article on how to build business credit fast if you’re part of this statistic.

The likelihood of approval can also be influenced by the funding a company requests and if it is secured by collateral. Additionally, just because a loan application was approved doesn't mean the business received the whole amount requested; in fact, the amount is mostly lower.

33. Merchant cash advances have the highest approval rate (85%) of all small business lending options.

(NerdWallet)

Most small firms that apply for a merchant cash advance get approved. Nevertheless, you might be shocked by how the following other loan types for small businesses compare, though:

- 80% of auto and equipment loans are approved.

- 73% of applications for business lines of credit are approved.

- The approval rate for home equity lines of credit is 70%.

- Mortgage applications have 69% approval rates.

- 67% of traditional business loans are approved.

- Personal loans have 55% approval rates.

- The approval rate for SBA loans or lines of credit is 52%.

34. The approval rates can also change based on the lender.

(Biz2Credit)

As of May 2021, the Small Business Lending Index from Biz2Credit provides the following breakdown of loan approval rates by lender type:

- The approval rate for alternative lenders is 24.3% (increasing from 20.5% in 2020).

- The approval rate for institutional lenders is 23.6% (rising from 21.4% in 2020)

- The approval rate for credit unions is 20.4% (up from 20.3% in 2020).

- The approval rate for small banks is 18.7% (up from 16.9% in 2020).

- The approval rate for large banks is 13.5% (rising from 11.5% in 2020)

- The approval rate for business credit cards is 98%.

Small Business Lending Statistics by Industry

35. Most small business loans—nearly 15%—go to the building and remodeling sector.

(SBA)

Similarly, transportation and trucking small firms rank second most, obtaining about 14% of business loans. Loans are frequently required in these sectors to pay for machinery, repairs, upkeep, and even to earn a profit.

SBA loans are not available to at least 11 legal industries. These include lending loan packaging firms, speculation-based industries, gambling, multi-sales distribution, government-owned, multi-level marketing, nonprofit, and real estate investment firms.

36. Most SBA small business loans go to full-service restaurants, with 28,680 being given out in just 2021 alone.

(SBA)

With 19,141 loans distributed, limited-service restaurant enterprises are in second place. The aggregate amount of these enormous loans was $17.1 billion. For comparison, the dental industry came in second place behind the restaurant sector with only 10,699 loans worth $6 billion.

Growing Your Business with Small Business Loans

We hope these small business lending statistics have opened your eyes to the thousands of opportunities you can use to get funding. Once you've evaluated each financing option and decided which one is best for you, get your bookkeeping in line and submit your application as soon as possible.

Finally, getting a loan is just one piece of the puzzle – you'll have to know if you'll manage to pay the monthly installments without hurting your business. And to do that, you'll need a business loan calculator:

- Bankrate has a simplistic calculator that can help you map out various financial risk strategies for loans, mortgages, credit cards, investments, insurance, and home equity.

- Nerdwallet offers a business loan calculator geared towards US-based businesses. The easy-to-use calculator estimates your monthly/yearly payments based n the APR you provide.

- Shopify is not only one of the best eCommerce platforms but also provides business loan calculations. The tool is free, so you have nothing to lose using it.

Sources

Explore More Statistics Articles

- 29 Eye-Opening SBA Lending Statistics (2023 Report)

- Credit Card Statistics for 2023

- The Ultimate List of Small Business Statistics for 2023

- 26 Business Automation Statistics for 2023

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.