What is Working Capital? Definition, Formula, Examples

If you own a business or work for one, chances are that you have heard the word ‘working capital.’ You may not talk about it in the same frequency as you talk about cash, but this accounting term plays a key role in a company’s success.

Working capital affects multiple areas of your business. They include payroll, paying vendors and suppliers, maintenance of business equipment, and planning for sustainable long-term growth. The lack of sufficient working capital affects your company’s ability to fulfill its current and short-term obligations.

In this article, you will learn the meaning of working capital, the elements of working capital, and how to calculate net working capital and the working capital ratio. You will also get tips on how to lower your working capital needs, the best ways to finance working capital, and what you need to know about negative working capital.

Let’s get started.

What is Working Capital?

Working capital refers to the money that is available to a business to run its regular operations. Another name for working capital is the Net Working Capital (NWC). It is the figure that remains when you subtract the current liabilities from the current liabilities. Mathematically, working capital can be written as:

Working Capital = Current Assets – Current Liabilities

According to Investopedia, working capital “is the difference between a company’s current assets, such as cash, accounts receivable (customers’ unpaid bills), and inventories of raw materials and finished goods, and its current liabilities, such as accounts payable.”

The accounting term determines how much short-term liquidity a business needs to cover its forthcoming liabilities. It focuses on current items that are pressing needs for the business and does not concern itself with long-term assets, liabilities, or equity.

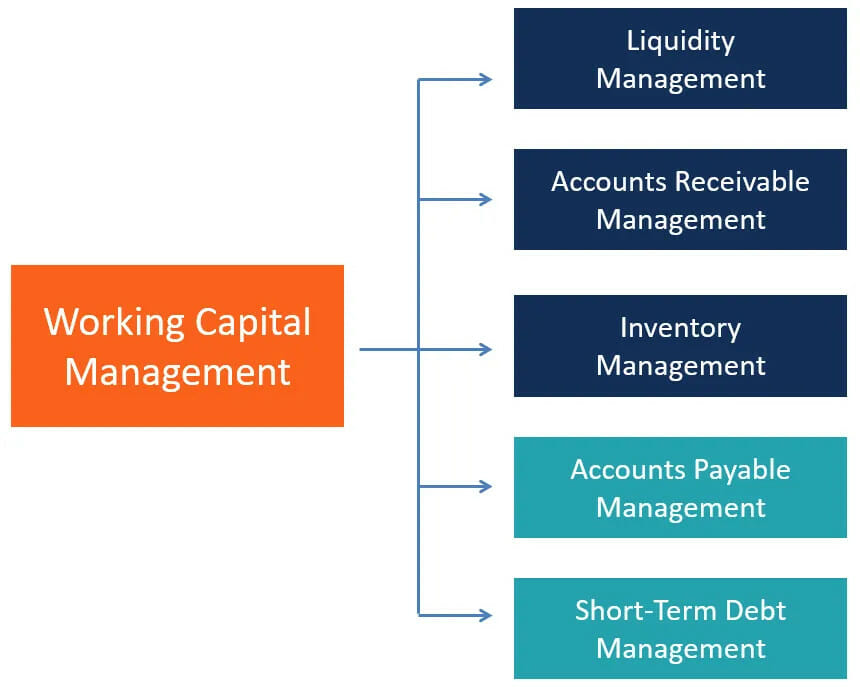

Working capital is a key metric that indicates whether a company’s operating liquidity is healthy enough for efficient performance in the short term. A company’s working capital covers different aspects of its activities such as cash, accounts payable, accounts receivable, inventory, and short-term debts and accounts.

In some cases, the working capital can also include debt management, inventory management, paying suppliers, and revenue collection. It is the total money that a business can freely spend on its operation.

Working capital is a reflection of a company’s short-term financial health and operational efficiency. A positive working capital opens room for potential investments and growth.

Companies with positive working capital usually outperform those with negative working capital. However, having too much working capital at hand is a sign that you are not maximizing your working capital efficiently.

Investors and stakeholders check a company’s working capital to determine if it can pay its debts within a year. Once a company’s current liabilities far exceed its current assets, it is an indication that the company will struggle to pay its debts and could go bankrupt.

Businesses can use their corporate balance sheet to decipher the working capital available to them. Determining your working capital from your corporate balance sheet and income statement requires all the assets and liabilities section to be accurate.

There are accounting software providers that help companies automatically reveal their available working capital from their current assets and liabilities. They include QuickBooks, FreshBooks, Xero, and QuickBooks alternatives.

Elements of Working Capital

There are two elements of working capital: current assets and current liabilities. You can find both elements in your balance sheet. These two elements are the integral components used for calculating the working capital or net working capital.

1. Current Assets

Current assets refer to assets that a business owns that can easily convert into cash in less than a year. It is on one side of the working capital formula. Businesses use current assets to handle their daily operations and operate efficiently.

Working capital is all about managing the current assets of the business so that the business has enough cash flow to cater to its current liabilities. Managing your current assets is crucial for effective working capital management.

Current assets are the cash and resources that a company has available and can be converted to cash within a year. Cash or assets that are tied to a long-term purpose do not count as current assets.

The date displayed on the company’s balance sheet is commonly used to determine the one-year duration for a company’s current asset. There are exceptions in which companies may use the duration of the operating cycle (longer than a year) to determine their current assets.

Examples of Current Assets

- Account Receivables

- Bank Balances

- Cash

- Inventory of Finished Goods

- Inventory of Raw Materials

- Inventory of Work-in-progress

- Prepaid Expenses

- Short-term Advances

- Short-term Investments

- Supplies

2. Current Liabilities

Current liabilities, also known as short-term liabilities are another significant element of a company’s working capital. It refers to the financial obligations of a company that is due for fulfillment within a year.

A company’s current liability is what you get when you add up its debts, expenses, and other financial obligations it is expected to pay within a year window.

Current liabilities refer to claims from external parties which are due in a year from the date set on a company’s balance sheet. However, there are uncommon circumstances where instead of a year duration, the company uses its operating cycle to calculate its current liabilities. In this case, the operating cycle is longer than a year.

Report your current liability as a long-term liability in your balance sheet if the long-term liability is eventually going to replace the current liability.

Examples of Current Liabilities

- Account Payable

- Accrued Expenditure

- Advances Received Against Sales

- Annual Licensing (If it is a requirement in your occupation, industry, or working area)

- Client Deposits and Deferred Incomes

- Company Tax

- Credits for Goods Purchased

- Dividends Payable to Investors

- Interest and Fees on Loans

- Outstanding Bills and Expenses

- Payroll Taxes Kept from Employees

- Rent Payments

- Short-term Borrowings or Loans

- Wages Payable

How to Calculate Net Working Capital (+ Formula and Example)

There are several methods that you can use to calculate the net working capital. You can choose to exclude some values such as cash and debt while calculating the net working capital for your business.

The most popular and basic net working capital formula used by businesses is the subtraction of current liabilities from current assets. This formula is broad and factors in all the company’s current assets and liabilities that are available or due within a year.

Mathematically, the formula read as:

Net Working Capital = Current Assets – Current Liabilities

If you want to narrow the focus on your net working capital, you can choose to remove cash and debt from the equation. The new equation will read like this:

Net Working Capital = Current Assets (less cash) – Current Liabilities (less debt)

You can further narrow the focus of your net working capital by only using three accounts (accounts receivable, inventory, and accounts payable) for your calculation. This formula is the narrowest of the three working capital formulas.

Mathematically, the third formula reads as:

Net Working Capital = Accounts Receivable + Inventory – Accounts Payable

You can also calculate changes in your net working capital by comparing the previous net working capital with the current net working capital. It is important that you do this to track how much progress you are making with your working capital management.

The formula for calculating changes in your net working capital is:

Current Net Working Capital – Previous Net Working Capital = Change in Net Working Capital

Net Working Capital Formula Examples

Here are some examples that show how to use the net working capital formula to calculate the net working capital for any business.

Example 1

An online store that sells men wears has $50,000 in cash, accounts receivable balance of $5,000, and inventory of $20,000 on the current assets side of the balance sheet.

On the other side of the balance sheet (current liabilities), it has a short-term loan of $40,000, accounts payable balance of $10,000, and accrued liabilities of $4,000. What will its net working capital be?

The first step is to identify the formula that best fits this scenario (the first formula).

Net Working Capital = Current Assets – Current Liabilities

Then we group and sum its current assets, and repeat the same process for its current liabilities.

Current Assets = Cash + Accounts Receivable + Inventory

Current Assets = $50,000 + $5,000 + $20,000

Current Assets = $75,000

Current Liabilities = Short-term Loans + Accounts Payable + Accrued Liabilities

Current Liabilities = $40,000 + $10,000 + $4,000

Current Liabilities = $54,000

Now that you know what the total current assets and total current liabilities are, the next step is to calculate the net working capital.

Net Working Capital = Current Assets – Current Liabilities

Net Working Capital = $75,000 – $54,000

Net Working Capital = $21,000

The online store has net working capital of $21,000.

If the company decides to use a more narrow net working capital, taking away cash and debt from the equation, here is how it will calculate it.

Net Working Capital = Current Assets (less cash) – Current Liabilities (less debt)

From the previous calculations, the current assets are $75,000 and the current liabilities are $54,000.

Net Working Capital = $75,000 (less cash) – $54,000 (less debt)

Also, the online store has $50,000 in cash and a short-term loan of $40,000.

Net Working Capital = ($75,000 – $50,000) – ($54,000 – $40,000)

Net Working Capital = $25,000 – $14,000

Net Working Capital = $11,000

The new working capital that excludes the online store’s cash and debt is $11,000.

Example 2

A retail grocery store in Ohio wants to calculate its working capital.

- Accounts Receivable: $5,000

- Inventory: $15,000

- Accounts Payable: $7,000

With the limited factors given, finding the working capital for this retail grocery store is best suited for the third net working capital formula.

Net Working Capital = Accounts Receivable + Inventory – Accounts Payable

Net Working Capital = $5,000 + $15,000 – $7,000

Net Working Capital = $20,000 – $7,000

Net Working Capital = $13,000.

The retail grocery store has net working capital of $13,000.

Example 3

A payroll software provider has a current net working capital of $1.5 million. Last year it had net working capital of $1.3 million. Here is how the payroll software will calculate the changes in its net working capital.

Current Net Working Capital – Previous Net Working Capital = Change in Net Working Capital

$1,500,000 – $1,300,000 = $200,000

The payroll software provider recorded a $200,000 change in net working capital.

Understanding the Working Capital Ratio

The working capital ratio is calculated by dividing the total current assets by the total current liabilities. Another name for the working capital ratio is also called the current ratio.

Unlike the working capital which is an absolute amount, the working capital ratio can quickly tell you if your company has enough current assets to meet its current obligations.

Calculating your net working capital alone may not give you a full picture of the financial health of your business. You need to use the working capital ratio for better insights.

The working capital ratio is a measure of liquidity. Businesses use it to gauge their ability to fulfill their financial obligations when due.

Here is the formula for calculating the working capital ratio.

Working Capital Ratio = Current Assets / Current Liabilities

A high working capital ratio boosts a business’s ability to carry out its day-to-day operations efficiently and expand its operations. Businesses need to track their working capital for better efficiency and results.

If your working capital ratio is reducing, it may be a sign that your company is getting into trouble. Businesses that track their working capital ratio can easily make moves to address the situation before it gets ugly.

The ideal working capital ratio varies depending on the industry and the circumstances the business faces.

If your working capital ratio is less than 1.1, it means you are struggling to meet your short-term current liabilities. If it is 1.1, it doesn’t mean you are out of the struggling zone yet, you are struggling to break even.

When the working capital ratio is between 1.2 – 2.0, your company is in an optimal or stable financial zone. However, you may still experience some levels of financial distress depending on how quickly you can collect accounts receivable and sell inventories.

A net working capital ratio above 2.0 means your business is not making proper use of its current assets. You need to re-strategize and make proper use of your current assets to boost your business.

Here is an example of the working capital ratio formula in use.

A business internet service provider has current assets worth $800,000 and current liabilities of $500,000. What is the company’s working capital ratio?

Working Capital Ratio = Current Assets / Current Liabilities

Working Capital Ratio = $800,000 / $500,000

Working Capital Ratio = 1.6

The business internet service provider has a working capital ratio of 1.6, which is an indication that it is making good use of its current assets.

How to Lower Your Working Capital Needs

Lowering your working capital needs is simply about increasing your current assets and reducing your current liabilities. Here are some of the best ways to lower your working capital needs and improve cash flow in your business.

1. Improve Your Inventory Management

Improving the way you manage your inventory can help lower your working capital needs. Inventory falls under your current assets. It consists of items that you have prepared for sales, used in production, and held for sale.

Stakeholders and investors check the company’s inventory to determine if it is viable enough for investment.

Although inventory falls under current assets, a large inventory can decrease your current assets if it attracts high maintenance and warehouse costs and possible spoilage. Here is where inventory management comes in.

Effective inventory management is an effective way of reducing your working capital needs and optimizing your working capital. Your company should produce inventory at the level of market demand, especially if you produce perishable items to cut down on current liabilities.

Managing inventory with manual methods is not only time-consuming but is generally not worth it. There are inventory management software providers that help you track and optimize every aspect of your inventory process. The inventory management software will save you from overstocking and alert you when your inventory stock is running low.

2. Manage Expenses Better to Improve Cash Flow

Cash flow is vital for almost any business. When you have a lot of current liabilities and you have lots of cash tied up in unpaid invoices or inventory, your business will struggle to meet its short-term financial obligations. A negative working capital scares away investors and shareholders.

One of the best ways to improve your cash flow is to manage your expenses properly. Reducing your expenses will help lower your working capital needs as it will save you the valuable cash flow that you need to run your business’s day-to-day operations.

Track all your business expenses to see if there are expenses you can do without. You can start by reviewing your monthly subscriptions. Thoroughly dispense of subscriptions and other expenses that are wasteful and not helping your business growth. Your goal is to reduce your expenses as low as you need to without affecting your company’s performance.

3. Incentivize Receivables

Too many businesses have money tied up in account receivables. Getting customers to pay on time can be a burden and lead to high demand for your company’s working capital.

You can lower your working capital demand by simply providing incentives for your customers to meet their payment obligations on time. Reward customers who pay on time and establish penalties for late payments. Ensure your customers are on board with such a policy to avoid ruining your working relationship with customers.

Properly investigate and check your customers’ creditworthiness before you provide goods on credit to them. It will save your business from attracting bad debts and negative cash flow.

4. Work with Vendors Who Offer Good Deals and Discounts

As a business, you always want to get the best deal. Doing business with vendors that offer good deals and discounts can help you lower your working capital needs. Having a good working relationship with your vendors and suppliers can also get you special deals and discounts.

If you can leverage early payment to get a discount, do it. You can negotiate your deals with your existing suppliers and vendors. Business is all about negotiation, do not shy away from negotiating better terms and pricing.

These discounts may seem small but they can save you some money which can help you handle your pressing expenses and debts. The money you save from getting good deals and discounts from suppliers will help grow your working capital.

5. Take advantage of Tax Incentives

Governments at all levels offer tax incentives for businesses. The first step in taking advantage of tax incentives is to know that they exist and are available.

You can check the tax collecting body’s website responsible for collecting your taxes for these tax incentives. Another option is to hire an accountant or certified public accountant (CPA) to help you leverage on possible tax breaks your company qualifies for.

Regularly paying your taxes can help you secure tax incentives such as reduced taxes, tax breaks, and favorable settlements in tax negotiations. Tracking your taxes early before it is due will prevent you from overpaying your taxes.

What About Negative Working Capital

Negative working capital refers to a situation in which your company’s current liabilities exceed its current assets. A negative working capital usually means that your company does not have enough cash to cover its short-term payment obligations such as payroll taxes, short-term expenses, and debts.

Stakeholders and investors favor a positive working capital as it assures them the company has enough cash to meet its short-term patent obligations.

Negative working capital can happen when a company makes large cash payments that deplete its current assets below its current liabilities. Also, if the company gets a large short-term loan, it can lead to negative working capital.

The working capital ratio or current ratio makes it easy to determine if a business has a negative working capital or not. If the working capital ratio or current ratio is less than 1, it means the business working capital is negative.

Not all negative working capital is bad. If the working capital is temporarily negative, it often means that the company has just spent lots of cash or increased its accounts payable. However, if the working capital is negative for extended periods, it is a sign that the company is struggling to meet its short-term financial obligations.

Some industries operate with negative working capital such as retailers, restaurants, and grocery stores. These businesses because of their nature of operations, negative working capital counts as a positive for them.

A negative working capital situation that is positive arises when a company collects cash upfront from customers and then pays the supplier for the goods supplied (which it sold to customers). It is an effective method of cash management as the company is using the vendor’s money to grow itself.

Dell Computers is a classical example of a company in which negative working capital is a positive. For years, Dell Computers collected cash up-front from customers but paid suppliers later, causing it to have negative working capital.

Sam Walton, the founder of Walmart used negative working capital to grow the company. He used the same technique of selling goods to customers (collecting cash immediately) and then paying the suppliers with the cash generated. Since he was able to generate high inventory turnover, he used his profits to expand his empire quickly.

Best Ways to Finance Working Capital

Your business can be flourishing and your working capital positive and then all of a sudden you start to face a cash flow crisis. Suddenly your working capital declines and without adequate working capital, you cannot operate your business efficiently or even expand it.

The option left to you is to seek loans from a bank. If you are a small business owner, the process of getting a short-term loan from a bank can be draining. Your business may not even meet the bank requirements for a loan. So what other options are you left with?

Here are some of the best ways to finance your working capital.ß

1. Trade Credit or Vendor Credit

You may be using this working capital financing option already. If you have purchased supplies or inventory from your vendor and have a 30, 60, or 90 days grace period to pay your bills, that is an example of trade credit.

This type of financing does not provide physical cash to you, however, it gets you the goods you would have spent a loan on. Receiving trade credit or vendor credit can make all the difference in your cash flow.

2. Business Credit Card

A quick way to finance your working capital is to get short-term financing with your business credit card. If you already have one, you can eliminate the process of applying and waiting for approval from banks and other financial institutions.

A business credit card gives you the option of either taking a cash advance or financing your purchase with the card. The only drawback is the high-interest rate and the extra charges for missing payments or paying below the minimum.

3. Business Line of Credit

Getting a business line of credit is a great source of working capital for your business. If you qualify for one, you don’t need to use collateral to collect the line of credit.

The best thing about the business line of credit is that you are not obligated to repay the money until you draw on it. For example, if you get a line of credit for $50,000 in January and draw it in September to buy products, you will not have to start repaying the line of credit until November.

For your business to qualify for a line of credit, it has to have an excellent credit score and a good track record of success.

4. Merchant Cash Advance Financing

If your business does a lot of credit card sales, this working capital financial option may appeal to you. This financing option allows you to take a cash advance against your business’s future credit card sales.

A percentage of your daily credit sales goes to the lender until your cash advance and the interest on the deal are fully paid.

5. Invoice Factoring

Factoring companies buy a percentage of the face value of your accounts receivable at a discount in exchange for cash.

The factoring company then collects the accounts receivable on your behalf, takes its fees and the initial amount you borrowed, and then returns what is left to your company. It is a quick way to get working capital financing without having to worry about repayment.

Continue Learning

- How to Calculate Working Capital

- Working Capital vs Investing Capital

- How to Calculate Operating Income

- Net Income Formula

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.