What is Accumulated Depreciation? Definition, Formula, Examples

As a business owner, you need to pay attention to your financial accounting to adequately keep track of your company’s financial records. Businesses prepare their financial records in the form of financial statements such as income statements and balance sheets.

Your company’s balance sheet can provide answers to many of the questions you have about your business’s financial health. Investors also pay attention to your balance sheet to determine how much money the company has and what it owes.

While there are many items on the balance sheet (all are important), one item you need to track on your balance sheet is accumulated depreciation.

In this article, you will learn everything you need to know about accumulated depreciation, how to calculate it, and the best accumulated depreciation calculators.

Let’s get started.

What is Accumulated Depreciation?

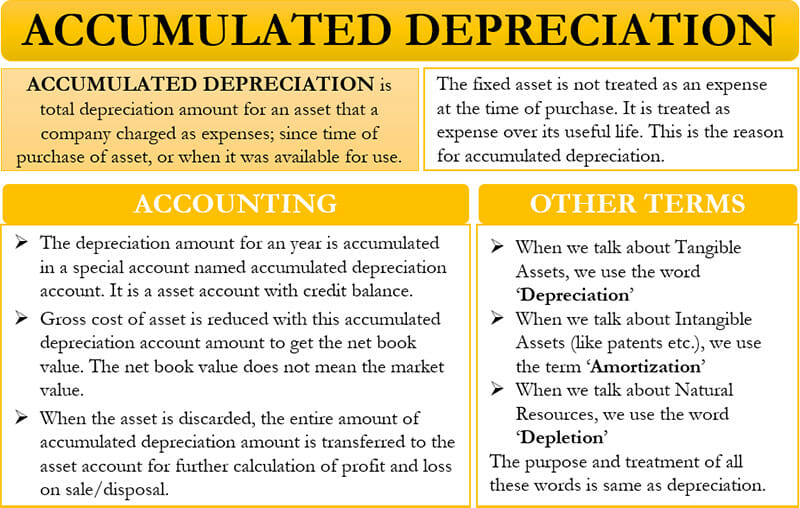

Accumulated depreciation is the cumulative depreciation of an asset up to a single point in its life. It is the total amount of a fixed asset's cost that has been allocated to depreciation expense since the asset was put into service.

With the exception of land which appreciates, all types of fixed assets wear out over time. As a consequence, they depreciate. As a result, depreciation is recorded to balance out the cost of using a long-term capital asset with the benefit gained from its use over time.

Calculating accumulated depreciation requires knowledge of useful life and the salvage value of an item. The useful life of an asset is the shelf life of the said asset and the salvage value is the expected value of the asset at the end of its useful life.

How to Calculate Accumulated Depreciation (Simple Formula)

There are two methods for calculating accumulated depreciation: the straight-line method and the double-declining balance method.

1. The Straight-line Method

The straight-line method is a simple method for calculating accumulated depreciation. It splits the yearly depreciation expense evenly over the useful life (usually years) of the asset. Unlike the double-declining method, it is very straightforward and only needs to be calculated once.

The formula for calculating accumulated depreciation with the straight-line method is:

Annual Depreciation = Depreciation / Years in Useful Life

Where:

Depreciation = Purchase Price – Salvage Value

Example

A gaming machine is bought for $10,000 with an estimated useful life of 8 years after which it will possess a salvage value of $2,000.

Annual Depreciation = Depreciation / Years in Useful Life

Where:

Depreciation = Purchase Price – Salvage Value

Depreciation = $10,000 – $2,000

Depreciation = $8,000

Annual Depreciation = $8,000 / 8

Annual Depreciation = $1,000

Using the straight-line method the annual depreciation is $1,000.

2. Double-declining Balance Method

The double-declining balance depreciation method is an aggressive depreciation approach. It doubles the regular depreciation approach to expend more depreciation costs in the earlier years of an asset’s useful life and less in the later years of the asset's lifespan. It is used with assets that lose a lot of value early in their useful life.

Here is the formula for calculating accumulated depreciation using the double-declining balance method.

Depreciation Expense = (2 x Basic Depreciation Rate x Book Value)

The basic depreciation rate is the same as the straight-line depreciation rate, while the book value of the asset is what it is worth every year after you write off the depreciation of the asset. This means the first book value is the original cost of the asset and it will continue to be reduced by a declining depreciation value each year.

To calculate the basic depreciation rate, you first have to divide the cost of the assets by the recovery period to get the basic yearly write-off. The cost of the asset is what you paid for an asset, while the recovery period refers to the period over which you are depreciating the asset in years. Another name for the recovery period is the useful life of the asset.

The formula for the basic depreciation rate is Basic Yearly Write-off / Cost of the Asset.

Example

Using IRS rules where vehicles are depreciated over 5 years, a truck bought at $15,000 would depreciate by $3,000 each year. What is its accumulated depreciation?

Depreciation Expense= (2 x Basic Depreciation Rate x Book Value)

The basic depreciation rate of the truck is: Basic Yearly Write-off / Cost of the Asset

Basic Depreciation Rate of the Truck = $3,000 / $15,000

Basic Depreciate Rate of the Truck = 0.2

The next step is to determine the book value of the truck. For the first year, the book value of the truck is $15,000. From this, we can calculate the double-declining rate of the truck in the first year using the depreciation amount formula.

Depreciation Expense = (2 x Basic Depreciation Rate x Book Value)

Depreciation Expense = ( 2 × 0.2 × $15,000)

Depreciation Expense = $6,000

Therefore, in the second year, the book value is reduced by $6,000 meaning your truck is now worth $9,000.

The depreciation in the second year is therefore calculated as:

Depreciation Expense = (2 x Basic Depreciation Rate x Book Value)

Depreciation Expense = (2 × 0.2 × $9,000)

Depreciation Expense = $3,600.

Subtracting the depreciation amount for the second from $9,000 will leave you with $5,400, which will automatically be your book balance for the third year.

Note that the double-declining method does not end at zero, even after its useful life. To close out the asset's journal, the straight-line method will eventually have to be deployed.

Recording of Journal Entries of Accumulated Depreciation

Recording accumulated depreciation of assets can be carried in a single journal designed to accommodate all types of fixed assets. Or it may be subdivided into separate entries for each type of fixed asset.

The reason for this is to adjust the book values of the company's fixed or capital assets. It also adds the depreciation expense of the current year to the accumulated depreciation account where the depreciation expense account will be debited.

Instead of expending the entire cost of a fixed asset in the year that it was purchased, the asset is depreciated, allowing the spread out of the cost so revenue can be earned from the asset.

Accumulated depreciation is a contra asset account and unlike a normal asset account, a credit to a contra-asset account increases its value while a debit decreases its value. Therefore, the accumulated depreciation account will be credited in the books of accounts of the company.

Recording accumulated depreciation as a debit entry creates a wrong impression of the asset being a liability to a third party, which is not the case. These entries are designed to reflect the ongoing usage of fixed assets over time. It is why assets like vehicles that will need more maintenance costs in the latter part of their useful life are usually calculated with the double-declining balance method.

The accumulated depreciation balance will continue to increase as more depreciation is added to it, until when it equals the original or desirable depreciated cost of the asset. At this point, the balance of the asset account becomes zero and there should be no more entries into the account.

Accounting for depreciation requires an ongoing series of entries to charge a fixed asset to expense, and eventually to derecognize it.

Best Accumulated Depreciation Calculators

Several online sites calculate depreciation accurately based on the data given to them. Some of the best accumulated depressions include CalculatorSoup, CalculateStuff, and Calculator Academy.

1. CalculatorSoup

CalculatorSoup is arguably the most elaborate accumulated depreciation calculator online. Not only does it calculate both straight-line and double-declining methods, but it also goes into detail to explain the variables that could be inputted into the calculator.

In addition, it provides a depreciation schedule as well as the opportunity to share your calculations on social media.

Secondly, it is a good calculator which makes use of the IRS-backed Modified Accelerated Cost Recovery System (MACRS) to calculate the depreciation schedule of depreciable assets.

2. CalculateStuff

CalculateStuff offers a variety of supporting information to make understanding depreciation calculation much easier. Their site also contains a graphical representation of the relationship between depreciation expense and the book value.

3. Calculator Academy

Calculator Academy is a free accumulated depreciation calculator which does not have the broad calculations and tutorials that the first two calculators.

What it lacks in quantity, it makes up for with ease of access. There is an easily available shortcut to allow users to switch between the straight-line and double-declining methods.

All three accumulated depreciation calculators provide ample examples of accumulation depreciation calculations. You can also use accounting software such as QuickBooks, Xero, FreshBooks, and QuickBooks alternatives to calculate accumulated depreciation.

Accumulated Depreciation FAQ

By subtracting depreciated value from the original cost of a capital asset, accumulated depreciation can indicate the book value of the asset. Being able to calculate depreciation is crucial for writing off the cost of expensive purchases, and for doing your taxes properly.

Accumulated depreciation is also important for calculating the taxable gain on a sale. It could help one avoid being taxed at the higher ordinary tax rate as opposed to the standard capital rate.

Accumulated depreciation can also be useful to calculate the age of a company's asset base, although this is mostly used for internal purposes and not disclosed to the public.

A decrease in accumulated depreciation will occur when an asset is sold or salvaged before the end of its useful life. At this point, the asset's accumulated depreciation and its cost should be removed from the accounts.

After this, the book balance should be compared with the proceeds from the sale to determine if profit has been made. If the amount received is greater than the book value, a gain will be recorded.

Depreciation expense is the cost that a business takes against its assets in each financial period reported.

Accumulated depreciation on the other hand is the total of depreciation expenses recorded over the useful life of an asset. So while the accumulated depreciation balance increases over time, adding the amount of depreciation expense recorded in the current period, depreciation expense declines or remains the same depending on the method of asset depreciation used.

Another important difference between the two is that depreciation expense appears on the income statement, while accumulated depreciation appears on the balance sheet.

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.