What is Managerial Accounting? Definition, Functions, Examples

Accounting is an important function that every business, irrespective of its size, should pay maximum attention to. Accountants and bookkeepers are responsible for compiling, measuring, and analyzing accounting records in the form of financial reports or statements for companies.

However, it can be difficult for internal managers in a company to interpret these accounting records compiled by accountants and bookkeepers because they are mostly aimed at external parties.

Managerial accounting involves the compiling, analyzing, and interpretation of financial records for managers. It helps managers make informed internal decisions for the benefit of the company.

In this article, you will learn the meaning of managerial accounting, how managerial accounting works, who are the users of managerial accounting information, managerial accounting vs financial accounting, types of managerial accounting, techniques in managerial accounting, and managerial accounting reports to know.

Let’s get started.

What is Managerial Accounting?

Managerial accounting is a branch of accounting that deals with the compilation of financial records for internal decision-making. It is also known as cost accounting or management accounting, and managerial accounting.

Another definition of managerial accounting is that it is the process of compiling, measuring, analyzing, and interpreting accounting records for managers to make informed business decisions in the pursuit of business goals.

For managerial accountants, the analysis of various accounting operations and metrics is aimed at extracting useful information for the company's management.

By analyzing the cost of each product, activity, and facility, among others, detailed and useful information is provided to the management of a company. These analyses are based on the budget of the company and business decisions are aimed at productively exploiting this.

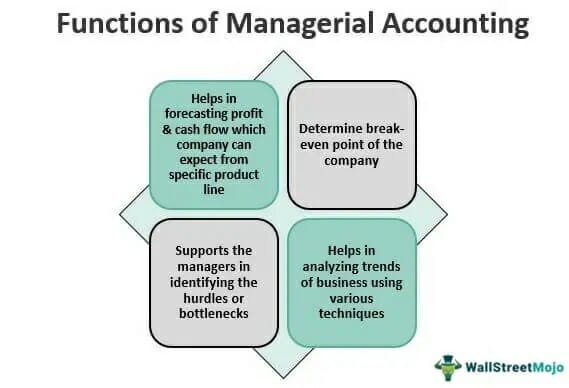

Managerial accounting is a very important accounting type for businesses in highly competitive business environments. It helps with operational data to quickly and easily make more accurate business decisions.

Overall, the goal of managerial accounting is to compare financial records with a company's budget and provide beneficial information for better internal decision-making and productivity.

How Managerial Accounting Works

Managerial accounting involves all areas of accounting aimed at providing useful information for better management of business operations. Accountants in this department make use of the cost of products and services, the sales revenue, as well as the budget of the company to generate useful information.

The area of managerial accounting that attracts the most focus is cost accounting. This includes financial records and accounts about the total cost of goods and services purchased by a company.

To give a good idea of how it works, here is an example.

If a company has a budget of $100 per week for purchasing a good and the weekly price of this good increases to $150, managerial accounting helps to provide quick information to go about this change.

The analysis would consider the cost of goods sold (COGS) and the revenue generated from sales and determine if the business can fund this price increase or if a cheaper alternative is better.

Without prior managerial accounting, the business may decide to go for a cheaper product which may affect the quality of products and, ultimately, the profitability of sales.

Managerial accounting only exists to help make these decisions much easier, accurate, and effective in relation to a company's budget and achieving business objectives.

Who are the Users of Managerial Accounting Information

Managerial accounting information is used by internal administrators of a business. These internal administrators include the general management of a company and the owner of a business to make better financial and operational decisions.

The management of a business makes use of the information to evaluate and analyze a company's performance and financial position. It also uses the information to make better financial decisions and prioritize business operations around fulfilling financial goals in terms of profitability and cash flow.

Owners of businesses invest capital in businesses and need accurate information to be able to access their level of profit or loss from their business operations. This allows them to know if business operations, as well as capital investments, need to be expanded or contracted.

Managerial accounting gives business owners appropriate information to make these important financial decisions.

For small or sole proprietary businesses, the owner of a business is usually part of the management. Nonetheless, information from managerial accounting is used by the internal administrators of a company that make the decisions.

Managerial accountants compile and analyze financial data and provide information for business administrators to use.

Managerial Accounting vs Financial Accounting

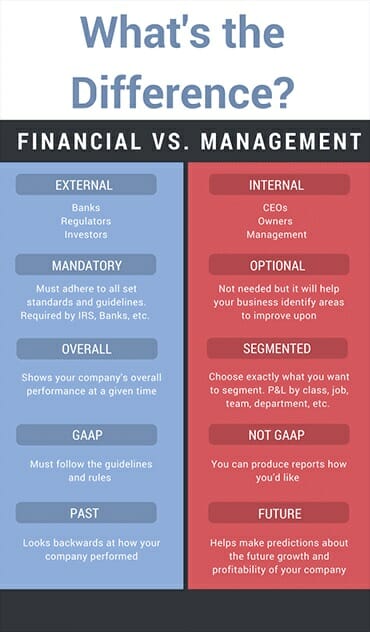

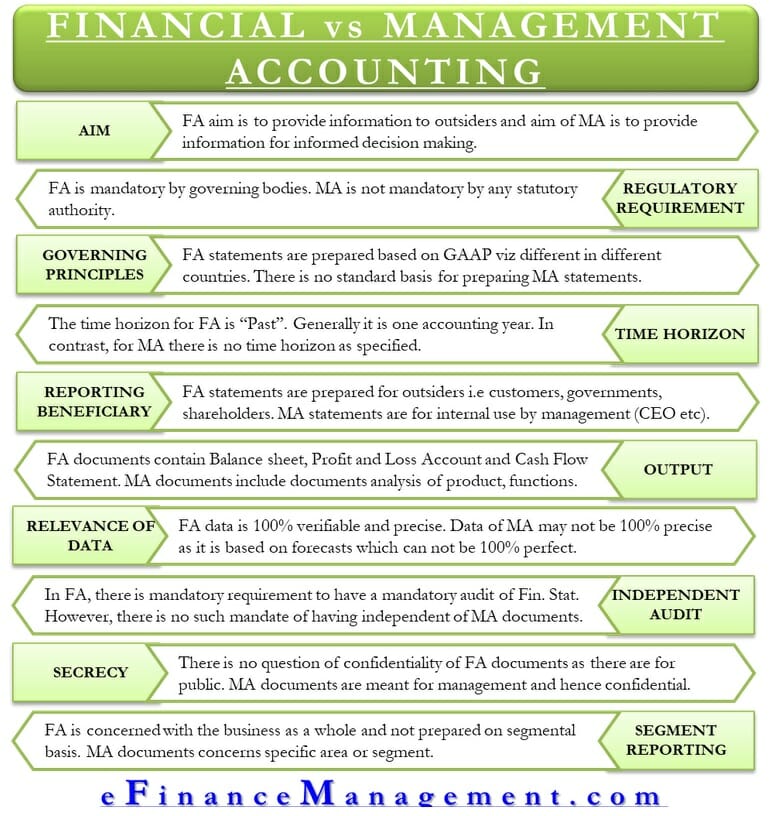

The main difference between managerial accounting and financial accounting is the users of the information generated.

Managerial accounting is intended for internal administrators of a business to make internal decisions.

Financial accounting, on the other hand, deals with financial records intended for external actors such as investors, creditors, or lenders. It aims to provide external parties with information about the financial health of a business

Apart from this, however, there are other grounds on which these two accounting types differ.

1. Presence of External Regulation

Financial accounting activities are regulated by external standards as opposed to the more flexible requirements placed on managerial accounting procedures.

External parties need to be protected from the incompetence of a firm as they are the main users of financial accounting information. Because of this, financial accounting procedures are required to fulfill certain standards set by regulatory bodies.

The Generally Accepted Accounting Principles (GAAP) set by the Securities Exchange Commission (SEC) and standards set by the Financial Accounting Standards Board( FASB) are the primary regulatory standards in the US.

Publicly held companies are required to complete all their financial accounts following GAAP standards to keep their public-traded status. Companies that also wish to get loans, entice investors, or fulfill debt covenants set by financial institutions also conform with the GAAP.

On the other hand, managerial accounting does not have to fulfill any form of general standards. Managerial accounting only has to fulfill internal standards and principles set to achieve business goals. Any set standard can be easily modified to meet the changing business environment and needs.

Standards relating to managerial accounting vary, not just from company to company but, even between departments within a company. Financial reports and data can be presented in any way, as long as the individuals intending to use them are satisfied and can use them to make decisions.

2. Futuristic Outlook

Managerial accounting compiles, analyses, and interprets data with the main aim of rendering decisions affecting the future of a company easier to make. The final interpretations presented to internal administrators offer clues to making accurate decisions that affect the future operations of a business.

Financial accounting, on the other hand, only aims to present information about the historical financial data of a company. It aims at presenting external stakeholders with information about the financial health of the company.

Financial accounting may seem to enable external stakeholders like investors and lenders to make more informed decisions but this is not the main aim for the company keeping accounts. A company may not need the help of external institutions and still engage in financial accounting activities.

Financial accounting is only aimed at keeping historical data about all the financial transactions a company has engaged in. It is responsible for producing financial statements for external use such as balance sheets and income statements.

3. Time for Generating Reports

The time when reports and statements are generated for use is different between managerial and financial accounting. While reports are only presented at the end of an accounting period with financial accounting, multiple operational reports are generated for managerial accounting.

An accounting period is usually set to be year-long and this could either be a regular calendar year or a fiscal year starting from a particular day. Financial accounting statements are usually run and presented at the end of this period.

Managerial accounting statements, on the other hand, are presented at any period of time that is convenient for the productive management of a business. They may be fixed over a period of time but this fixed period is entirely flexible and comes at different times and forms within a month.

With these, it is apparent that financial accounting statements are not useful for properly managing a business. Unlike managerial accounting statements that are compiled as at when needed, financial accounting statements are compiled too late for use.

Types of Managerial Accounting

Managerial accounting activities and operations come in different forms. Some of the most popular types of managerial accounting used by companies include product costing, marginal costing, cash flow analysis, inventory turnover analysis, constraint analysis, financial leverage analysis, and accounts receivable management.

1. Product Costing

Product costing is the process of determining the total cost involved in the production of goods and services. It is the process of tracking, recording, and studying every expense involved in the purchase and sale of goods and services including the cost of goods manufactured (COGM).

These expenses span from the cost of raw materials to labor costs to factory overheads and the cost of delivering goods to buyers or consumers.

Costs are broken down into four categories; fixed cost, variable cost, direct cost, and indirect cost. Product costing aims at identifying and distinguishing expenses into these categories for better understanding and analysis.

Managerial accountants exercise product costing in several ways. Overhead charges are determined for each product by dividing the whole expense by the number of goods or other factors like storage space.

Proper product costing allows a company to accurately estimate the cost and value of products in different stages of production. Product costing helps managers to implement pricing strategies that are beneficial to the company.

2. Marginal Costing

Marginal Costing is another type of managerial accounting that deals with the cost of goods. It involves determining the impact of adding one additional unit of a product to the purchase or production order. This impact is then measured in relation to the overall cost of production.

Making use of marginal costing is good for short-term business decisions. It helps to measure the amount of contribution a product has to the overall cost and profit of a company.

For managerial accounting, marginal costing works closely with break-even analysis. Additional products are added to determine the unit volume that makes the total sales revenue equal to the total expenses. This gives companies enough information in determining the price points of products.

Marginal costing also helps businesses determine the best use of raw materials and the optimal sales mix for products.

3. Cash Flow Analysis

Cash flow refers to the different inflows of cash into a company and outflows of cash from a company. Cash flow analysis is the examination of these inflows and outflows of cash during a particular period under consideration.

Managerial accountants engage in cash flow analysis to identify the impact of business decisions on the cash flow of a company. This cash flow concerns activities surrounding outflowing operational costs, outflowing investments, and in-flowing financing of a business.

Financial information is usually recorded on an accrual basis. Accrual accounting provides the financial position of a company at the end of a particular period. However, each transaction within this period is not accounted for with accrual accounting alone.

Cash flow analysis measures the impact of a particular transaction on the final financial position of a company. The cash inflow and outflow resulting from a single transaction are recorded and considered.

Proper cash flow analysis gives managerial accountants and administrators a chance to optimize the flow of cash within a company.

Optimization of cash flow ensures that a company has enough liquid assets to cover immediate expenses. Companies optimize cash flow so that they do not worry about future events and insufficient finances to complete them.

4. Inventory Turnover Analysis

Inventory turnover is a financial ratio that shows the number of times a company has sold and replaced inventory over a given period. Inventory turnover analysis involves the process of studying this ratio and coming up with enough information for better business administration.

Calculating the inventory turnover ratio helps companies to better determine the price of products and make better decisions on the production, marketing, and purchase of new inventory.

When calculating inventory turnover, two factors are important: the cost of goods sold (COGS) and the average beginning and ending inventory.

With inventory turnover analysis, managerial accountants can determine the cost of storing each unsold inventory. Optimizations can then be made to reduce the possibility or impact of excessive inventory.

5. Constraint Analysis

Constraints are limitations or restrictions that prevent a business process from fully materializing. Constraint analysis involves the identification and examination of possible bottleneck situations in the whole production line or sales process.

Bottlenecks cause delays in the business process of a company and can prove very costly in the end. The possible bottlenecks that may occur and their impact on the overall cash flow, revenue, and profit are determined by managerial accountants. Managers then use the generated information to optimize the whole business workflow to maneuver these constraints.

Constraint analysis is a crude process and constraints or bottlenecks can be inaccurately identified or missed entirely. So it is important that it remains as carefully executed and accurate as possible.

6. Financial Leverage Analysis

Financial leverage is the use of borrowed capital to increase the value of assets, investments, and return on investments. Financial leverage analysis involves the in-depth study of all the implications borne by a company after acquiring financial leverage.

Information comparing a company's debt and equity is provided by managerial accountants. These pieces of information help business administrators put financial leverage to their most productive use.

Information such as return on equity, debt to equity ratio, and total return on invested capital helps a company to properly manage the exploitation and repayment of financial leverage.

7. Account Receivable Management

Account receivables are the invoices or credits which a company expects to be remunerated by its debtors. The proper management of account receivables is an important form of managerial accounting.

Managing account receivable involves the process of ensuring that debtors pay their dues on time. It helps to prevent a company from running out of working capital to keep the business running.

Account receivables management also helps a company avoid situations of harmfully overdue payments or total non-payment of pending receivables.

Some of the different stages of this process involve determining if credit to a client should be extended, ensuring agreements are well documented, sending out invoices, sending out reminders, and increasing payment collection efforts, among others.

Techniques in Managerial Accounting

To provide as much beneficial information as possible, managerial accounting relies on a number of techniques. These techniques include forecasting, financial planning, and trend analysis, standard costing, budgetary control, funds flow analysis, and revaluation accounting.

1. Forecasting, Financial Planning, and Trend Analysis

Forecasting is the act of predicting how financial situations will shape the future. Trend analysis involves the study of patterns and trends of product costs to recognize reasons for unusual variances.

Forecasting and trend analysis work together in making financial planning easier and more accurate. Financial planning, accordingly, acts as one of the primary techniques of managerial accounting.

Appropriate financial planning helps a company to easily determine all its future needs. A company's future operations are also easily streamlined for achieving business goals and objectives.

Financial planning is a culmination of other techniques involved in achieving the internal goals of an organization. It involves the analysis of comparative financial statements and accounting ratios and the use of generated data to plan for the future.

2. Standard Costing

Standard costing involves the establishment of a standard total cost that is characteristic of efficient business operating conditions. Current costs of operation and goods or services are then compared to these standard costs.

With this form of comparative analysis, the variance between the standard cost and actual cost is determined. Problem areas are then pinpointed and remedial actions are executed to get things up to standard.

3. Budgetary Control

Budgetary control is another technique used for controlling costs in running a business. It is a technique used to guide and regulate the financial activities of a business.

Under budgetary control, future financial needs are documented alongside their costs and arranged in an orderly manner for efficient business operations.

Information related to capital expenditure is generated and analyzed. The crucial key metrics taken into account are the net present value (NPV) and internal rate of return (IRR).

Business operations are then executed in accordance with the estimated budget. The budget is usually based on or limited by the amount of capital a company has to invest.

4. Funds Flow Analysis

Funds flow analysis aims at providing an answer to the change in financial position as compared to other accounting periods. It compares the inflow and outflow of funds as documented in two comparative balance sheets.

Funds flow may seem the same as cash flow but they are differentiated on a very thin line. While cash flow involves all the cash inflow and outflow of a company, funds flow includes only the net cash within an organization that can be used as working capital.

This type of analysis tells where the flow of cash is coming from and how it is being used within a business. Proper funds flow analysis helps with future decisions on expenditure, comparative analysis, and the overall financial analysis and control of a company.

5. Revaluation Accounting

Revaluation is an accounting technique that involves the review of the recorded book value of an asset in relation to its true market value. Revaluation accounting is only used where the fair value of an asset can be reliably measured. A company then re-evaluates an asset in accordance with this fair value and ensures that the new valuation does not widely vary from it.

Revaluation accounting involves the act of recording increases or decreases in the value of a fixed asset. This accounting either credits or debits the asset account and any increase in value of an asset is credited into an equity account as a revaluation surplus.

Through this technique, managerial accountants ensure that the company's true capital is determined, preserved, and maintained. Financial statements are made more accurate and forecasts for future asset valuation become easier and more reliable.

Managerial Accounting Reports to Know

Reports generated from managerial accounting are done relative to the budget of a company. These reports help a business to understand how to allocate costs to stay within a budget while maximizing productivity.

Some of these reports include budget managerial reports, account receivable aging reports, performance reports, and cost managerial accounting reports.

1. Budget Managerial Reports

Budgets or budget managerial reports are reports on which other managerial accounting reports and activities are based.

A budget is generated by a business to create a financial framework according to which business goals can be achieved without overspending. It is usually based on past experiences and contains all the planned earnings and expenditures expected by a business within a period.

Operational and financial activities are streamlined in accordance with budgets and managers can cut costs and enter into contracts with vendors in accordance with it.

2. Account Receivable Aging Reports

An account receivable report is a periodic report that organizes a company's receivables according to the length of time the debt has remained unpaid. It helps a company to measure the financial health of its customers and determine the creditworthiness of each in case of future credit transactions.

Account receivable reports are important for companies that deal with a lot of debtors or lending institutions. With this report, you organize all the balance of credit receivable from your clients and can follow the periods allocated for repayment closely.

Outstanding invoices are tightly followed while debtors and repayment issues are easily identified. Cash flow policies are then revised to keep the company's budget workable.

3. Performance Reports

A performance report provides information about the outcome of an activity or the work of an individual. It compares the initial plan set out by a company with the current state of affairs, determining if business goals are being fulfilled or not.

The whole company, each department, and each employee in a company are considered in a performance report. It remains a good tool in properly managing business objectives and improving business workflow and day-to-day operations.

Underachieving departments and employees are provided with these performance reports and called to order according to their performance metrics.

Overachieving and constantly productive departments and employees are also easily identified, giving a company an idea of its most valued human assets.

Overall, performance reports help to compare the final outcome of a business workflow or operation with the initial budget and standard set for it. Decisions as to the future operations of a company are then easily carried out.

4. Cost Managerial Accounting Reports

Cost managerial accounting reports help businesses to compare the total cost of producing goods or services with the selling price for each unit. It contains all the costs for raw materials, overheads, and labor, among other additional costs in running a business.

With these reports, companies can determine the overall cost of production. Profit margins are then estimated and monitored in accordance with company goals. A proper understanding of costs and profit margins helps a company to optimize resources for increased productivity.

Some of the other managerial reports taken into account include competitor analysis reports, order information reports, and project reports. Apart from being internally generated, all managerial reports can also be outsourced to external expert institutions so that they remain as accurate as possible.

Managerial Accounting FAQ

The main objective of managerial accounting is to optimize a company's operating costs and maximize profits.

Managerial accounting involves identifying, measuring, analyzing, and interpreting an organization's financial statistics to provide actionable financial intelligence in terms of key metrics for managers. It offers suggestions on the economic decision-making process of an organization.

The job of a managerial accountant is to provide key insights that help a company's management team make many of its business decisions. They provide and analyze relevant financial and statistical data to be used in guiding the decision-makers of the company.

Aside from just crunching the numbers, managerial accountants also help companies choose and manage investments, as well as offer advice on financial decisions like budgeting.

The main difference between managerial accounting and financial accounting is the parties for which they provide financial information.

Managerial accounting varies from financial accounting in terms of its purpose. It provides internal managers or employees with useful insights that assist the organization's management in planning strategic operations. It helps them set realistic goals, and encourages an efficient directing of company resources.

Financial accounting is more concerned with providing insights to external parties such as investors and financial bodies. While it has internal uses as well, it aims to provide financial information on the organization's operations and financial well-being to financial accounting investors, creditors, and industry regulators.

Another difference in managerial and financial accounting is that managerial accounting is much less formal than financial accounting. Because management reports do not have to be issued to external parties, managerial accounting does not have a regulatory body like financial accounting where accountants have to follow GAAP standards in reporting financial information.

Four basic principles govern managerial accounting. The first principle is that the data provided by a managerial accountant should be relevant. They must provide managers with accurate, contextual, and up-to-date data that will provide vital insight into the cost model of the organization.

The second principle of managerial accounting is that the insight provided must be influential. By doing this managers can obtain the necessary data to inform their decisions.

Third, accountants must be able to analyze the efficiency of their managerial accounting operations and identify the scope for improvements.

By assessing opportunities and risks, they should be able to run simulations on the data to predict future outcomes and determine which outcome is best pursued. Results are not prioritized by what calculations are the most correct but by their impacts on the desired outcome.

Last, accountants should be able to garner trust from other departments through stewardship. It means diligently managing relationships and resources so that the assets and reputation of the organization are protected. Ethics and proficiency are important attributes for this principle.

Managerial accounting involves more than just calculations, managerial accountants must be able to deduce vital information from these numbers that will guide financial planning.

By studying management accounting we can cultivate skills that allow us to become strategic partners in a company's decision-making process.

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.