Net Sales vs Gross Sales: Definition & Ultimate Guide

As a business owner, you have your eyes fixed on your company’s revenue. One of your primary concerns is how to increase your company’s revenue. To effectively increase your company’s revenue, you need to measure your sales revenue properly.

Net sales and gross sales are two metrics that your sales team or business use to measure your company’s revenue. Many business owners can hardly tell the difference or misuse them. If you fall into these two categories, you are not alone.

In this article, you will learn everything you need to know about net sales and gross sales. You will learn about the differences between these two metrics and how to calculate them.

Let’s get started.

What are Net Sales?

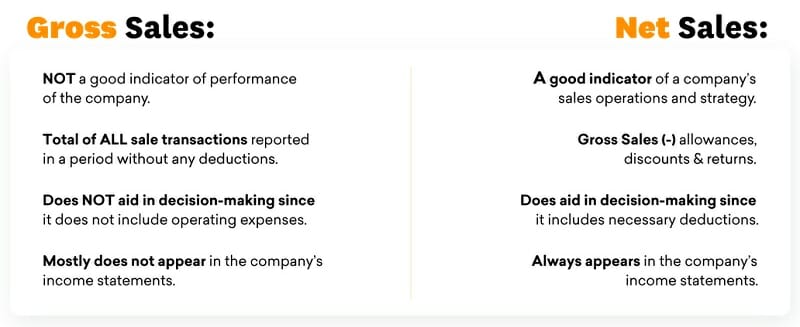

Net sales are the total of a company's gross sales excluding its sales returns, sales discounts, and sales allowances. It is the remaining portion of a company's revenue after deducting the allowances for damaged or missing goods. In other words, it is the amount of revenue reported on a company's income statement.

Net sales represent a portion of gross sales. It is derived from the gross figure which is the total income a company earns during a specific period. The period could be a quarter of a year, half a year, or a complete year.

At the end of an accounting period, businesses determine net sales by subtracting the total sales allowances, discounts, and returns from the gross sales. You cannot do proper financial accounting for your business without calculating net sales.

What is the Difference Between Net Sales and Gross Sales?

Gross sales represent the total money derived from all sales transactions within an accounting period – without deductions of any kind. Net sales, on the other hand, represents the total figure after the deductions have been made.

You can also say that net sales are percentages of the gross sales. The remaining percentage would be for the deductions.

Regarding the deductions in a company's account, the three major ones we talk about are sales discounts, sales allowances, and sales returns.

Sales Discounts

Discounts are given on sales either based on early payments, bulk purchases, or a good buyer-seller relationship. Oftentimes, the common cases are always based on early payments.

For example, if a buyer purchases your stocks on credit and manages to pay within the first 10 days of invoice issuance. He or she might be offered a percentage discount based on the former agreement between both parties.

Now, at the time of purchase, the seller does not know how many buyers would make early payments. So the discount is only offered at the time of receipt of cash from customers.

Sales Allowances

Sales allowance is a reduction in the price of goods paid by a customer due to minor goods defects. When cases like this happen, the seller offers a sales allowance after the buyer has purchased the goods in question. It is like compensation for the shortcomings of the goods.

Sales Returns

Sales return is a refund granted to a customer after they return whatever products they purchased to the seller. This works for businesses under the return merchandise authorization, that is, businesses that support the return of goods due to conditions like dissatisfaction, delivery error, and more.

These deductions make the difference between net sales and gross sales. If a company does not record sales allowances, sales returns, and sales discounts, their net sales value, and gross sales value will be the same.

How to Calculate Net Sales

The calculations of net sales can be derived from its different definitions. It is a function of the subtraction sign.

Mathematically,

Net Sales = Gross Sales – Returns – Allowances – Discounts, or

Net Sales = Gross Sales – (Returns + Allowances + Discounts)

The values in the bracket in the second expression represent the total deductions needed to be removed from the gross value to get the net value.

Net sales are always recorded in a company's income sheet. For companies that record the deductions, the gross sales and net sales will have to be recorded separately.

If the financial statements do not include the deductions, then the financial information will not be clear enough because it will not explain the status of each transaction – if discounted sales were more than the normal sales.

To have an understandable financial statement, the gross sales should be recorded, followed by the discounted sales, sales allowances grants, sales returns, and finally the net sales value.

Although this representation takes a lot of space, it also outrightly explains the quality of your transactions. So if a company wants to put them into separate columns, the accounting officer must understand how each transaction went so he or she can put it into the appropriate lines.

In some companies, it might be difficult for a financial analyst to calculate the net sales barely by looking at their financial statements. The income statements will be further broken down into direct costs, capital costs, and indirect costs. If income statements look this way, then the net sales will be under the direct costs.

From the calculation of net sales, it can be inferred that the difference between gross sales and net sales is the returns, allowances, and discounts.

If this difference is very much higher than the industry average value, then the company in question might be offering a very high discount on their goods or they experience a high amount of returns in a specific period.

The net sales revenue on your income statement shows how much revenue you have left after the subtractions of allowances, returns, and discounts.

Example Calculation of Net Sales

Example 1

Cole's gadget hub recorded gross sales of $200,000 for 6 months. During that same period, they had sales returns of $4,000, sales discounts of $10,000, and sales allowances of $6,000. The net sales for the hub during the space of 6 months are calculated like this:

Net Sales = Gross Sales – Returns – Allowances – Discounts

Net Sales = $200,000 – $4,000 – $10,000 – $6,000

Net Sales = $180,000

Example 2

Jimmy Forlan Company Ltd. is a retail company that sells all types of electronics, from televisions to radio sets, washing machines, pressing irons, dishwashers, vacuum cleaners, refrigerators, microwaves, gas cookers, ACs, and more.

However, the company had some downside moments when they had to refund some customers due to damaged goods. They also had good times where they offered discounts to esteemed customers.

At the end of the year, the company is about to release the financial statement for the just concluded accounting period and the accounting officer is to collate the financial sheets and calculate the net sales. The accountant, therefore, collects the invoice from the administrative office and the information in it includes:

- Sales Returns: $40,000

- Damaged Products: $10,000

- Discount of 10% at an invoice of $200,000

- Sales Returns: $10,000

- Discount of 5% at an invoice of $50,000

- Discount of 10% at an invoice of $80,000

- Damaged Goods: $50,000

The gross sales for that period were $850,000

To calculate net sales, we have to get the total sum of sales allowances, sales returns, and discounts.

Total Sales Returns: $40,000 + $10,000 = $50,000

Total Sales Allowances: $10,000 + $50,000 = $60,000

Total Sales Discounts: 10% of $200,000 + 5% of $50,000 + 10% of $80,000 and that is respectively $20,000, $2,500, and $8,000 to give a sum total of $30,500.

Therefore the net sales are calculated like this:

Net Sales = Gross Sales – Returns – Allowances – Discounts

Net Sales = $850,000 – $50,000 – $60,000 – $30,500

Net Sales = $709,500

These two examples are perfect illustrations of the difference between gross sales and net sales.

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.