Real Accounts – Overview, Types & Examples

Accounting is crucial for the success of every business. An effective accounting system for calculating financial inflows and outflows is necessary for hitting your financial goals.

Apart from the typical bank account, organizations use different types of accounts such as real, nominal, and cash accounts for different purposes. Real accounts differ significantly from nominal and personal accounts because they can serve as permanent accounts.

This blog post will teach you what a real account is, including the types and examples of real accounts.

Let’s get started.

Definition of Real Accounts

Real accounts keep the balance open at the end of the financial year, which means the closing balance is kept open from one accounting year to the following year.

A real account is different from other accounts like a nominal account and a personal account, mainly because real accounts roll forward and retain their ending balance at the end of the accounting year.

The balance becomes the beginning balance in the new year. Your beginning balance consists of the balance from your fixed assets, cash, and inventory accounts.

What Is A Real Account?

A real account is an account where the closing balance of the accounts in a particular accounting automatically becomes the opening balance of the next accounting year. It can also be called permanent accounts.

In other words, a real or permanent account is a general ledger account that is not closed but kept open at the end of the accounting year. The balance in the real accounts is carried forward to become the beginning balances of the next accounting period.

A golden rule when recording a transaction in a real account is to deduct or debit what comes in on the debit side and credit items that leave the organization on the credit side.

Another crucial bookkeeping practice involves recording journal entries in financial statements such as the balance sheet and income statement.

Your real accounts reflect your business's financial strength. They are subject to change periodically because these accounts are always active.

How Many Types Of Real Account Are There?

There are two types of real account use by businesses and organizations. These are called tangible and intangible real accounts.

1. Tangible Real Accounts

Tangible means anything that can be seen and touched or perceived by touching it. A tangible real account represents assets or objects that can be touched or tangible. Examples include fixed deposits, cash, stock, and land accounts.

2. Intangible Real Accounts

The word intangible refers to anything you cannot touch or anything that lacks a physical presence.

In the light of real accounts, an intangible real account refers to assets that do not have a physical presence or can not be touched. However, these assets can be measured in terms of money and greatly value the organization.

Examples include goodwill accounts, copyrights accounts, and trademarks.

Real Account Examples

To fully understand the dimensions of how it is applied, the few real account examples listed below will bring you up to date.

The items listed in an organization's financial statement are examples of Real accounts.

Assets

An asset is any resource the organization owns that has monetary value, which can also be used to generate revenue.

Assets are readily available to meet the organization's liabilities. They fall into two categories: tangible and intangible assets.

Tangible Assets

Tangible assets can be touched or have physical existence. They include cash, purchased furniture, inventory, building, accounts receivable (AR), and machinery.

Intangible Assets

Intangible assets can not be touched or felt, but these assets can be measured in teams of money, and they possess great value to the organization.

Examples include goodwill, patents, brand value, copyright, customer data, and trademarks.

Liabilities

Liabilities are recorded on the balance sheet's right side and could be legal or financial obligations an organization owes to someone or another company. They include loans, mortgages, accounts payable, bonds, warranties, and accrued expenses.

Stockholders Equity

Stockholders equity refers to the total value of assets that a company's shareholders have access to after the payment of the due liability.

In other words, stockholder's equity is the remaining assets available in the business after all liabilities have been settled or paid off.

Stockholder's equity is calculated by subtracting total liabilities from assets. Examples include retained earnings and common stock.

Journal Entries of Real Accounts

Let's take the example of Mr. John, who owns a large business in the real estate industry and owns various properties in various towns and cities.

To effectively run the business, he must give attention to the administrative aspect, which has a lot to do with bookkeeping, customer service center, smooth running of the office, and lots more.

To effectively run the office, he has to purchase certain vital equipment like furniture, cabinets, stationeries, etc. All the equipment purchased for the office cost $6,000.

To analyze the value of the equipment, you can consider the real accounts.

| Particulars | Amount |

| Equipments A/C …..Dr | $6,000 |

| To Cash A/C | $6,000 |

The two assets interact (cash accounts and equipment accounts) and are classified as real accounts in the above journal entry.

Firstly, the equipment account is debited based on the golden rule (debit what comes in), and the cash account is credited based on one of the golden rules (credit what goes out). Both accounts are reported on the balance sheet of the company.

Advantages of Journal Entries in Real Account

- Journal entries provided the closing balance of the liabilities and assets displayed on the balance sheet. They are rolled over into the next accounting year.

- Doing journal entries becomes easy because of the golden rule, which states that you should debit and credit what goes out.

- With the journal entry, the specific side on which the credit or debit is posted becomes clear and properly applied.

Disadvantages of Journal Entries in Real Account

- The organization will carry over any error in the closing balance of the real account in a particular year into the next accounting year. Because the closing balance of a particular accounting year is the opening balance of the succeeding accounting year.

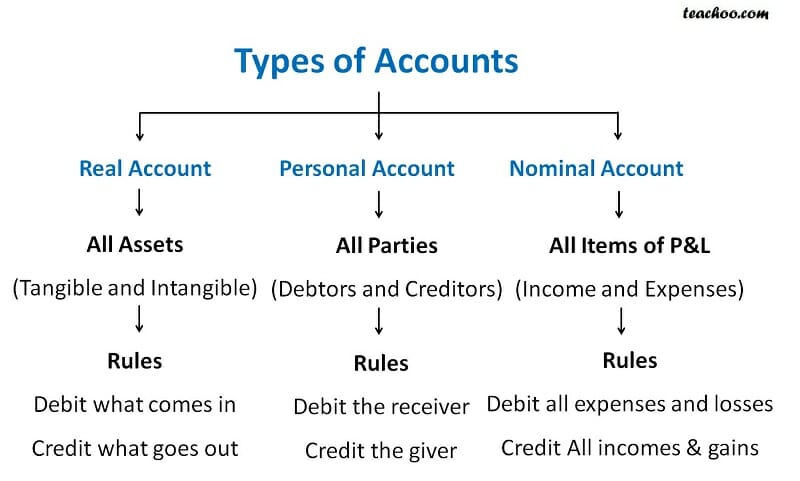

The Difference Between Real, Nominal & Personal Accounts

In accounting, accounts are grouped into real, nominal, and personal accounts. Based on the three golden rules of accounting, ledger accounts can be classified under the above examples, with each type having roles that they play.

1. Real Accounts

Real accounts indicate assets, equities, and liabilities such as gold deposits, inventory, bank, patent, and business loans. A major feature of this account is that it has accumulated balances that are rolled over to the next accounting year.

The Golden Rule for Real Accounts

Debit items that come into the organization on the debit side and credit items that leave the organization on the credit side.

2. Nominal Accounts

Nominal or temporary accounts do not accommodate any accumulated balances.

Instead, the account closes that same year without rolling over or keeping the balance sheet open till the next financial year and transfers the account balances to the income statement at the end of ther year, unlike real accounts.

Figures are recorded in the nominal account that pertains specifically to that particular year. The nominal account displays profits, losses, income, and expenses.

A nominal account generally represents the profits and losses that occur in a particular transaction and, when it is carefully accessed, points out if the company has succeeded in making a profit or has suffered losses that particular year.

For example, the nominal account determines if the company has a loss by displaying it in the fire account, rent account, interest received account, conveyance account, commissioned account, salary account, and discount received account.

The final result of every nominal account is either loss or profits, which are transferred to the capital account.

Golden Rule for Nominal Accounts

Debit all losses and expenses in the general ledger and, on the other hand, credit all gains and incomes.

3. Personal Accounts

As the name implies, personal accounts describe accounts specific to enterprises, institutes, people, and companies. These accounts can represent natural persons like Caleb's account and John's account.

Examples of personal accounts include banks, prepaid, debtor, creditor, and outstanding account.

Personal accounts can represent artificial persons like various par and credit bodies, an association of persons and companies. Representative personal accounts could include outstanding insurance accounts and wages payable accounts.

For example, if you pay salary in advance to a staff member, your accountant will open a wage prepaid account which is a representative personal account linked to the staff.

A personal account is similar to a real account because they both carry their balance to the next accounting year, except an individual has to settle the pending dues before it is carried into the next accounting year.

The Golden Rule for Personal Accounts

Debit the receiver on the right side of the general ledger and credit the giver on the left side.

FAQ

A real account is where the closing balance of the accounts in a particular accounting year automatically becomes the opening balance of the following accounting year. It can also be described as a permanent account.

A nominal or temporary account is a type of account where the closing balance does not stay open to be rolled over to the next financial year; this implies that the balance sheet is closed or balanced for that particular accounting year.

Goodwill is qualified as an intangible asset categorized under a real account.

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.