What is Financial Accounting? Definition, Principles, Examples

Financial accounting is one of the most important branches of accounting for businesses. Every business needs to accurately track its financial records. It is impossible to make accurate business forecasts and financial goals without knowing the business’ financials.

How much resources you allocate to the different departments in your company is determined by your financial accounting information. Financial accounting is what both internal and external shareholders use to determine the financial stability and performance of a business for the fiscal year.

In this article, you will learn the A to Z of financial accounting. You will learn the basics such as the meaning of financial accounting, how it works, why it is important, and the two types of financial accounting.

What are the differences between financial accounting and managerial accounting? What are the principles of financial accounting? You will also get an overview of the financial statement and a brief overview of the financial accounting standards.

Let’s get started.

What is Financial Accounting?

Financial accounting is a core branch of accounting that keeps track of a company’s financial records. It involves the whole process of summarizing, recording, and reporting multifarious financial transactions.

The financial transactions are prepared in the form of financial statements. Examples of financial statements are cash-flow statements, income statements and balance sheets. These financial statements are obtained from business operations over time and they can report the company’s financial performance for a specific time.

Financial statements show the summary of transactions, clients you had business with, date, time, and volume of transactions. Companies use their financial statements to show customers, investors, suppliers, employees, analysts, competitors, and clients their financial performance. Financial statements can help secure funding from potential investors to expand an organization.

Financial accounting gives internal board members and external stakeholders a brief about the financial health of a company. Therefore, the financial output depends on the business operations, the efficiency of workers, the value of assets, etc.

Organizations issue financial statements routinely. Financial accounting is done to give externals or recipients enough information to access and evaluate the worth of a business. Financial accountants can be found in both private and public organizations. Their duties are also quite different from that of a general accountant in a company.

Double-Entry Bookkeeping: How Financial Accounting Works

Double-entry bookkeeping is a small business bookkeeping basics that every business owner should know. Financial accounting works best under some established principles. The principles to use depend on the regulations in the accounting sectors of a country.

For example, companies in the US carry out their financial accounting operations in line with the Generally Accepted Accounting Principles (GAAP). These accounting principles are what guide the availability of information to creditors, investors, clients, stakeholders, and others.

The statements used in financial accounting present financial data in five main classifications for real accounts. They are assets, liabilities, revenues, expenses, and equity. Revenues and expenses are always reported under the income statement record.

With the use of financial accounting, you can determine the net income of a company from the income statement sheet. The other three financial data (assets, liabilities, and equity accounts) are accounted for under the balance sheet. A balance sheet can be used to determine the owner of a company’s economic benefits.

The financial accounting section of a business uses the double-entry bookkeeping system. That is, financial transactions are recorded using this system.

In an organization, ‘double-entry’ means every transaction that occurs affects two accounts (debit and credit accounts). For instance, if an organization borrows $75,000 from a microfinance bank, the company’s cash assets increase while its debt also increases.

The double-entry accounting format ensures entries on both sides of an account. A transaction is recorded as a debit in one account and simultaneously recorded as a credit in the other account.

Multiple entries on the debit side connote an increase in assets (what the company owns) and expenses, and a decrease in liability, equity, and income. On the credit account, multiple entries connote a decrease in assets and expenses, and an increase in liability, income, and equity.

The entries on the debit and credit sides must be equal. For any transaction, the debit amount must be equal to the credit amount. The double-entry bookkeeping format is one of the most efficient ways of recording a company’s transactions. It helps you keep tabs on the company’s present financial health and rate of financial growth. Also, it reduces human errors.

An advantage of the double-entry format is that, at any given time, you can tell if you have recorded a transaction on the wrong side. In that situation, the debit and credit entries would not be equal. Equal entries on both sides give a clearer picture of the financial state of a business.

Why is Financial Accounting Important?

Financial accounting is important to businesses for many reasons. Some of the reasons include tracking financial transactions, properly distributing resources in all areas of the business, communicating your business ideas to potential investors and creditors, strategic future planning, showing external parties the strength or weakness of your company, and for internal use

1. Tracking Financial Transactions

The primary reason why financial accounting is important to a business is to keep track of financial transactions. For that reason, a company can utilize the information in other areas of the business.

2. Properly Distributing Resources Across All Areas of the Business

Financial accounting helps businesses to make logical decisions on how to effectively distribute their resources. In your financial statements, you can infer that some areas need close monitoring than some other sections. With this, you can pay more attention to those areas.

3. Communicating Your Business Ideas to Potential Investors and Creditors

Another importance of financial accounting is that it helps you to communicate your business ideas to potential investors and creditors. When you have a clear representation of your financial data, it will be easier for you to convince investors when trying to secure funding.

Businesses rely on financial accounting as part of their pitch decks to convince investors and creditors about the viability of investing in them.

The different financial statements are enough to pass the necessary information that recipients need to know. It is what will either encourage or discourage them from partnering with you.

4. Strategic Future Planning

The management of a company uses financial accounting statements to resolve financial issues and also plan for the future. A financial accounting statement is required by the law in case there is legal action against a company concerning its income and expenses. Lawyers will be able to analyze the financial data of the company effectively using the financial statements.

5. Showing External Parties the Strength or Weakness of Your Company

Suppliers also demand to know a company’s financials before supplying goods and services. They do this to get assurance that the company has the financial ability to pay its invoices.

Financial institutions like microfinance banks also demand financial accounting statements from companies before they offer loans. Financial statements tell if the organization is capable of paying back whatever loan they borrow. If a company’s data is to be audited, auditors will make use of the financial accounting statements.

6. For Internal Use

Financial accounting is also important for internal use. Employees who are interested in stock-based compensation can also make use of the information gotten from financial accounting operations.

The financial accounting statements of different companies can be brought together and compared. With this, a standard method of analysis can be derived from different financial statements.

Types of Financial Accounting: Accrual Accounting vs Cash Accounting

There are two methods that you can use to perform financial accounting. They are the accrual accounting method and the cash accounting method.

Some organizations make use of either of them, while others use a combination of both. The major difference between the two methods of accounting is timing.

Accrual Accounting

Accrual accounting deals with the recording of financial transactions when they happen. By that time, the revenue is feasible. You can say it is based on anticipated revenues. The expenses are recorded when they are incurred and revenues are also recorded even before they are paid.

Large-scale businesses and public companies usually make use of this method. It presents a pragmatic financial overview for a particular period. With this method, you can easily make financial projections. Although it does not show the real cash flow, it can have unpleasant outcomes if you are not observant or sensitive enough.

Accrual accounting is like an extension of cash accounting. It involves credit, debit, and other forms of transactions. This type of accounting gives a clearer picture of the financial health of your business.

Cash Accounting

On the other hand, cash accounting involves the recording of financial transactions only when money changes hands (exchange of cash).

For this type of accounting, revenue is only recorded when there is a confirmed proof of payment like a receipt. Also, expenses are recorded when payment of supplies is made.

Unlike accrual accounting, revenue and expenses are recorded only when money has exchanged hands. Private companies and small and medium-scale businesses often use this method of accounting because it is quite simpler than the accrual method.

With this method, you can confirm the cash assets in possession by merely checking the account balance. You do not need any sophisticated calculations to know that.

A disadvantage of this financial accounting method is that you can not get a true picture of how well your business is doing. Your account balance may be weighty but you are into debt. By the time you pay all your debtors, you realize that you have little or nothing left to expand the scope of the business.

Cash accounting records financial transactions made by the members of the organization. For example, the expenses for business trips like meals, accommodation, and transportation, are recorded in cash accounting. After the transaction is made, they hold on to the receipts and report to the company’s manager.

In cash accounting, transactions are not recorded in financial statements but there is proof that a transaction has occurred.

Financial Accounting vs Managerial Accounting

Financial accounting is just one of the numerous types of accounting a business uses. Another popular accounting type used by businesses is managerial accounting.

There are clear differences between financial accounting and managerial accounting. As broad as financial accounting is, its operations are quite different from the operations of managerial accounting.

Financial Accounting

Financial accounting entails providing the necessary information to third parties outside the organization. The third party could be investors, creditors, competitors, suppliers, lawyers, and clients. Each of these groups of people needs your financial statements for specific reasons. Thus, it is important for every company, private or public, small or large-scale, to perform financial accounting.

The preparation of financial statements is done following some principles laid down by regulatory bodies and financial organizations. That is why the financial statements of different companies are compared so that a standard can be set. The standard is what every organization uses to prepare its financial statements.

Managerial Accounting

Managerial accounting is aimed at providing adequate information needed by the management of a company. The company’s management makes use of this information to make rational and data-driven decisions to move the organization forward. Unlike financial accounting, this information is always circulating internally and used by the management.

Managerial accounting does not operate on some laid-down rules or principles. The reason is that so many accounting rules do not fit into the operating style of some businesses. So, it is difficult for you to set rules for thousands of businesses – that operate differently – to follow.

In this case, the management of a company sets its rules internally and operates based on those principles. The principles are obtained from an internal analysis.

The major difference between the two types of accounting is who uses the information and what it is used for. Managerial accounting is solely for internal purposes while financial accounting is distributed to third parties outside the organization. Both have their importance to an organization and should be managed efficiently.

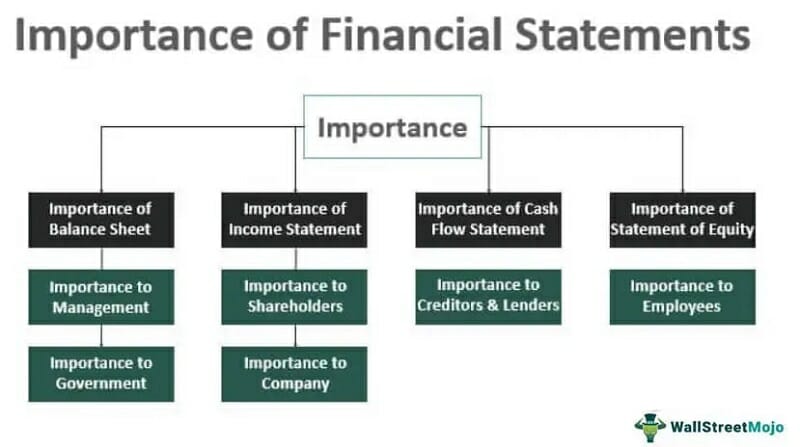

Overview of the Financial Statements

In financial accounting, transactions are put together in the form of statements. Oftentimes, companies put these statements together quarterly (four times in a calendar year) or annually. They make the financial statements available to their target audience, either the investing public or the regulatory bodies.

In the finance world, four fundamental financial statements are used to show a company’s financial performance or accomplishment. They are the income statement, balance sheet, cash flow statement, and statement of retained earnings.

1. Income Statement

An income statement, also known as a profit and loss statement, is the net income of a company for a particular period. The period could be a month, three months, six months, one year, twelve weeks, or any custom interval set by a company.

The fundamental components of an income statement sheet are revenue, expenses, profits, and losses. On an income statement sheet, you can calculate the net income by subtracting the total expenses from the total revenue.

Net Income = Revenue – Expenses

Revenues include interest revenues, sales revenues, and service revenues. Expenses include operating expenses (rent, utilities, salaries) and non-operating expenses (interest expenses), and cost of goods sold (COGS). An income statement reports the profitability of a company.

In line with the GAAP (Generally Accepted Accounting Principles), you should record the revenue during the period of sale of goods and services. That is, it may not necessarily be the same period when cash exchanges hands. An income statement can be called a statement of operations or a statement of earnings.

2. Balance Sheet

A balance sheet is a statement that records the assets and liabilities of a company at the end of an accounting cycle. It is also known as a statement of financial position. In other words, the balance sheet is a direct shot at a company’s financial health at any specific time.

On a balance sheet, the relationship between assets and liabilities is:

Assets = Stockholders’ Equity + Liabilities

A company’s assets can include cash, inventory, investments, vehicles, notes receivables, prepaid expenses, accounts receivables, and machinery. Liabilities include loans, accounts payable, current and deferred taxes, owed payroll, mortgages, and obligations.

Stockholders’ equity, also known as owners’ equity, is the number of assets available to a company after all liabilities have been settled or paid. It may include treasury stock, paid-in capital, comprehensive income, etc. Stockholders’ equity can also be gotten from stockholders who reinvest their dividends. The double-entry bookkeeping format keeps the balance sheet balanced.

3. Cash Flow Statement

A cash flow statement shows the amount of money going in and out of a company for a specific period. Unlike the net income, which is a non-cash number, the cash flow statement shows the actual flow of cash.

In a cash flow statement, cash flows can be from financing activities, operating activities, and investing activities. A cash flow statement shows the change in a company’s cash for a while.

Operating activities explain the change due to a company’s operations. Investing activities explain the change when the company records transactions involving long-term assets. Financing activities explain the change due to issuance of stock, issuance of debts, etc.

4. Statement of Retained Earnings

This financial statement is a sheet that shows the dividends paid to shareholders and the earnings withheld by the company. It is a financial statement that shows the changes in earnings over a specific period. Statement of retained earnings can also be called a statement of shareholder’s equity, statement of owner’s equity, or an equity statement.

Statement of retained earnings shows a company’s net income after dividends have been paid to shareholders. The earnings can be reinvested into the business or retained. This statement is very important to the shareholders in a company because it shows how much equity they hold in a company. Shareholders can know how much they are entitled to in a share by dividing the retained earnings by the number of shares.

A retained earnings account can show negative values if a company records large cumulative net losses. Items that affect a retained earnings account are operating expenses, depreciation, cost of goods sold (COGS), and sales revenue. You can reinvest retained earnings into assets but retained earnings are not assets.

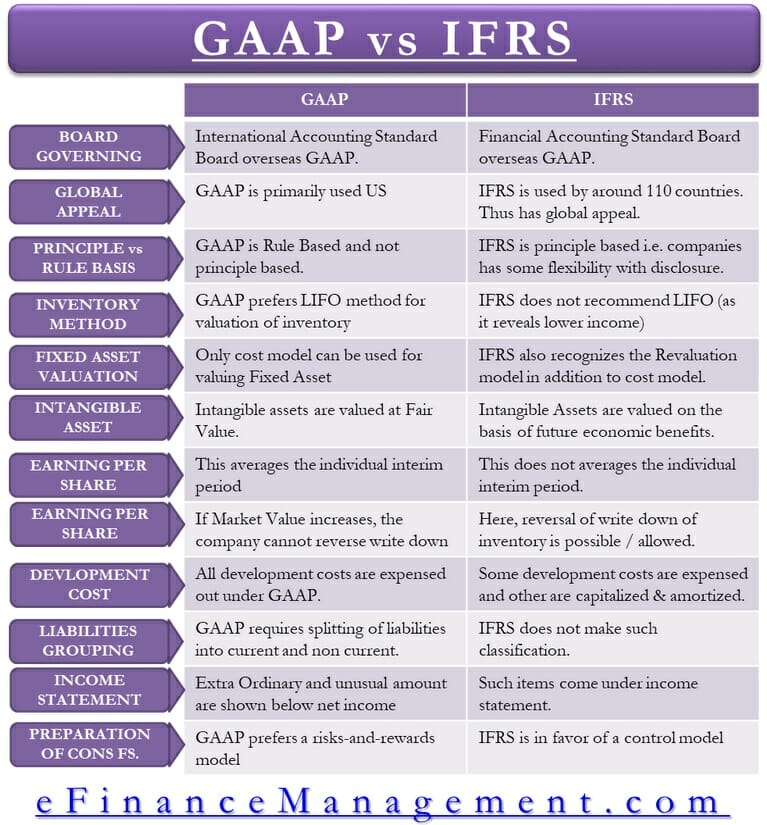

Financial Accounting Principles

For financial accounting to be functional, a company’s financial reports must be comprehensible, credible, and comparable to the reports of other companies. For your company’s reports to achieve this, there are some set of rules and principles called Generally Accepted Accounting Principles (GAAP) that it needs to follow.

GAAP are the rules that are applied to every financial statement issued by a company to external users or third parties such as investors, clients, creditors, competitors, and lawyers.

Note that GAAP applies to US companies, other countries have other financial standards they follow such as International Financial Reporting Standards (IFRS).

The Generally Accepted Accounting Principles (GAAP) entails some fundamental principles and concepts such as matching principle, full disclosure, cost principle, relevance, conservativeness, credibility, reliability, and economic entity.

1. Cost Principle

The cost principle is a financial accounting principle that records short and long-term assets at the amount they are worth (cash amounts). It entails that the accounting officer will record transactions at the specific time they occurred.

For example, if a client wants to get a car whose value is $20,000 for $15,000; the automobile company will record $15,000 as the amount paid on the balance sheet instead of the $20,000 which is the actual value.

Following this principle, a company’s most valuable properties and assets are not reported. Examples of these assets are search engine rankings, web domain names, trademarks, a team of employees, etc. Inflation and fluctuations in the market do not affect the cost recorded for an asset.

2. Full Disclosure Principle

The full disclosure principle states that a company should provide sufficient and necessary information that can aid the total understanding of their financial statements.

Since external users do not know much about the company’s operational activities, it is the work of the company to provide easy-to-understand information about the company.

The principle demands a company’s financial statements contain many schedules and disclosures in the notes. Understanding the details of a company is a key factor in the financial analysis of accounting statements.

3. Economic Entity Principle

This principle allows the financial accountant to separate the transactions of the sole proprietorship business from the sole proprietor’s personal transactions. Also, it means that the activities of a business entity should be recorded separately from the activities of the owner.

There are different varieties of business entities like a sole proprietorship, partnership, governmental agencies, or corporations.

The importance of this principle is to make accounting practices easier for external users when they receive financial statements.

4. Matching Principle

This accounting principle warrants you to use the accrual method of accounting instead of the cash method. The reason is, the company’s revenue must align with the company’s expenses. It means that the revenues and any other affiliated expenses should be recorded during the same accounting period.

The matching principle ensures consistency in the recording of financial statements like income statements, balance sheets, and others.

5. Relevance

For a company’s financial statements to maintain their relevance, they should be allocated to external users at the end of the accounting period. In essence, timeliness is a key factor in maintaining relevance too.

To achieve this, the accounting officer must close all financial statements promptly. The accounting officer must also be active at all times in a fiscal year.

6. Conservativeness

This principle allows the accountant to recognize and report expenses and liabilities when there are uncertainties, but still recognizes assets and revenues only when there is the certainty of possession. It allows clear recording even when uncertainties exist in financial transactions.

It is also a principle that guides an accountant to pick the alternative approach that yields lesser asset or income amounts when there are two acceptable methods of recording financial transactions.

7. Reliability

This principle guides the integrity of accountants. Accountants are expected to be unbiased and reliable. Every business audits its financial statements so that external users can be double sure that every figure in the statements is true and reliable.

Some of the effects of these financial accounting principles on financial statements are:

- The accrual method of accounting

- Revenues and expenses reported on the income statement

- Assets and liabilities reported on the balance sheet, and

- Stockholders’ equity is reported on the balance sheet.

These rules allow external users to make easy comparisons between the financial statements of different companies.

GAAP contains some complex and complicated standards that are set based on the analysis of some sophisticated business transactions. It also contains some accounting standards that are unique to specific companies, like banking and insurance. Due to these complexities, GAAP is always extensive and elaborate.

The Generally Accepted Accounting Principles (GAAP) also include some declarations issued by an accounting body known as Financial Accounting Standards Boards (FASB). It is a non-governmental group that inquires about current needs and creates accounting rules to meet those certain needs.

Brief Overview on the Financial Accounting Standards

Businesses and organizations need financial statements to introduce every necessary detail of their operations to external users. Oftentimes, internal users like the management entity also make use of the information in the statements to make financial decisions.

Financial accounting standards are the rules that govern the accounting operations of companies. They define the basis for financial accounting practices.

For a financial statement to be useful, it must conform to the accounting standards set by the accounting bodies in a country. That is, it must meet the necessary legal requirements. In America, the FASB (Financial Accounting Standards Board) set up financial accounting standards and principles known as Generally Accepted Accounting Principles (GAAP).

GAAP is a set of principles that governs the preparation of financial statements. They are usually used by both public and private organizations in the US. Every company in the US must follow these rules and principles to collate its financial statements.

These principles aim to improve the comparability, lucidity, and consistency of financial information. They are what guide every business on how to run their financial accounting.

The FASB (Financial Accounting Standards Board) set up these principles by gathering and comparing the financial statements of different organizations. It enables them to set a standard for everyone to follow.

International Accounting Standards Board (IASB) is another body that develops international accounting standards. International Financial Reporting Standards (IFRS) is the set of principles that IASB established to guide companies across borders. They make accounting across countries easier due to the increasing rate of global commerce.

Accounting standards handle every aspect of a company’s financial operation including the balance sheets, income statements, and others.

External users like banks, tax and regulatory agencies, and investors depend on these accounting standards to ensure that the information companies provide is accurate and credible.

Financial Accounting FAQ

The primary objective of financial accounting is to provide the necessary information about your business to external users like investors, clients, creditors, lawyers, auditors, and competitors. External users are a set of people that do not know much about your business, so you are expected to provide detailed information to give them an overview of your operations.

The external users all have different reasons for requesting your financial statements. Investors need to know if your business is worth investing in. Banks need to know if you are capable of paying back any loans they lend your business. Accounting bodies need to compare your financial statements with other companies so that a standard can be set for every company in that country.

Effective recording of financial transactions makes it easy for external users to comprehend the financial statements distributed to them. Here are a few tips on how to record your financial transactions.

Know and understand the types of accounting. Most accounting principles recommend the accrual method of accounting to accountants. But it is better if you understand the cash method of accounting. It gives you an advantage of a dynamic approach to tracking digital financial transactions. Also, cash accounting is a part of accrual accounting. So you will work best when you understand both.

Know the financial statements to utilize in your business. Oftentimes, some small-scale businesses can operate financial accounting practices without using all the financial statements. If you have investors to communicate with, it would be best if you use all the financial statements. It would show your transparency in recording business transactions, and transparency builds the trust investors have in you.

Always apply accounting principles. Learn to adhere to the underlying accounting principles. It is the best way to efficiently report financial records to external users.

Internal and external users make use of financial accounting information. Examples of internal users are company managers, owners, administrative boards, and employees.

External users are those outside the business entity, and they are creditors, clients, banks, competitors, tax agencies, and investors.

Financial accounting and financial reporting are somewhat related but are two different concepts. Financial accounting is a branch of accounting that keeps track of financial transactions. The transactions are prepared in the form of statements. The purpose is to distribute to external users who have one or two business deals with the organization.

Financial reporting is much broader than financial accounting. It does not include only financial statements but also entails a company’s annual report. It covers all the information for distribution to people outside the business entity.

Financial reporting includes financial statements, annual reports on conference calls and press releases, and annual reports for governmental agencies like the Securities Exchange Commission (SEC).

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.