What Is an Expenditure? Types, Differences, and Examples

Every business uses a general ledger to sort, store, compile, and summarize its financial records. Your accounting records consist of your income and expenditure. Understanding what these two terms mean and how they apply to your business is essential for proper management.

Unfortunately, not many business owners fully understand the concept of expenditure and how to manage it properly. Many mistake expenses to mean expenditure.

This article discusses the differences between expenditures and expenses and the different types and examples of expenditures.

Let's get started.

What is an Expenditure?

An expenditure is a form of legal payment to purchase goods or services offered by businesses, organizations, corporations, and individual buyers. This form of payment may be with cash or credit.

Generally, expenditures include Amazon purchases, paying for plane tickets, buying a burger, and salaries.

In the business world, expenditures benefit the company positively and move the business forward in various ways. For example, if your company executives decide to buy new stationeries and other office equipment to make the work smoother.

Smart business owners and employees keep a proper record of their expenditures irrespective of the range and the amount paid. Expenditure records must be accurate and timely and accompanied by an invoice or a sales receipt as proof.

The benefit of keeping records is monitoring cash flow, avoiding spending beyond the budget, and reducing operating expenses. In addition, this action helps anticipate profits and losses while keeping track of revenues.

Many small businesses and large companies struggle to accurately track their expenditures manually. The solution? Use accounting software to manage your personal and business finance quickly, accurately, and in real time.

Expenditures vs Expenses

Most people mistake these two words to mean the same thing, but there is a slight difference between an expenditure and an expense.

Expenditure refers to the entire cost of a purchase or liabilities incurred by an organization.

An expense is an actual payment the company planned for offsetting its revenue or income, which is recorded on the company's income statement.

A simple example of a company’s expenditure is the purchase of a truck for $20 million for transporting their finished product with an operating life of 8 years. This form of purchase is called capital expenditure.

Alternatively, the same truck bought at $20 million with eight years of operating life will have a depreciation expense of $2 million each year.

Types of Expenditures in Accounting

Companies, while executing their various tasks and activities, have to deal with two main types of expenditure. They are capital expenditures and revenue expenditures.

Without these forms of expenditure, you cannot successfully establish the business, begin production, and drive your growth.

Let’s take a closer look at these types of accounting expenditures.

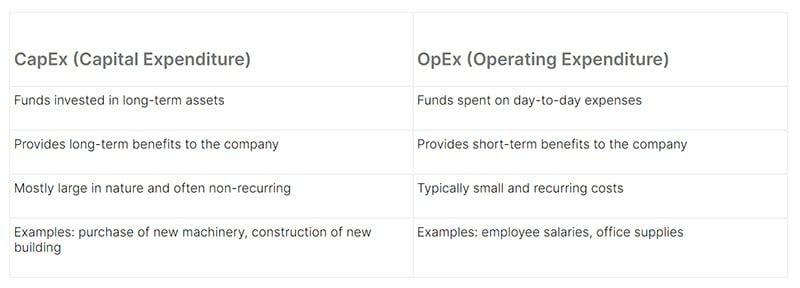

1. Capital Expenditure

In accounting, capital expenditures are costs a company incurs when paying for relevant assets with a lifespan of more than one year (non-current asset).

A business incurs capital expenditure after making payments to purchase capital-intensive assets like a building with a useful life that goes beyond one year.

For example, a company expands its reach beyond a particular region to diversify its business venture into other areas to earn more revenue. Carrying out this project is costly, and this type of cost is called capital expenditure.

When dealing with capital expenditures, begin with a major initial investment and subsequent expenses for continuous maintenance to ensure the new assets remain in good shape.

A unique feature of capital expenditures is that the existing assets offer the company long-term benefits.

The full cost of the assets cannot be deducted within the same financial year of its purchase. Rather, the company spreads the process through the life of the asset and shows it on the balance sheet under non-current assets.

Companies use debt or equity financing to settle capital expenditures due to the long-term benefit of spreading the payment process through the asset's lifespan.

Examples of Capital Expenditure

Example 1

John Sew Inc is a prominent fashion business in the UK. The company executives purchase new heavy-duty sewing machines to increase efficiency and revamp production.

- Based on their analysis, and projection, they can boost production by 30%.

- Based on the expenditure analysis, the total purchase price for these heavy-duty sewing machines is $500,000.

These machines are fixed assets and have a lifespan of at least 10 years, making them beneficial to the company over a long period. Because of their long lifespan, the company treats these assets as capital expenditures.

As time flies, John Sew Inc will depreciate the machine as an expense (depreciation).

Example 2

Big Bite is a fast-growing restaurant in the US with a lot of staff and a large customer base. The company is expanding its domain beyond its founding state Texas.

- The project manager of the expansion project wants the company to purchase a new building (fixed asset) to make the plan feasible.

- The cost of purchasing the building is $1,000,000, and the manager is confident that with the new building in operation, the company’s revenue will increase by 10%.

After purchasing the product, the useful life of the building is 20 years. Buying the building is a major investment for the company, but the benefit of this action spans many years and qualifies it as capital expenditure.

2. Revenue Expenditure

Revenue expenditure is the direct opposite of capital expenditure. With this form of expenditure, a company spends money to purchase new assets that are for the company’s use within a year.

These expenses are also known as short-term operating expenses. They are short-term purchases of goods or services for daily operations with economic benefit for the company within the same accounting period.

An example of revenue expenditure includes raw materials needed regularly for the production cycle to continue. The purchase of these raw materials occurs regularly. These materials have a lifespan below one year.

Here are the two ways a company can incur revenue expenditure.

- Cost of Sales or Direct Expenses: A company incurs direct expenses by purchasing goods or services relevant to production. They include raw material costs and direct labor costs required within the same accounting year.

- Operating Expense or Indirect Expenses: Indirect expenses are associated with running the company's operations. Examples include advertising costs, office rent, and utility bills.

Example of Revenue Expenditure Application

Example 1

Clear Imagination is a fast-growing photography studio. Due to its fast growth, the company regularly needs skilled photographers and established professionals ready to show up at work and get the job done.

The general manager in the company decided to employ twenty new photographers capable of completing tasks excellently to increase their over-the-counter sales. As a result, the company’s profit margins increased significantly.

These new hires increased the company’s labor costs. The wages of these photographers are continuous and commission based. The money spent on this expenditure is operating expenses that fall under revenue expenditures.

Example 2

Judy Cake Factor is about to launch a new batch of pastries to boost its over-the-counter sale strategy. During its testing phase, the company was able to attract the attention of various pastry lovers who are waiting for its debut.

After launching the new pastry, the demand has increased significantly, resulting in the constant purchase of raw materials like flour, sugar, milk, and eggs. The purchase of these resources in accounting terms is referred to as revenue expenditure.

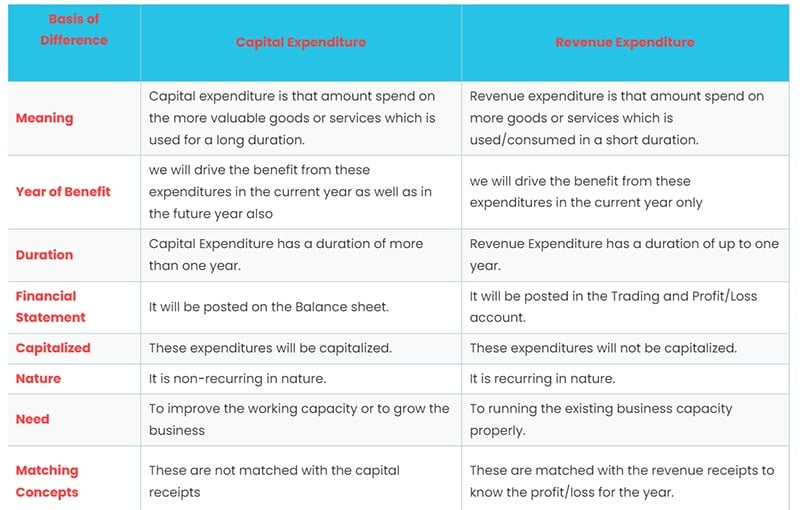

The Differences Between Capital Expenditure and Revenue Expenditure

3. Deferred Revenue Expenditure

Deferred revenue expenditures are also known as prepaid expenses or deferred expenses. Deferred payment is made in advance to acquire goods or services. They contribute to the increase in the asset value on the balance sheet.

With deferred revenue expenses, a binding agreement is present containing information about the contract.

Within this document, the agreement states that the company will offer an advance payment for certain goods and services they will receive in the future. This agreement gets recorded as a new asset until it’s time to receive the benefit.

The company documents the result of the arrangement to the profit or loss account over a period.

An Example of Deferred Revenue Expenditure

Jack's Bakery's special bread is one of a kind that has huge demand from various vendors, wholesalers, and consumers.

Based on the high demand, the manager chose an eight months advance payment for the supply of materials like sugar, flour, and oil.

The agreement mandates the supplier to deliver these materials in bulk every month and ensures the production process does not stop for any reason.

This prepaid or deferred expense is more cost-effective than paying for materials based on demand. The materials that have been paid for, but not yet delivered, count as a deferred revenue expenditure.

Explore Further

- What is Cost Accounting?

- Balance Sheet vs Income Statement

- Working Capital vs Investing Capital

- Small-Business Bookkeeping Basics

- How to Calculate Operating Income

- What is Accumulated Depreciation?

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.