Elements of Cost in Cost Accounting with Examples

In cost accounting, elements of cost refers to the components that make up the cost of manufacturing a product. The three main cost elements include material, labor, and expenses.

You can subdivide these elements into direct and indirect material, direct and indirect labor, and direct and indirect expenses. However, you can group the elements of costs into two categories: direct and indirect costs.

Direct costs include direct material, labor, and expense, which form the prime cost. Similarly, all the indirect costs, such as indirect material, labor, and expense, are also known as supplementary costs.

This article covers everything you need to know about the 4 elements of costs in cost accounting.

Let’s get started.

1. Material

Material refers to all the raw materials involved in creating a finished product, whether direct or indirect.

Types of Materials

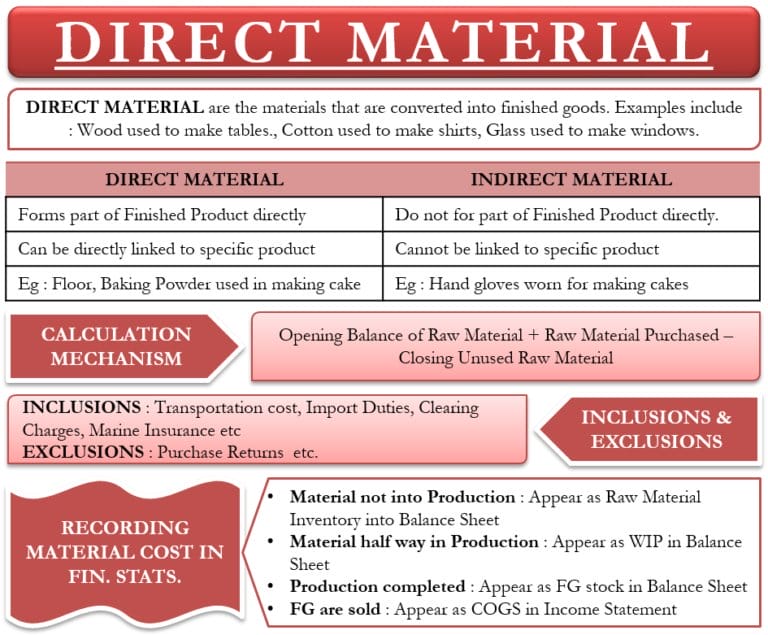

1. Direct Materials

Direct material cost includes all raw materials and goods a company requires to create its product. You can call them functional materials because, without these materials, there will be no production.

When considering direct material cost during production, remember that the overall cost depends on the company's output.

The most influential factor when considering the cost of direct materials is the output size. This direct cost comes in the form of process, stored, purchased primary packing, and production materials that’s integral to the success of every manufacturing process.

An example of a direct material is cotton in the production of clothing and textiles. Furniture-based organizations require direct materials like wood to execute production operations.

2. Indirect Materials

Indirect materials are resources or tools used in production that do not directly fluctuate with the output. In simple terms, indirect materials play a significant role in a company’s overall production process but are not integral to the furnished product.

A production company can function without these materials because the final product does not need them to be effective. Some examples of indirect materials include disposable gloves, personal protective equipment, tape, and nails.

Indirect material cost does not vary in direct proportion to the product. As a business owner, pay attention to the difference between these elements and their unique cost types to ensure you don't go overboard in costing and financial reporting.

Once you understand direct and indirect materials, you can seamlessly make informed decisions. For example, determining the total cost of production, setting selling prices, and analyzing the efficiency of the production process becomes easier and more accurate.

Your knowledge of direct and indirect materials is handy when making vital decisions like budgeting, cost control, and managerial decision-making regarding resource allocation.

2. Labor

Labor cost is vital in successfully executing an organization's production cycle. Human resources are among the most valuable resources that give a company an advantage regarding production. Without people, nothing happens in an organization.

The process of managing human resources requires proper cost allocation and informed decisions. In simple terms, labor cost refers to the amount an organization pays to workers involved in production. Labor in cost accounting includes direct and indirect labor.

Types of Labor

1. Direct Labor

Direct labor cost is remuneration paid to the individuals or staff producing goods and services. The amount you pay employees is directly proportional to the product output.

Most companies calculate the input these workers offer based on the overall output to pay them the amount due.

Direct labor cost refers to direct wages you can trace to specific products or services. Any form of salary paid to trainees or apprentices does not come under direct labor.

For example, in a food packaging production line, the workers assembling the food carry out direct labor. You can consider their wages as direct costs associated with the production of each food package.

2. Indirect Labor

An indirect laborer is an individual who supports the production process through supervision or monitoring but is not directly involved in producing goods or services.

Indirect labor costs are wages paid to dispensable workers in producing goods. Their work does not vary directly with the product output, which means a higher increase in production does not mean a pay increase.

An example of this indirect cost is the amount you pay interns for a particular job in a beverage company.

Remember that every manufacturing firm has key players, like maintenance staff, supervisors, and quality control inspectors. These staff members are not part of the production team, which means they do not get their hands dirty with the production process.

As long as they are staff members in a manufacturing firm, they will receive a salary, which is indirect labor costs.

A clear understanding of the difference between direct and indirect labor costs is your one-way ticket to accurate figures in cost accounting and financial analysis.

This information will make the process seamless when making managerial decisions concerning workforce allocation, productivity improvement, and cost control.

3. Expenses

Expenses are a vital element of cost in cost accounting. This type of cost centers around the amount an organization pays or spends during production.

In simple terms, expenses refer to costs incurred during production to generate more revenue, such as production costs.

Examples of expenses include payments to suppliers, employee wages, factory leases, and equipment depreciation. The prices of these expenses largely depend on the production level, whether on a large or small scale.

Types of Expenses

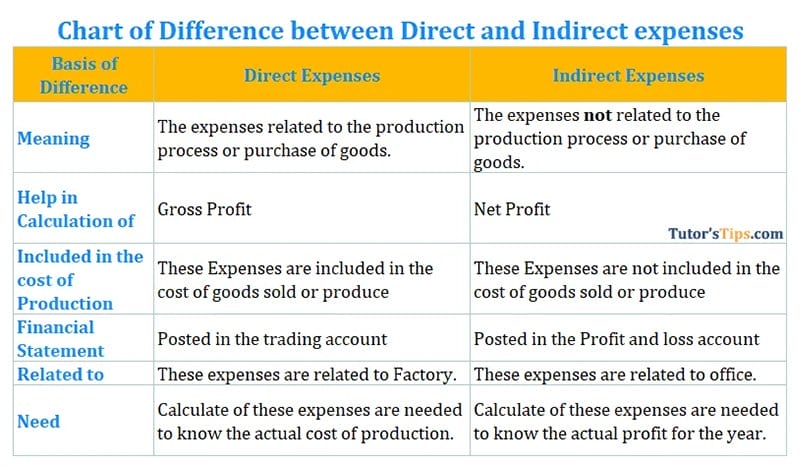

1. Direct Expenses

Direct expenses are known as chargeable expenses. They refer to expenses incurred during an organization's production process. Examples include the cost of goods sold (COGS), administrative fees, office supplies, direct labor, and rent.

Such expenses vary directly with the output, meaning the more you produce, the more money you spend. These expenses are specifically incurred and vital to the success of their production process. Without this manufacturing expense, the production of goods will not occur.

You must ensure you properly manage your direct expenses to seamlessly maximize profit without incurring loss.

2. Indirect Expenses

Indirect expenses refer to various costs incurred by an organization necessary for production. The difference between this form of expense and the direct expense is that there is no specificity to the indirect expense.

In most cases, the expenses occur outside the company's day-to-day activities and may be hard to track without proper assessment.

Indirect expenses do not vary with the output and are not easily identifiable. An example of indirect expense is the cost incurred for electricity during cloth manufacture, interest charges, and other costs associated with borrowing money.

4. Overhead

Overhead are indirect costs incurred in the production of goods in an organization. These costs are necessary for daily business operations.

You can define it as the summation of indirect material, labor, and expenses. In most cases, the cost and management accountants are responsible for running these costs.

Types of Overheads

1. Factory or Manufacturing Overhead

Factory or manufacturing overhead refers to a particular cost unit or indirect manufacturing costs incurred within an owned factory building.

Examples include factory rent, equipment depreciation, maintenance, taxes, and rates.

2. Administration Overhead

Administration overhead is a cost related to the administration of a company or organization. This overhead cost includes insurance, audit fees, stationery, and office salaries. Office cost is the summation of factory cost and administration overhead.

3. Selling and Distribution Overheads

Selling overhead refers to expenses in connection with sales in manufacturing operations. Examples are sales commissions, advertising costs, travel expenses, marketing materials, and customer entertainment.

4. Distribution Overhead

Distribution overhead refers to expenses involved from the time of the finished product to the time of delivery to consumers.

Examples are costs incurred during transportation, warehousing, packaging, and marketing. They are useful in calculating individual cost units.

Explore Further

- Best Accounting Software

- Variable Cost vs. Fixed Cost

- What Is an Expenditure?

- Business Cycle

- Working Capital vs Investing Capital

- Net Sales vs Gross Sales

- What is Financial Accounting?

- What is Managerial Accounting?

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.