Variable Cost vs. Fixed Cost: What’s the One Key Difference?

You don’t need to be a certified accountant to manage your small business finances effectively. Basic knowledge of cost accounting, the different cost types, and the most appropriate way to manage them are essential for running a business successfully.

This article will discuss the differences between variable and fixed costs and how they influence business activities.

Let’s get started.

Fixed Cost vs. Variable Cost

Successful businesses have to deal with various costs at different levels and degrees. In defining costs, we must be conscious that it is inevitable. No business can operate without incurring costs.

Cost is the total amount required for production and selling finished products. Every business attracts two main cost types during production.

- Variable Costs are flexible expenses that fluctuate depending on how much a company produces and sells. Variable costs are volume-related. They will increase when production rises and decrease when production decreases. Examples include labor, utility expenses, commissions, and raw materials.

- Fixed Costs don’t change based on the number of outputs produced (time-related expenses). This cost type is usually not subject to the company's business activities. Fixed costs will remain constant irrespective of production rate or output level. Rent, property tax, insurance, loan payments, and depreciation are examples of fixed costs.

Fixed and variable costs are relevant in financial accounting and managerial accounting and impact your financial statements significantly. They appear in vital accounting documents like your general ledger or balance sheet and income statement.

The combination of fixed and variable costs is called semi-variable costs. Since fixed costs do not fluctuate when production or activity volume changes, the fixed portion of a semi-variable cost remains the same; meanwhile, the variable portion of a semi-variable cost changes as production or activity volume rises or falls.

What are Variable Costs?

What comes to mind when you hear variable costs? Your first thought may be that the cost is not stagnant but changes depending on certain factors that can influence it.

In simple terms, variable costs are corporate or business expenses that fluctuate based on production and sales volume. They are referred to as prime costs.

If the production level is higher than its original state, the variable costs increase at the same rate and vice versa. Also, If the output is zero, then the variable cost will be zero.

Variable costs change with the output. If you want to calculate the total variable cost of your company, you will multiply the total quantity of output by the variable costs per unit of output.

Total Variable Cost = Total Quantity of Output x Variable Cost Per Unit of Output.

A simple example of variable cost is operational expenses. The operational expense of a business is subject to change as the business activities evolve.

Examples of variable expenses include wages for temporary staff and the cost of relevant utensils and utilities like electricity, gas, and water.

Types of Variable Costs

Variable costs contribute significantly to the overall business cost but come in different forms and types.

Let’s access some of the popular types of variable costs.

1. Raw Materials

A company's production process cannot begin without the availability of relevant raw materials. Raw materials represent a chunk of the overall production costs and overly business costs. They are passed to the final product the company launches for sale.

The volume of raw materials required for production output varies. If your organization does not have sufficient capital to purchase raw materials, the volume produced will reduce, and the total variable cost will also reduce.

On the other hand, if demand increases, the units produced will increase, and as a consequence, the total variable costs will increase.

2. Direct Labor

Labor costs are a significant variable expense a company cannot do without. An important ingredient in the production process is a reasonable amount of skilled workforce.

After employing, you have to pay an amount for compensation. The amount workers receive depends on the quality of work they do and their rank in the organization.

Direct labor cost varies. If you have temporary staff, you will not pay them the same amount as your permanent staff. Your company must have varying remuneration structures (hourly, daily, and fixed monthly salaries) drafted to compensate workers based on workers' input.

You may reduce the overall amount you pay your staff if you have an excess supply of workforce. Also, if there is less demand for your goods, you have to let some of them go.

On the other hand, if the demand for your product increases with less workforce, you may have to increase the pay or hire more workers.

3. Associated Charges, Fees, and Commissions

One constant thing about running a business is that you will incur costs at different stages and phases.

Your overall business strategy may help you outpace your competition, but it won’t save you from hidden costs like associated costs, fees, and commissions.

These costs will still arise irrespective of sales or business activities. For example, to increase sales and grow your business, you must offer discounts, sales commissions, and hidden fees to agents and distributors.

Hidden charges are examples of variable costs because they fluctuate and are influenced by various external and internal factors.

4. Utility Costs

Every production plant requires energy and other relevant equipment to go smoothly. Utilities fall under operating costs, and they don’t remain constant.

During production, you must pay to use electricity, water, gas, and production venues. On the other hand, you don’t have to pay utility bills when you are not using the services.

You may have to pay more utility bills if production increases due to higher demands for your goods. Also, when demand drops, production drops, and utility costs follow the same pattern.

The utilities an organization uses during production fluctuate and influence production, and in return, the variable costs change based on the volume of production.

5. Transportation Costs

You will experience variable costs while transporting the goods from one location to another. The amount you will pay to transport your goods depends on unique factors like location, packaging, and logistics.

While calculating these costs, you must consider certain expenses like freight, carriage, shipping, transit insurance, and the cost of operating the fleet.

Transportation cost varies depending on external factors like weather conditions, fuel charges, infrastructure, and conditions. For example, shipping costs can increase if the quantity of units shipped is large and vice versa.

Government policies can cause a major hike in the prices of transporting goods, causing the amount you are required to pay to vary at different times.

What are Fixed Costs?

Fixed costs are the total opposite of variable costs. They remain the same for a specific period without being influenced by the performance of the business or other relevant activities. Other terms for fixed costs include overhead costs, period costs, or supplementary costs.

Fixed costs are predetermined expenses. They are a normal part of every organization. Most businesses will have certain fixed costs whether a business is running or not.

The company can’t avoid paying fixed costs because of their adverse effects on the company's operations.

No matter how high or low sales are, fixed costs remain the same. However, these overhead costs make budgeting seamless because fixed expenses do not fluctuate throughout the financial year.

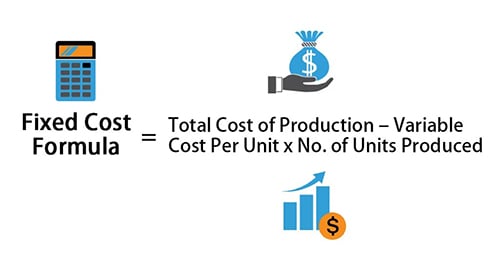

If you want to have a picture of your total fixed costs, calculate the sum of expenses your organization will incur if business activities stop. Bear in mind that fixed costs are not constant in the long run. The amount may change, but it is not as volatile as variable costs.

For example, let’s consider fixed costs like the company’s rent, which may be $10,000. If the facility owner decides to increase the rent at the end of the agreed term, the fixed costs (rent) will also change.

Types of Fixed Costs

Let's check out some of the most popular types of fixed costs an organization will always have to encounter.

1. Depreciation

Depreciation occurs when a tangible asset loses its value over time. This cost is a fixed expense because it doesn’t vary, and companies can use the amount depreciated to purchase new machinery after the old one turns into scrap.

Depreciation occurs in pieces of machinery and equipment due to constant use for business purposes.

2. Amortization

Amortization is the total expenses a firm incurs due to the existence of its various intangible assets. They include trademarks, copyrights, and patents. It is relevant in lowering the cost value of intangible assets.

3. Insurance

Insurance is a contract that gives its holder protection as long as both parties are faithful to their side of the agreement. The policyholder must pay a specific amount periodically for the agreement to stand. These payments are the company’s fixed costs.

4. Rent Paid

Every business needs a venue to conduct its activities, which requires some form of payment.

Rent is the amount a company pays for the facility the business occupies to carry out its activities. The facility's rent is not influenced by the company’s performance. The company will pay the same amount whether the business is doing well or not.

In addition, rent is fixed and is not dependent on the number of sales retailers make.

5. Interest Expense

Running a business is usually expensive, and most companies survive through loans. The implication of acquiring loans is that the company will be required to pay interest on the amount borrowed.

This interest expense is a fixed cost because it’s charged based on percentage and does not fluctuate. Other forms of borrowing include bonds, convertible debt, or lines of credit from banks and relevant financial institutions.

6. Property Taxes

Governments usually come up with different policies that will naturally affect business operations and running costs. A common example is property tax which is valued based on the total assets the company has.

The payment is made annually and usually the same amount, making it a fixed cost.

7. Salaries

If a business owner decides to pay workers monthly based on the work they have put in, the organization is running a salary system. The workers receive the same amount every month based on the original agreement they signed when they got employed.

Salaries are fixed costs because they don’t vary or are influenced by business performance.

8. Advertising and Promotional Expenses

There is no successful business that doesn’t invest significantly in advertising and promoting its goods and services.

This process causes a company to incur significant costs. These costs feature in activities such as print and broadcast ads, brochures, marketing campaigns, and catalogs.

The company may decide to increase its marketing efficiency through activities such as contests, focus groups, giveaways, and surveys that come under promotional activity.

All these activities are expensive to run, and they fall under fixed costs because the amount required to run them doesn't vary.

9. Equipment Rental

Not all businesses can afford to buy the required equipment. Some may decide to rent it because of the high cost of purchase. In this case, the company will pay a fixed amount for renting the equipment.

10. Legal Expenses

There are vital legal proceedings that every business owner must follow before setting up their business. Other legal fees will appear periodically, which the company has to pay. Such bills are fixed costs because they don't fluctuate and have a fixed payment date.

Special Considerations

Going beyond what we discussed earlier, let’s look at fixed costs and variable costs from a different angle.

Relevant Range

The concept of the relevant range is affiliated with both fixed costs and variable costs, but it's more pronounced when dealing with fixed costs.

Relevant range occurs when dealing with tangible products being converted into goods and labor costs. By implication, the total cost of production increases if you spend more time during production.

Wholesale bulk pricing gives a perfect example of the relevant range. The higher the volume of goods sold, the less the price.

For example, if you want to sell T-shirts for $10, the higher the volume of products you are willing to sell, the less the price, which means you will sell 50 for $9 each.

Degree of Leverage

When dealing with the degree of operating leverage of a company, both fixed cost and variable cost are major players.

The difference between fixed costs and variable costs in this regard is that fixed costs generate the company a higher degree of leverage. By implication, it leaves the company with greater upside potential. This result is risky and can have adverse effects on the company.

Alternatively, variable costs have a different trick up their sleeves. For variable costs, the result is not as risky as fixed costs because you generate less leverage, thus leaving the company with smaller upside potential.

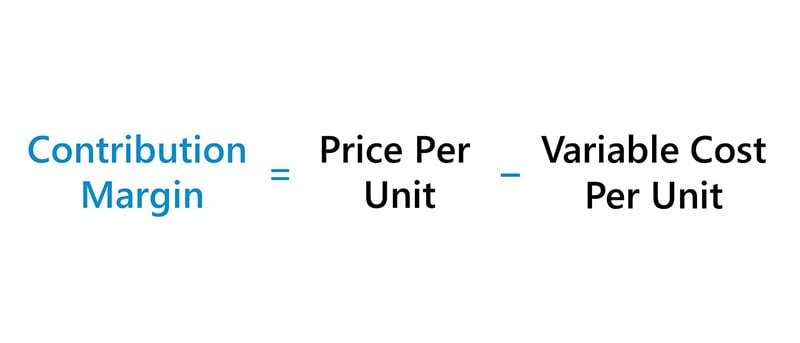

Contribution Margin

The contribution margin is the total amount a company earns after using sale proceeds to cover variable costs. Every amount of contribution margin goes directly to paying for fixed costs. After paying the fixed cost, the remaining income is considered profit.

Variable costs are vital to companies calculating their break-even analysis. With this component, they can determine their break-even point and sale targets for a specific profit target.

While determining contribution margin, both fixed and variable expenses are vital players, but variable costs are a direct input while determining contribution margin calculations.

Why Is It Important to Distinguish Between Fixed Costs and Variable Costs?

Fixed and variable costs evolve with changes in the volume and output levels. Determining the price level of your goods and services is easy if you understand the implication of these costs. This information helps to solidify your overall business strategy.

Fixed and variable costs serve as a solid foundation for various costing methods employed by businesses, such as activity-based costing, job order costing, and process costing.

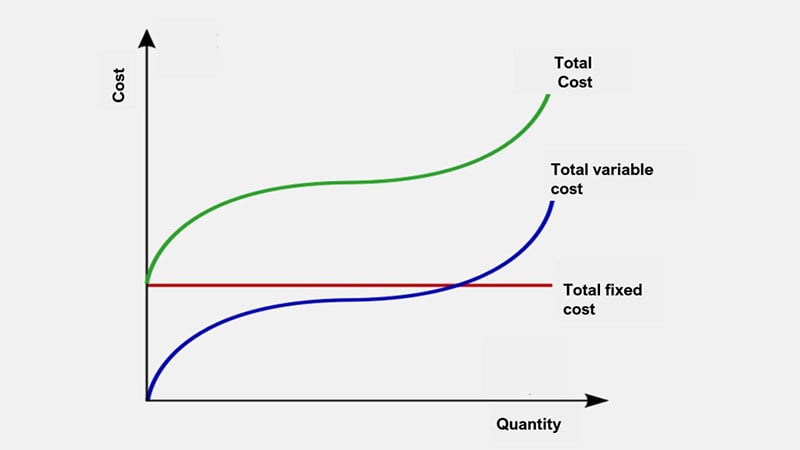

The Relationship Between Total Cost, Total Variable Cost, and Total Fixed Cost

Here are some significant reasons why it is essential to draw a line between variable and fixed costs.

1. Break-even Analysis

Profit is a vital part of the business. Determining profitable price levels becomes feasible with the knowledge of fixed and variable expenses.

The break-even analysis gives insight into where total revenues equal total costs and where your profit margin begins.

Here is the formula: Volume Needed to Break Even = Fixed Costs / (Price – Variable Costs)

The break-even analysis is an equation that offers business owners insight into the feasibility of a planned expansion. You can calculate a business’s project profit, number of units, and the dollar volume required to make a profit.

2. Economies of Scale

Determining economies of scale and the overall cost structure is easy with a clear understanding of fixed costs and variable costs.

With this insight, you can make rational decisions about business expenses, which helps to reduce losses and increase profitability.

Explore Further

- What Is the Cost of Goods Sold (COGS) and How to Calculate It

- What is Return on Investment (ROI) and How to Calculate It

- How to Calculate Cost of Goods Manufactured

- Best Accounting Software

- Types of Accounting Software

- How to Calculate Operating Income

- Small-Business Bookkeeping Basics

- Balance Sheet and Income Statement

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.