How to Grow a Small Business in 10 Easy Steps

Do you want to grow your small business from its present state to the top of the food chain? Starting a business can be challenging, but growing one into a huge success is even more difficult.

Entrepreneur statistics show that 20% of small businesses fail within the first year and 70% of businesses fail within the first ten years. You can have a different experience by putting the right strategies to work to increase your customer base and grow your business.

This article explores the 10 steps that show you how to grow your business to become a major competitor in your target market.

Let’s get started.

1. Create a Business Map

Many small business leaders begin their businesses with the sole aim of experiencing rapid growth and business profits without creating a solid business strategy or map. In reality, there is no successful business without having a concrete business map.

Imagine going on a journey or quest without a map. You will keep moving in circles and unable to focus on a particular direction or goal.

You probably have a business plan, but it is not the same as a business map.

A business plan is a strategic plan that describes a business's current state, aims, goals, and objectives. When writing your business plan, you have to answer the what’s and why’s of your business. Businesses use this plan to secure funds, monitor growth, and measure success.

On the flip side, a business map is a geographical visualization of a business’s current existence. This map shows you where you are and where your competitors and partners are.

Your business map includes the niche you want to focus on, your inspiration, and any strategic partnership you plan on venturing into.

With a foolproof map, you can identify the state of things in your business and create innovative ways to move your business in the right direction.

Benefits of Having A Reliable Business Map

- Identify Improvement Opportunities: A business map helps small business owners seamlessly understand and identify areas requiring adjustments. For example, customer retention, customer satisfaction, establishing retail stores, marketing strategies, and the need to practice corporate social responsibility.

- Offers Clarity to Business Operations: As a business owner, identifying key areas in your roadmap is vital to making productive moves. With a clearly defined business map, business activities will move in the right direction, and every stakeholder can make decisions based on the map.

- Offers Transparency to Customers: Customers prefer to do business with organizations with a well-defined business map. With this information, they can identify the production process that gives them a sense of recognition and satisfaction. Creating a concrete customer loyalty program is workable with this in focus.

2. Determine The Goals and KPIs Of Your Organization

Diving head-first into your business activities will make your goals and objectives impossible to achieve and cost more time and money.

If you desire to avoid making king-sized mistakes in growing your small business and getting more customers, carefully determine the overall business objectives and goals.

Stop in your tracks and ask vital questions by putting yourself in the customer's shoes.

- What do my customers want?

- What are their intricate needs, and are my products solving them?

- How will I stand out from competitors and make lasting impressions with my products?

- What more can I do to satisfy my present/potential customers and increase cash flow?

Do not ignore vital KPIs (Key Performance Indicators) for your organization and how they affect the target market.

Identifying KPIs involves setting targets or milestones and using them to measure the progress you are making with time.

Ignoring these strategies can affect the overall success of your organization and negatively influence customer perception and business news.

Top Organizations Goals and KPIs

- Financial Goals: The aim of starting a business is to make a profit, and this goal remains a core focus at every business stage. With strategic planning and commensurate action, your small business can set financial goals like reducing operational expenses, increasing revenue, and maintaining a positive cash flow.

- Customer Service Goals: These goals focus on increasing the strength and efficiency of the customer service services department to improve client satisfaction. On the other hand, it may be customer-centered and aim at improving customer experience.

- Employee Retention Goals: The effectiveness of your business is the result of the type of employee you have. You can set goals towards hiring more employees or hiring less with a specific skill set.

- Operational Efficiency Goals: You must set realistic goals to determine how efficiently your business runs. For example, you can set a goal to improve on-time delivery performance to customers or reduce energy consumption by 20 percent.

3. Know Your Customer Better Than Anybody Else

If you want to grow a strong client base, identifying and understanding your target audience is key. Many businesses use effective marketing strategies like lead generation that involve getting information about your target audience.

Business surveys are relevant in getting the data required to stir your physical and online business in the right direction and achieve great customer service.

Collating this feedback can help you streamline your products and services to meet the specific needs of your customers. This feedback prevents you from wasting your time and resources on people who would never require your services or products.

You can begin your research by asking who would most likely buy my products and why.

- What makes my company stand out from my competitors?

- Would I choose my product if I was a potential customer?

- What are the pain points, and why do current clients keep leaving?

Answering all these questions gives you an understanding of your ideal customer. You can seamlessly create a strong customer base and increase your company's market share.

If you can know and make your customers happy, they will spread positive messages about your business, giving you all the social proof you need.

Types of Customers

Knowing the different types of customers and how to approach them will help you grow your small business.

- Loyal Customers: These customers are vital to the growth and stability of your own business because they will always come back for more products or services. They usually make up a minority of the customer base but generate a huge portion of sales.

- Impulse Customers: Usually clueless and do not have a specific product in mind, but they will go for any products that appeal to them emotionally. They are targets in marketing efforts because of their likelihood to respond impulsively.

- Discount Customers: These customers get moved by markdowns and will only purchase with significant discounts on each product. Discount customers are the least loyal segment of customers, always looking for the cheapest store.

- Need-Based Customers: You will not see a need-based customer except if you have the specific product they want. Customers buy a product and nothing more. You can make them loyal with strategic email marketing campaigns.

- Wandering Customers: They make up the biggest chunk of the business’s customer base but contribute the smallest percentage of sales revenue. Wandering customers have no specific need but are primarily attracted to the business's location rather than the products.

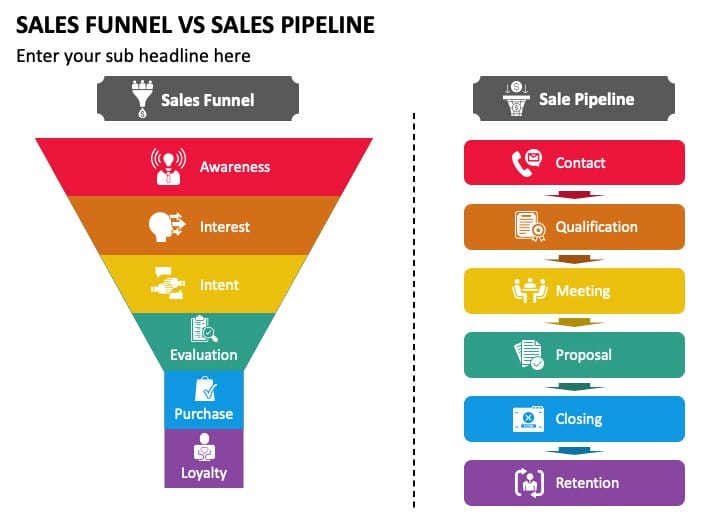

4. Build A Sales Funnel

A sales funnel paints a picture of the sales journey. The funnel begins when a potential customer contacts your product or service via physical or digital marketing before purchase.

Building a sales funnel helps you know how your potential clients feel at every point in their purchase journey. You have a responsibility to identify their pain points and proffer solutions to them for fast business growth.

Steps in Building A Sales Funnel

- Awareness: The first step of a sales funnel is when people make contact with your product or service like seeing it on search engines like Google or from a previous customer.

- Consideration: At the interest or consideration phase, your potential clients are willing to learn more about your product or service with the aim of purchase. You can give them access to this information by publishing a blog post with valuable insights on your product.

- Desire: The third step of the sales funnel is the point where they decide to purchase. In this stage, they compare your services or products and decide if it is the best option for them.

- Action: This phase can go both ways. Potential customers can choose to make the purchase or leave without purchasing. If they do decide to make the purchase, the sales funnel doesn't end here, you have to work on retaining the customers.

- Loyalty: The loyalty phase is known as the retention stage. This stage focuses on turning one-time buyers into repeat customers. At this phase, customers are satisfied with the services and products and are willing to return for more.

5. Increase Customer Lifetime Value

Every business owner wants new customers, but that doesn’t mean you devalue your existing customers. Getting new customers is good for the business and a great experience. You can increase your revenue by managing your current customer base effectively.

Your Customer Lifetime Value (CLV) and Customer Acquisition Costs (CAC) are vital KPIs every business should actively track and not just leave for the marketing or sales team.

Customer Lifetime Value (CLV) refers to the gross profit you can earn from a customer on the strength of your customer-business relationship.

For instance, if a customer buys your product for $100 and comes back to buy that product five more times in one year, the CLV is $500.

On the other hand, Customer Acquisition Costs (CAC) are the total amount of money a company spends to earn new customers over a period.

If you want to enjoy fast business growth, your Customer Lifetime Value should be at least three times your Customer Acquisition Costs.

You can increase your Customer Lifetime Value by offering sustainable products and great customer service. Strategic partnerships also increase your CLV by raising brand awareness.

Listening to customer feedback helps to identify their pain points and the best way to meet their needs and keep them loyal to your small business.

Offering quality customer service and support will ultimately influence your Customer Lifetime Value. Ensure every customer who comes in contact with you has a pleasant and satisfactory experience.

If you execute these strategies, the result will be a significant increase in your Customer Lifetime Value and more loyal customers.

6. Increase Employee Productivity

An essential ingredient for business growth is to map out strategies for increasing productivity. A friendly workplace environment where people can share ideas and contribute to business growth is an excellent way to maintain success.

How to Increase Employee Productivity

- Hire the Right Employees: Having the ideal set of people on your team is essential. According to Employee Productivity Statistics, talented employees are 8x more productive than the average. You can use freelance job websites and online job boards to find relevant workers that align with their company’s vision.

- Provide Valuable Insights and Track Progress: Don’t assign tasks to your employees and fold your arms while expecting maximum results. Provide valuable insights regularly and be a part of what they do. You can execute vital activities like setting daily, weekly, and monthly goals and creating tracking systems to ensure they achieve them.

- Set Up a Reward System: Provide incentives and rewards from time to time to help boost your employees’ morale and ultimately their productivity levels.

- Prioritize Quality over Quantity: Most times, workers tend to prioritize quantity over quality. Stand out in the market by ensuring your company prioritizes quality. Potential clients will identify with you by testing your product or service and proving its quality.

- Invest in Employee Education: Organize courses and sponsor training and trips for increased learning. Attending networking events will provide opportunities to check out productivity hacks working for other businesses.

- Learn from Past Employees’ Results: You can continually implement strategies by accessing past results and checking out new workplace productivity tips.

- Make Relevant Tools Available: Employees tend to function well when they have the tools needed for effective output. Your workplace must be conducive to help you remain at the top of your game. You can use productivity tools like ClickUp and Monday.com to maximize team results.

7. Invest in Technology that Makes you Faster and Efficient

The world is advancing faster than you think. As a small business owner, you must always be on the lookout for new ways to be more efficient and effective. Large companies like Apple, Samsung, and Dell effectively use technological advancements to remain where they are.

Slaving your employees by making them work six hours on a job they could have finished in an hour is a complete waste of time and human resources.

You cannot rely on outdated technology if you want to compete and achieve faster results. Sharpen your ax so you can produce more and increase your market share.

No one likes repeating the same job manually over time, this process dampens the spirit. Make use of tools like automation technology to accelerate production and delivery processes.

For example, new businesses can use AI-powered assistants and marketing automation tools to help in lead generation and cloud computing for storing remote data.

Investing in technology would make your business more efficient, produce quality goods, and keep it ahead of competitors. Your employees will spend fewer hours doing manual tasks and focus on more productive tasks with the right technology.

8. Explore Cheap & Highly-Converting Market Channels

Every business owner desires customers to keep flooding the company and buying products at an increased rate that brings in more profits. But guess what? You cannot increase sales without strategic marketing.

Smart small businesses use search engine optimization (SEO) to increase the rate of traffic to their website and blog posts. But SEO is just one of many cheap and highly-converting marketing channels. Another popular example is word-of-mouth marketing.

Providing great service and satisfying current clients will help you significantly. Always remember that people will generally tell others about a product that satisfies their needs, and will spread the news like wildfire.

Social media marketing is an excellent marketing channel to find potential clients. To grow a startup, you must have credible social proof that boosts your brand’s image. Social media platforms like Instagram and LinkedIn are great places to set up your brand.

Market channels like content marketing, such as podcasts, videos, and articles help to attract and retain the target audience for your product.

In the early stages of your business, email marketing will help you build a loyal customer base. With email marketing, you can always update clients about new product releases.

You can get their opinions and pain points concerning your service or product which when worked upon will certainly accelerate your growth.

9. Diversify your Products or Service Offerings

What if your current business option isn't yielding much fruit? Are you pumping in capital but you are not enjoying the expected revenue? Another fast way to grow is to diversify your products or service offerings.

You could produce several products within a particular niche, or unrelated products to your existing business.

For example, if your business focuses on academia, you could use a horizontal diversification strategy to provide not only notebooks but biros, pencils, mathematical sets, and textbooks.

A recognizable company that diversified its products and services is Walt Disney. Walt Disney started with Mickey Mouse and later expanded their reach with TV shows and music.

Diversification of your products will help you generate more revenue streams and protect your brand from competitors.

There are seasons when a particular product you offer may not thrive. You can create new business lines and services. With this strategy, diversifying will assist you during periods of low income to get back on track.

Do not diversify blindly, take calculated risks. Investing in unrelated products (conglomerate diversification) is far riskier because you are exploring a new market.

Strategic partnerships will help you remain afloat and guarantee your success. A partner must be someone who can bring the utmost value to your business, and whose strengths are the major areas you are lacking in.

Research properly, weigh out options, and make sure you are involving the right people to enjoy fast business growth.

10. Extend to New Markets

One of the reasons why you may not have expanded or grown is because you are staying in the same market for too long. Sometimes, a particular state, country, or city may not encourage the sale of a product or service.

As a business owner, continually research and check out new places, and new audiences where you can sell your products, and distribute your services.

Before you extend or enter a new place or a foreign country, you must strategize. Using the same processes you are familiar with will cause more damage than good.

You can collect relevant information and facts and familiarize yourself with the culture of the people. That way, you will know if your product is indeed relevant for them or another passing object that will remain on shelves.

Time is a very important factor when planning to venture into new markets. Be aware of the perfect time to enter the market, when to advertise, and the right channels to increase sales and bring in more revenue.

Check out competitors and learn from them so you can stand out. A tweak or adjustment to your product may be all you need to remain ahead of others.

Explore Further

- Types of Business Strategies

- Best Small Business Software

- Best Small Business Ideas

- Small Business Websites

- Best Small-Scale Business Ideas

- How to Start a Business With No Money

- Ultimate List of Small Business Statistics

- Best Website Builders for Small Business

- What Type of Business Should I Start?

- How to Start an eCommerce Business

Was This Article Helpful?

Martin Luenendonk

Martin loves entrepreneurship and has helped dozens of entrepreneurs by validating the business idea, finding scalable customer acquisition channels, and building a data-driven organization. During his time working in investment banking, tech startups, and industry-leading companies he gained extensive knowledge in using different software tools to optimize business processes.

This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.